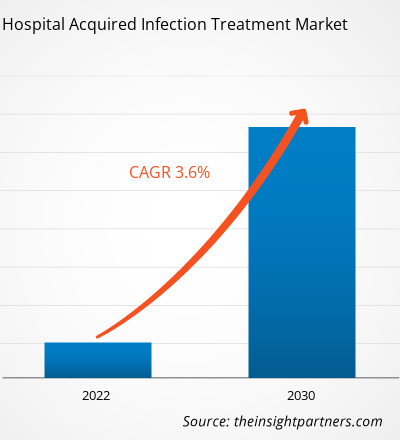

[تقرير بحثي] من المتوقع أن ينمو سوق علاج العدوى المكتسبة من المستشفيات من 15،099.19 مليون دولار أمريكي في عام 2022 إلى 19،978.39 مليون دولار أمريكي بحلول عام 2030؛ ومن المتوقع أن يسجل معدل نمو سنوي مركب بنسبة 3.6٪ من عام 2022 إلى عام 2030.

رؤى السوق ووجهة نظر المحلل:

قد تتطور العدوى المكتسبة من المستشفيات (HAIs)، والمعروفة أيضًا باسم العدوى المكتسبة من المستشفيات، في مجموعة متنوعة من البيئات، بما في ذلك المستشفيات ومؤسسات الرعاية طويلة الأجل والبيئات الخارجية، ويمكن أن تظهر أيضًا بعد الخروج من المستشفى. يمكن أن تنطوي العدوى المكتسبة من المستشفيات أيضًا على عدوى مهنية تؤثر على العاملين في مجال الرعاية الصحية. العوامل الرئيسية التي تدفع نمو سوق علاج العدوى المكتسبة من المستشفيات هي ارتفاع معدل انتشار العدوى المكتسبة من المستشفيات والتركيز المتزايد على سلامة المرضى وجودة الرعاية. ومع ذلك، فإن تهديد مقاومة مضادات الميكروبات يعيق نمو سوق علاج العدوى المكتسبة من المستشفيات .

محركات النمو ومعوقاته:

تعد عدوى مجرى الدم المرتبطة بالقسطرة المركزية، والتهابات المسالك البولية المرتبطة بالقسطرة، والالتهاب الرئوي المرتبط بأجهزة التنفس الصناعي من الأمثلة القليلة على العدوى المرتبطة بالرعاية الصحية. يمكن أن تنشأ هذه العدوى، المعروفة باسم عدوى موقع الجراحة، أيضًا في مواقع الجراحة. وفقًا لتقرير مراكز السيطرة على الأمراض والوقاية منها "تقرير التقدم الوطني والولائي للعدوى المرتبطة بالرعاية الصحية لعام 2020" المنشور في عام 2021، زادت حالات عدوى مجرى الدم المرتبطة بالقسطرة المركزية، وبكتيريا المكورات العنقودية الذهبية المقاومة للميثيسيلين (MRSA)، والأحداث المرتبطة بأجهزة التنفس الصناعي بنسبة 24٪ و35٪ و15٪ على التوالي، في الولايات المتحدة بين عامي 2019 و2020.

علاوة على ذلك، وفقًا لتقرير يناير 2022 الصادر عن الشبكة الوطنية لسلامة الرعاية الصحية (NHSN)، فإن التهابات المسالك البولية هي خامس أكثر أنواع العدوى المرتبطة بالرعاية الصحية شيوعًا. تمثل التهابات المسالك البولية أكثر من 9.5٪ من حالات المستشفيات للرعاية الحادة. تحدث عدوى المسالك البولية المرتبطة بالقسطرة (CAUTI) بسبب القسطرة البولية المستخدمة لتصريف البول من المثانة. تعد عدوى المسالك البولية المرتبطة بالقسطرة واحدة من أكثر أنواع العدوى شيوعًا بين مرضى التهابات المسالك البولية في المستشفيات. وفقًا لمراكز السيطرة على الأمراض والوقاية منها (CDC)، فإن ما يقرب من 75٪ من العدوى مرتبطة بقسطرة بولية. أثناء إقامتهم في المستشفى، يحتاج 15٪ إلى 25٪ من المرضى في المستشفى إلى استخدام قسطرة بولية. يعد استخدام قسطرة البول لفترة طويلة هو عامل الخطر الرئيسي للإصابة بعدوى المسالك البولية المرتبطة بالقسطرة. تتضمن مضاعفات عدوى المسالك البولية المرتبطة بالقسطرة معاناة المريض، وإطالة فترة إقامته في المستشفى، وزيادة تكاليف العلاج، وحتى الموت.

