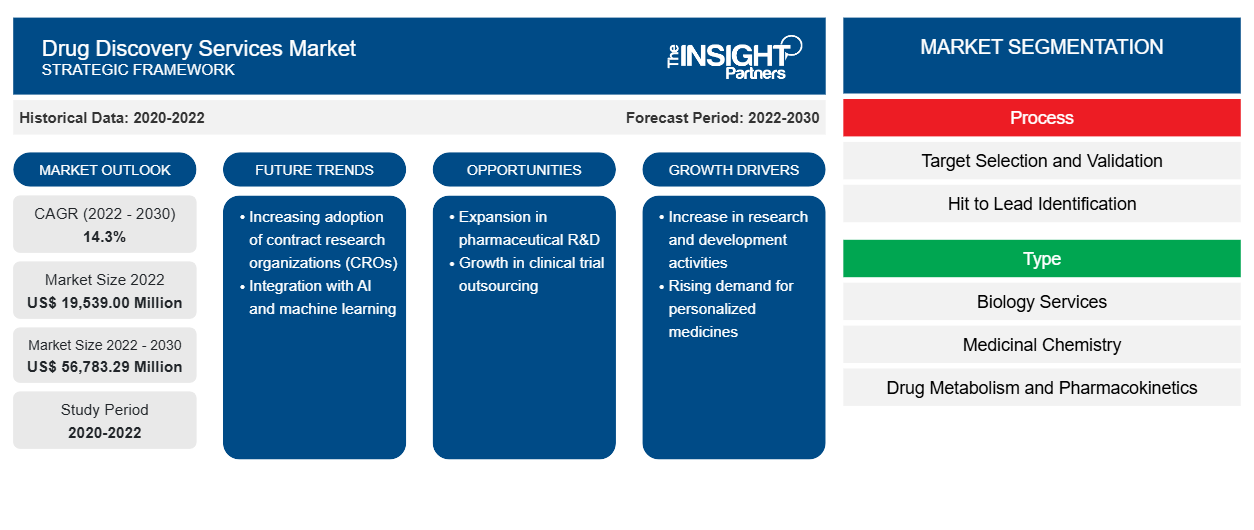

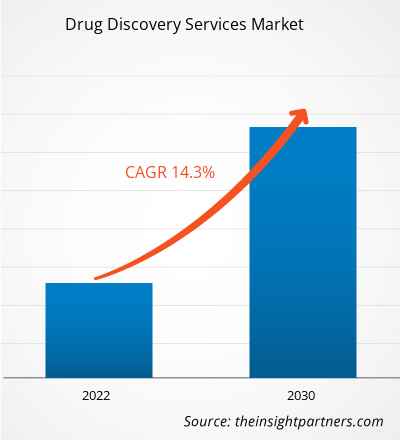

[تقرير بحثي] من المتوقع أن ينمو حجم سوق خدمات اكتشاف الأدوية من 19،539.00 مليون دولار أمريكي في عام 2022 إلى 56،783.29 مليون دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل السوق معدل نمو سنوي مركب بنسبة 14.3٪ من عام 2022 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

اكتشاف الأدوية هو عملية تحديد أو تطوير أدوية جديدة لعلاج الأمراض وتحسين صحة الإنسان. وهي تنطوي على تحديد مرشحي الأدوية المحتملين في مراحل تتراوح من تركيبها إلى الاختبار في المختبرات والنماذج الحيوانية، والتقييم في التجارب البشرية. يقدم مزودو خدمات اكتشاف الأدوية الخبرة والموارد المتخصصة لدعم عملية اكتشاف الأدوية. يمكن أن يشمل ذلك الكيمياء الطبية، والنمذجة الحاسوبية، والفحص عالي الإنتاجية، وخدمات الاختبار قبل السريري . غالبًا ما يتم تقديم هذه الخدمات من قبل منظمات أبحاث تعاقدية ( CROs ) أو مؤسسات بحثية أكاديمية. تختار شركات الأدوية وشركات التكنولوجيا الحيوية هذه الخدمات لتسريع عمليات اكتشاف الأدوية دون المساس بكفاءتها.