علاوة على ذلك، وفقًا لمراكز السيطرة على الأمراض والوقاية منها، فإن التهابات المسالك البولية مسؤولة عن أكثر من 13000 حالة وفاة كل عام. يسبب التهاب المثانة الحاد غير المعقد حوالي ستة أيام من الانزعاج، مما يؤدي إلى حوالي 7 ملايين زيارة مكتبية كل عام بتكلفة 1.6 مليار دولار أمريكي. ونتيجة لذلك، يفرض العدد المتزايد من حالات العدوى المرتبطة بالرعاية الصحية عبئًا ماليًا كبيرًا على نظام الرعاية الصحية. إن الانتشار المتزايد لالتهاب المسالك البولية المرتبط بالرعاية، إلى جانب الطلب المتزايد على الأدوية للعلاج، يدفع السوق إلى الأمام.

ومع ذلك، تشكل مقاومة مضادات الميكروبات تحديًا كبيرًا لعلاج العدوى المرتبطة بالرعاية الصحية، مما يحد من فعالية العوامل المضادة للميكروبات الموجودة ويستلزم تطوير استراتيجيات علاجية جديدة وبدائل مضادة للميكروبات لمكافحة مسببات الأمراض المقاومة بشكل فعال.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق علاج العدوى المكتسبة من المستشفيات:

- احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

تقسيم التقرير ونطاقه:

يتم تقسيم سوق علاج العدوى المكتسبة في المستشفيات العالمية على أساس فئة الدواء ونوع العدوى وقناة التوزيع. بناءً على فئة الدواء، يتم تقسيم سوق علاج العدوى المكتسبة في المستشفيات إلى أدوية مضادة للبكتيريا وأدوية مضادة للفيروسات وأدوية مضادة للفطريات وغيرها. بناءً على نوع العدوى، يتم التمييز بين علاج العدوى المكتسبة في المستشفيات إلى التهابات المسالك البولية والالتهاب الرئوي المرتبط بجهاز التنفس الصناعي والتهابات موقع الجراحة والتهابات مجرى الدم وغيرها من التهابات المستشفيات. بناءً على قناة التوزيع، يتم تقسيم السوق إلى صيدليات المستشفيات وصيدليات التجزئة والتجارة الإلكترونية وغيرها. يتم تقسيم سوق علاج العدوى المكتسبة من المستشفيات، على أساس الجغرافيا، إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (ألمانيا وفرنسا وإيطاليا والمملكة المتحدة وروسيا وبقية أوروبا)، وآسيا والمحيط الهادئ (أستراليا والصين واليابان والهند وكوريا الجنوبية وبقية آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (جنوب أفريقيا والمملكة العربية السعودية والإمارات العربية المتحدة وبقية الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية أمريكا الجنوبية والوسطى).

التحليل القطاعي:

ينقسم سوق علاج العدوى المكتسبة من المستشفيات، حسب فئة الدواء، إلى أدوية مضادة للبكتيريا وأدوية مضادة للفيروسات وأدوية مضادة للفطريات وغيرها. احتل قطاع الأدوية المضادة للبكتيريا الحصة الأكبر في السوق في عام 2022 ومن المتوقع أن يسجل أعلى معدل نمو سنوي مركب خلال الفترة 2022-2030.

ينقسم سوق علاج العدوى المكتسبة من المستشفيات، حسب نوع العدوى، إلى التهابات المسالك البولية ، والالتهاب الرئوي المرتبط بأجهزة التنفس الصناعي، والتهابات موقع الجراحة، والتهابات مجرى الدم، والتهابات المستشفيات الأخرى. احتل قطاع التهابات المسالك البولية أكبر حصة سوقية في عام 2022. ومع ذلك، من المتوقع أن يسجل قطاع الالتهاب الرئوي المرتبط بأجهزة التنفس الصناعي أعلى معدل نمو سنوي مركب من عام 2022 إلى عام 2030.

ينقسم سوق علاج العدوى المكتسبة من المستشفيات، حسب قناة التوزيع، إلى صيدليات المستشفيات وصيدليات التجزئة والتجارة الإلكترونية وغيرها. في عام 2022، استحوذ قطاع صيدليات المستشفيات على أكبر حصة في السوق، ومن المتوقع أن يسجل نفس القطاع أعلى معدل نمو سنوي مركب خلال الفترة 2022-2030.

التحليل الإقليمي:

على أساس الجغرافيا، يتم تقسيم سوق علاج العدوى المكتسبة من المستشفيات العالمية إلى خمس مناطق رئيسية هي أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ وأمريكا الجنوبية والوسطى والشرق الأوسط وأفريقيا.