محركات النمو والتحديات:

يشهد سوق خدمات اكتشاف الأدوية نموًا كبيرًا بسبب الطلب المتزايد باستمرار على العلاجات الجديدة عبر مجموعة من المجالات العلاجية. إن عملية اكتشاف الأدوية معقدة وتستغرق وقتًا طويلاً، ويعتمد نجاحها على الأبحاث المكثفة التي أجريت على مرشحين محتملين للأدوية بالإضافة إلى اختبارهم والتحقق من صحتهم. ونتيجة لذلك، تعتمد شركات الأدوية ومؤسسات البحث بشكل متزايد على مقدمي خدمات اكتشاف الأدوية، الذين يدعمون جهود تطوير الأدوية. يقدم مقدمو الخدمات هؤلاء تحديد الأهداف والتحقق منها، وتحسين النتائج، والدراسات السريرية المسبقة ، واختبارات الحركية الدوائية وعلم السموم، من بين خدمات أخرى جديرة بالملاحظة. تسعى شركات التكنولوجيا الحيوية والأدوية إلى تطوير علاجات مستهدفة يمكنها معالجة الخصائص الجينية والجزيئية المحددة للمرضى الأفراد، مما يؤدي إلى نهج أكثر تخصيصًا للرعاية الصحية. هذا، والتركيز المتزايد على الطب الدقيق والعلاجات الشخصية يزيد من الطلب على خدمات اكتشاف الأدوية.

إن زيادة استثمارات البحث والتطوير من قبل شركات الأدوية، وتوافر التقنيات المتقدمة مثل الفحص عالي الإنتاجية، والنمذجة الحاسوبية، والذكاء الاصطناعي، تفيد سوق خدمات اكتشاف الأدوية. تمكن هذه التقنيات من عمليات اكتشاف الأدوية بشكل أكثر كفاءة وفعالية، مما يؤدي إلى معدل نجاح أعلى في طرح الأدوية الجديدة في السوق. إن عملية اكتشاف وتطوير الأدوية الجديدة مكلفة، وغالبًا ما تتطلب استثمارًا كبيرًا في البحث والتطوير والتجارب السريرية. ارتفعت التكلفة المتوسطة لإنشاء أدوية جديدة بين أفضل 20 دواء حيويًا في جميع أنحاء العالم تم فحصها في دراسة الهندسة الوراثية والتكنولوجيا الحيوية بنسبة 15٪ (298 مليون دولار) إلى ما يقرب من 2.3 مليار دولار في العام الماضي.

إن ارتفاع معدل فشل الأدوية المرشحة في المراحل اللاحقة من الدراسات السريرية يزيد من التكلفة الإجمالية لتطوير الأدوية. ونتيجة لهذا، تسعى شركات الأدوية والتكنولوجيا الحيوية بشكل متزايد إلى الحصول على خدمات اكتشاف الأدوية الفعالة من حيث التكلفة، مما يجبر مقدمي الخدمات على تقديم أسعار تنافسية مع الحفاظ على معايير الجودة العالية. كما تؤثر التكلفة المرتفعة لجزيئات الأدوية على القدرة على تحمل تكاليف العلاجات الجديدة للمرضى، وخاصة في حالة الأمراض النادرة أو المجالات العلاجية المتخصصة، وهي منطقة رئيسية من التحديات لكل من مطوري الأدوية وأنظمة الرعاية الصحية وسط عملية توفير الوصول إلى العلاجات المبتكرة.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق خدمات اكتشاف الأدوية:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