في عام 2022، استحوذت أمريكا الشمالية على أكبر حصة من حجم سوق علاج العدوى المكتسبة في المستشفيات على مستوى العالم. وتتمتع الولايات المتحدة بمعدل انتشار مرتفع للعدوى المرتبطة بالرعاية الصحية، مما يدفع سوق علاج العدوى المكتسبة في المستشفيات إلى النمو. ووفقًا لمراكز السيطرة على الأمراض والوقاية منها، في أي يوم، يعاني حوالي 1 من كل 31 مريضًا في المستشفى من عدوى مرتبطة بالرعاية الصحية على الأقل. وبالمثل، وفقًا لمكتب الوقاية من الأمراض وتعزيز الصحة، يمكن أن تؤدي العدوى المرتبطة بالرعاية الصحية والالتهابات الأخرى إلى تعفن الدم، وتسبب حوالي 1.7 مليون حالة مرضية و270 ألف حالة وفاة سنويًا في الولايات المتحدة. وبالتالي، فإن الانتشار المرتفع للعدوى المرتبطة بالرعاية الصحية بين الأشخاص في الولايات المتحدة يغذي نمو سوق علاج العدوى المكتسبة في المستشفيات.

تطورات الصناعة والفرص المستقبلية:

فيما يلي قائمة بالمبادرات المختلفة التي اتخذها اللاعبون الرئيسيون العاملون في سوق علاج العدوى المكتسبة من المستشفيات العالمية:

- في مايو 2023، أعلنت شركة Innoviva Specialty Therapeutics أن إدارة الغذاء والدواء الأمريكية (FDA) وافقت على XACDURO (سولباكتام للحقن؛ دورلوباكتام للحقن)، المعبأ للاستخدام الوريدي في المرضى الذين تبلغ أعمارهم 18 عامًا أو أكثر لعلاج الالتهاب الرئوي الجرثومي المكتسب من المستشفى والالتهاب الرئوي الجرثومي المرتبط بجهاز التنفس الصناعي (HABP/VABP) الناجم عن عزلات حساسة من مجمع Acinetobacter baumannii-calcoaceticus (Acinetobacter). ذكرت شركة Innoviva Specialty Therapeutics أنها تركز على تقديم علاجات مبتكرة في الرعاية الحرجة والأمراض المعدية.

- في مايو 2023، أعلن باحثون من المعهد الهندي لتعليم العلوم والبحث (IISER)، في بوني ومعهد أبحاث الأدوية المركزي (CSIR-CDRI)، لكناو أنهم اكتشفوا مضادًا حيويًا جديدًا محتملاً ضد Acinetobacter baumannii، والذي يسبب بشكل متكرر العدوى المرتبطة بالرعاية الصحية.

- في سبتمبر 2020، أعلنت شركة Shionogi & Co Ltd أن إدارة الغذاء والدواء قد وافقت على طلب دواء جديد تكميلي (sNDA) لـ FETROJA (cefiderocol) لعلاج المرضى الذين تبلغ أعمارهم 18 عامًا أو أكثر والذين يعانون من الالتهاب الرئوي الجرثومي المكتسب من المستشفى والالتهاب الرئوي الجرثومي المرتبط بجهاز التنفس الصناعي (HABP / VABP) الناجم عن الكائنات الحية الدقيقة سلبية الجرام الحساسة مثل مجمع Enterobacter cloacae، Klebsiella pneumoniae، مجمع Acinetobacter baumannii، Escherichia coli، Pseudomonas aeruginosa، و Serratia marcescens.

- في يونيو 2020، أعلنت شركة ميرك أن إدارة الغذاء والدواء الأمريكية (FDA) قد وافقت على طلب دواء جديد تكميلي (sNDA) لـ RECARBRIO (إيميبينيم وسيلاستاتين وريليبكتام) لعلاج المرضى الذين تبلغ أعمارهم 18 عامًا أو أكثر والذين يعانون من الالتهاب الرئوي الجرثومي المكتسب من المستشفى والالتهاب الرئوي الجرثومي المرتبط بجهاز التنفس الصناعي (HABP / VABP)، الناجم عن الكائنات الحية الدقيقة سلبية الجرام الحساسة مثل مجمع Acinetobacter calcoaceticus-baumannii، Klebsiella oxytoca، Klebsiella pneumoniae، Enterobacter cloacae، Escherichia coli، Haemophilus influenzae، Klebsiella aerogenes، Pseudomonas aeruginosa، و Serratia marcescens.