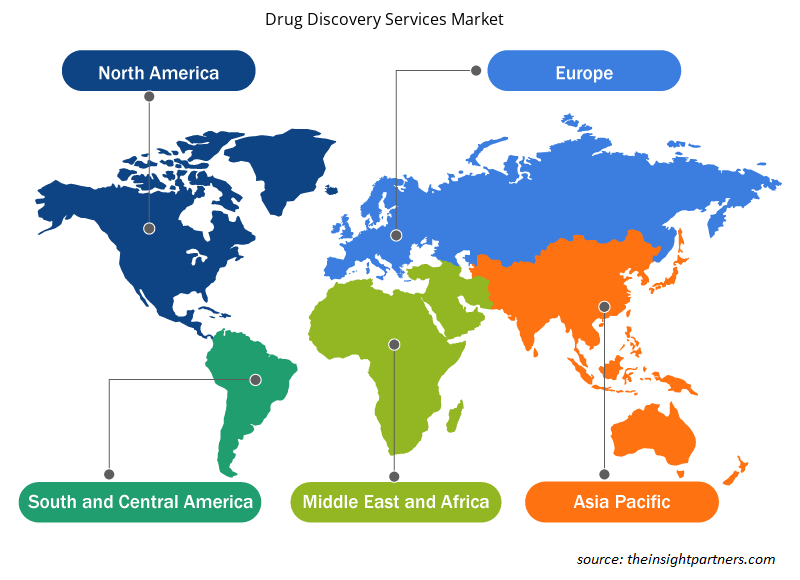

يتم تقسيم سوق خدمات اكتشاف الأدوية على أساس العملية والنوع ونوع الجزيء والمجال العلاجي والمستخدم النهائي. بناءً على العملية، يتم تقسيم السوق إلى اختيار الهدف والتحقق منه، وتحديد الهدف الرئيسي، وغيرها (تطوير الاختبار، والفحص، وما إلى ذلك). يتم تقسيم سوق خدمات اكتشاف الأدوية، حسب النوع، إلى خدمات الأحياء، واستقلاب الأدوية الكيميائية الطبية، والدوائية الحركية . من حيث نوع الجزيء، يتم تصنيف سوق خدمات اكتشاف الأدوية على أنها بيولوجية وجزيئات صغيرة. على أساس المجالات العلاجية، يتم التمييز بين السوق وأمراض القلب والأوعية الدموية والأورام وأمراض الأعصاب والسكري وأمراض الجهاز التنفسي وغيرها. حسب المستخدم النهائي، يتم تقسيم سوق خدمات اكتشاف الأدوية إلى شركات الأدوية والتكنولوجيا الحيوية والمعاهد الأكاديمية وغيرها. بناءً على الجغرافيا، يتم تقسيم سوق خدمات اكتشاف الأدوية إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (المملكة المتحدة وألمانيا وفرنسا وإيطاليا وإسبانيا وبقية أوروبا)، وآسيا والمحيط الهادئ (الصين واليابان والهند وكوريا الجنوبية وأستراليا وبقية آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (الإمارات العربية المتحدة والمملكة العربية السعودية وجنوب أفريقيا وبقية الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

استحوذ قطاع الجزيئات الصغيرة على حصة أكبر من الإيرادات في سوق خدمات اكتشاف الأدوية، استنادًا إلى نوع الجزيء. ويعزى نمو سوق الجزيئات الصغيرة إلى حقيقة أنها سهلة الدراسة ومحددة جيدًا وسهلة التوصيف.

في عام 2022، استحوذ قطاع الكيمياء الطبية على أكبر حصة في سوق خدمات اكتشاف الأدوية، حسب النوع. تستخدم الكيمياء الطبية على نطاق واسع في مجالات مختلفة من اكتشاف الأدوية، بدءًا من توصيل المرشحين إلى الدراسات السريرية المسبقة.

على أساس المجال العلاجي، هيمن قطاع الأورام على سوق خدمات اكتشاف الأدوية في عام 2022. ويعزى نمو السوق لهذا القطاع إلى زيادة جهود اكتشاف الأدوية المتعلقة بالسرطان في جميع أنحاء العالم. يعد علم الأورام سوقًا متنامية باستمرار بسبب ارتفاع معدل الإصابة بأنواع مختلفة من السرطان في عموم السكان. وقد قدرت الوكالة الدولية لأبحاث السرطان حوالي 10 ملايين حالة وفاة مرتبطة بالسرطان و19.3 مليون حالة إصابة جديدة بالسرطان في عام 2020. ومن المتوقع أن يزيد العدد العالمي لحالات الإصابة بالسرطان الجديدة بنسبة 47٪ من عام 2020 إلى عام 2040. ونتيجة لذلك، من المتوقع حدوث ما يقرب من 28.4 مليون حالة إصابة جديدة بالسرطان في جميع أنحاء العالم بحلول عام 2040.

رؤى إقليمية حول سوق خدمات اكتشاف الأدوية

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق خدمات اكتشاف الأدوية طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق خدمات اكتشاف الأدوية والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق خدمات اكتشاف الأدوية

نطاق تقرير سوق خدمات اكتشاف الأدوية

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 19,539.00 مليون دولار أمريكي |

| حجم السوق بحلول عام 2030 | 56,783.29 مليون دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 14.3% |

| البيانات التاريخية | 2020-2022 |

| فترة التنبؤ | 2022-2030 |

| القطاعات المغطاة | حسب العملية

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في السوق: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق خدمات اكتشاف الأدوية نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلك المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق خدمات اكتشاف الأدوية هي:

- شركة اجيلنت تكنولوجيز اوبيكويجنت

- شركة مختبرات أبوت

- شركة أدفينوس ثيرابيوتيكس ألباني للأبحاث الجزيئية

- أوريجين

- شركة باير ايه جي

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق خدمات اكتشاف الأدوية

التحليل الإقليمي:

بناءً على الجغرافيا، يتم تقسيم سوق خدمات اكتشاف الأدوية بشكل أساسي إلى أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى. تعد أمريكا الشمالية المساهم الأكثر أهمية في نمو السوق العالمية. ويعزى نمو السوق في هذه المنطقة إلى الاستثمارات التي قامت بها شركات تطوير الأدوية، والمنح الكبيرة التي تقدمها حكومة الولايات المتحدة، والحضور القوي لشركات تطوير الأدوية الكبرى، والبنية التحتية للرعاية الصحية الراسخة، وزيادة حالات الإصابة بالأمراض المزمنة.

قدرت "حقائق وأرقام السرطان لعام 2022" الصادرة عن الجمعية الأمريكية للسرطان حوالي 1,918,030 حالة إصابة جديدة بالسرطان و609,360 حالة وفاة مرتبطة بالسرطان في الولايات المتحدة بحلول نهاية عام 2022. ونظرًا لارتفاع معدل الإصابة بالسرطان في هذه المنطقة، فمن المرجح أن تزدهر أنشطة البحث لابتكار أدوية للسرطان في الولايات المتحدة في السنوات القادمة. وقعت شركة CytoReason وشركة Pfizer اتفاقية تعاون متعددة السنوات في سبتمبر 2022. ووفقًا لهذه الصفقة، يمكن لشركة Pfizer استخدام تقنية الذكاء الاصطناعي من CytoReason لتطوير الأدوية. ومن المتوقع أن يؤدي استخدام تقنية الذكاء الاصطناعي في اكتشاف الأدوية من قبل الشركات الكبرى في الولايات المتحدة إلى دفع توسع سوق خدمات اكتشاف الأدوية.