رؤى إقليمية حول سوق علاج العدوى المكتسبة من المستشفيات

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق علاج العدوى المكتسبة من المستشفيات طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق علاج العدوى المكتسبة من المستشفيات والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق علاج العدوى المكتسبة في المستشفيات

نطاق تقرير سوق علاج العدوى المكتسبة من المستشفيات

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2022 | 15,099.19 مليون دولار أمريكي |

| حجم السوق بحلول عام 2030 | 19,978.39 مليون دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2022 - 2030) | 3.6% |

| البيانات التاريخية | 2020-2022 |

| فترة التنبؤ | 2022-2030 |

| القطاعات المغطاة | حسب فئة الدواء

|

| المناطق والدول المغطاة | أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

كثافة اللاعبين في سوق علاج العدوى المكتسبة من المستشفيات: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق علاج العدوى المكتسبة من المستشفيات نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق علاج العدوى المكتسبة من المستشفيات هي:

- شركة ميرك آند كو

- شركة فايزر

- شركة آبفي

- شركة باراتيك للادوية

- يوجيا الولايات المتحدة المحدودة

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق علاج العدوى المكتسبة من المستشفيات

المنافسة والشركات الرئيسية:

تعد Merck & Co Inc وPfizer Inc وAbbVie Inc وParatek Pharmaceuticals Inc وEugia US LLC وAbbott Laboratories وCumberland Pharmaceuticals Inc وInnoviva Specialty Therapeutics Inc وCipla Ltd وEli Lilly and Company من بين اللاعبين البارزين الذين يعملون في سوق علاج العدوى المكتسبة من المستشفيات. تركز هذه الشركات على التقنيات الجديدة والتقدم في المنتجات الحالية والتوسع الجغرافي لتلبية الطلب المتزايد من المستهلكين في جميع أنحاء العالم وزيادة نطاق منتجاتها في محافظ التخصصات.

- التحليل التاريخي (سنتان)، السنة الأساسية، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالميًا وإقليميًا وقطريًا

- الصناعة والمنافسة

- مجموعة بيانات Excel

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

الأسئلة الشائعة

Hospital-acquired infections (HAI), also known as nosocomially acquired infections. HAIs are infections acquired during medical treatment that were not present at the time of admission. They may develop in a variety of settings, including hospitals, long-term care institutions, and ambulatory settings, and they can also appear after discharge. HAIs can also involve occupational infections that affect healthcare workers.

The hospital acquired infection treatment market majorly consists of the players, including Merck & Co Inc, Pfizer Inc, AbbVie Inc, Paratek Pharmaceuticals Inc, Eugia US LLC, Abbott Laboratories, Cumberland Pharmaceuticals Inc, Innoviva Specialty Therapeutics Inc, Cipla Ltd, and Eli Lilly and Company.

Key factors driving the hospital acquired infection treatment market growth include the high prevalence of hospital-acquired infections (HAI) and the growing focus on patient safety and quality care.

The hospital acquired infection treatment market was valued at US$ 15,099.19 million in 2022.

The hospital acquired infection treatment market, by distribution channel, is segmented into hospital pharmacies, retail pharmacies, e-commerce, and others. In 2022, the hospitals pharmacies segment held the largest market share, and the same segment is anticipated to register the highest CAGR during 2022–2030.

The hospital acquired infection treatment market is expected to be valued at US$ 19,978.39 million in 2030.

The hospital acquired infection treatment market, by infection type, is segmented into urinary tract infections, ventilator-associated pneumonia, surgical site infections, bloodstream infections, and other hospital infections. The urinary tract infections segment held a larger market share in 2022; However, the ventilator-associated pneumonia segment is anticipated to register a higher CAGR during 2022-2030.

The hospital acquired infection treatment market, by drug class, is segmented into antibacterial drugs, antiviral drugs, antifungal drugs, and others. The antibacterial drugs segment held a larger market share in 2022, and the same segment is anticipated to register a higher CAGR during 2022-2030.

Trends and growth analysis reports related to Life Sciences : READ MORE..

The List of Companies - Hospital Acquired Infection Treatment Market

- Merck & Co Inc

- Pfizer Inc

- AbbVie Inc

- Paratek Pharmaceuticals Inc

- Eugia US LLC

- Abbott Laboratories

- Cumberland Pharmaceuticals Inc

- Innoviva Specialty Therapeutics Inc

- Cipla Ltd

- Eli Lilly and Company

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

احصل على عينة مجانية لهذا التقرير

احصل على عينة مجانية لهذا التقرير