من المتوقع أن تسجل منطقة آسيا والمحيط الهادئ أعلى معدل نمو سنوي مركب في سوق خدمات اكتشاف الأدوية خلال الفترة 2022-2030. ويعزى نمو السوق في هذه المنطقة إلى زيادة الاستثمارات في أنشطة البحث والتطوير في دول مثل الصين والهند واليابان وكوريا الجنوبية، والتي تبرز كمراكز رئيسية للصناعات الدوائية والتكنولوجيا الحيوية. وعلاوة على ذلك، فإن وجود مجموعة كبيرة من الباحثين والعلماء المهرة، إلى جانب انخفاض تكاليف التشغيل مقارنة بالدول الغربية، يجعل منطقة آسيا والمحيط الهادئ وجهة جذابة لاستعانة بمصادر خارجية لخدمات اكتشاف الأدوية. إن الانتشار المتزايد للأمراض المزمنة والحاجة إلى أدوية مبتكرة لتلبية الاحتياجات الطبية غير الملباة يخلقان طلبًا على أدوية جديدة، وبالتالي الاستفادة من نمو سوق خدمات اكتشاف الأدوية في المنطقة.

المنافسة والشركات الرئيسية:

تعد Agilent Technologies Ubiquigent وAbbott Laboratories Inc. وAdvinus Therapeutics Albany Molecular Research Inc. وAurigene وBayer AG وAstraZeneca PLC وCharles River Laboratories International وCovance وChemBridge Corporation من بين اللاعبين البارزين الذين يعملون في سوق خدمات اكتشاف الأدوية. تركز هذه الشركات على توسيع عروض الخدمات لتلبية الطلب المتزايد من المستهلكين في جميع أنحاء العالم. يسمح لها وجودها العالمي بخدمة مجموعة كبيرة من العملاء، مما يسمح لها لاحقًا بتوسيع حصتها في السوق.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Increasing demand for novel therapies across a wide range of therapeutic areas, and rising R&D expenditure in the pharmaceutical and biotechnology industries are driving the drug discovery services market. However, the high cost of drug discoveries hinders the drug discovery services market growth.

The drug discovery services market was valued at US$ 19,539.00 million in 2022.

Drug discovery is the process of identifying and characterizing molecules with the potential to safely modulate disease, with a goal to bring medicines that can improve the lives of patients. It is a lengthy and resource intensive process, that requires close cooperation across multiple disciplines.

The drug discovery services market has major market players, including Abbott Laboratories Inc., Agilent Technologies Ubiquigent, Albany Molecular Research Inc., Advinus Therapeutics, AstraZeneca PLC, Bayer AG, Aurigene, Charles River Laboratories International, ChemBridge Corporation, and Covance.

The drug discovery services market is expected to be valued at US$ 56,783.29 million in 2030.

Based on molecule type, the small molecules segment held the most revenue share in the worldwide drug discovery services market. Its rise was encouraged by the tiny molecules' simple, well-defined, and easy-to-characterized nature. The public is more in demand for and considerably more productive with small molecule pharmaceuticals. Because they are small molecules, they small molecules can affect cells readily and can be used to treat patients effectively. This market has grown as a result of a growing understanding of the advantages of small-molecule medications.

In 2022, the medicinal chemistry segment held the largest market share in the drug discovery services market based on type. Medicinal chemistry finds extensive use in drug discovery services, ranging from candidate delivery to preclinical studies. Consequently, this segment's prominence can be attributed to its significance. Furthermore, the biopharmaceutical businesses' increased outsourcing is anticipated to fuel this segment's expansion.

In 2022, on the basis of therapeutic area, the global market for drug discovery services was dominated by the oncology segment, owing to increase in cancer-related medication discovery efforts. The oncology market has grown as a result of the rising incidence of various cancers in the general population. The International Agency for Research on Cancer estimates that there will be about 10 million cancer-related deaths and 19.3 million new cancer cases in 2020. The global number of new cancer cases is predicted to increase by 47% between 2020 and 2040. As a result, it is projected that there will be about 28.4 million new instances of cancer worldwide in 2040.

The List of Companies - Drug Discovery Services Market

- Agilent Technologies Ubiquigent

- Abbott Laboratories Inc.

- Advinus Therapeutics Albany Molecular Research Inc.

- Aurigene

- Bayer AG

- AstraZeneca PLC

- Charles River Laboratories International

- Covance

- ChemBridge Corporation

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير