استراتيجيات سوق أجهزة مساعدة البطين الأيسر، وأفضل اللاعبين، وفرص النمو، والتحليل والتنبؤ بحلول عام 2028

البيانات التاريخية : 2019-2020 | سنة الأساس : 2021 | فترة التنبؤ : 2022-2028توقعات سوق أجهزة مساعدة البطين الأيسر حتى عام 2028 - تأثير جائحة كوفيد-19 والتحليل العالمي حسب نوع التدفق (النبضي وغير النبضي)، والتصميم (أجهزة مساعدة البطين القابلة للزرع وأجهزة مساعدة البطين عبر الجلد)، والتطبيق (الجسر إلى الزرع، والعلاج في الوجهة، والجسر إلى التعافي، والجسر إلى الترشيح)

- تاريخ التقرير : Oct 2022

- رمز التقرير : TIPRE00018950

- الفئة : علوم الحياة

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 159

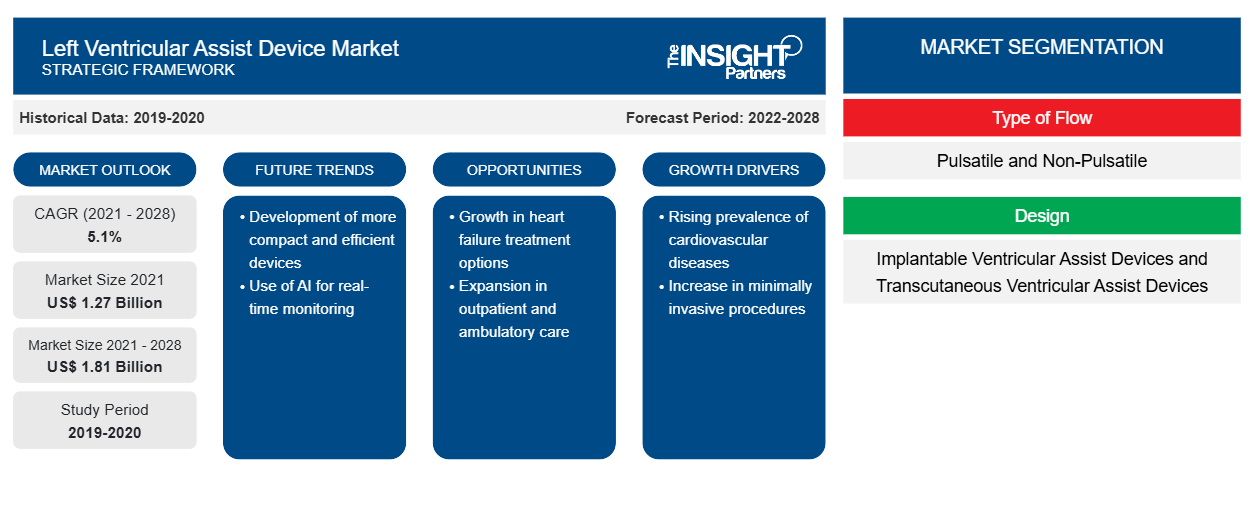

[تقرير بحثي] كان من المتوقع أن يصل سوق جهاز مساعدة البطين الأيسر إلى 1،272.08 مليون دولار أمريكي في عام 2021 ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 5.1٪ من عام 2022 إلى عام 2028.

يساعد جهاز مساعدة البطين الأيسر البطين الأيسر للقلب في ضخ الدم إلى بقية الجسم. يُعرف أيضًا باسم جهاز دعم الدورة الدموية الميكانيكي الذي يساعد في الحفاظ على الدورة الدموية السليمة داخل الجسم. إن الزيادة في انتشار اضطرابات القلب والأوعية الدموية وقصور القلب جنبًا إلى جنب مع الارتفاع الكبير في عدد كبار السن والسمنة يدفع نمو سوق جهاز مساعدة البطين الأيسر . ومع ذلك، فإن عمليات سحب المنتجات المتزايدة والمضاعفات المرتبطة بأجهزة مساعدة البطين الأيسر تعيق نمو السوق.

يقدم التقرير رؤى وتحليلات متعمقة لسوق جهاز مساعدة البطين الأيسر، مع التركيز على معايير مختلفة مثل اتجاهات السوق والتقدم التكنولوجي وديناميكيات السوق وتحليل المنافسة بين اللاعبين الرائدين في السوق العالمية. كما يتضمن تأثير جائحة كوفيد-19 على السوق في جميع المناطق. بسبب جائحة كوفيد-19، ركزت العديد من السلطات الصحية على الرعاية المتعلقة بالجائحة. لقد تجنبوا الاتصال البشري بسبب تزايد انتقال العدوى والضغط على موارد الرعاية الصحية من خلال تأجيل العمليات الجراحية الاختيارية، وتعليق العيادات الخارجية، وفرز الموظفين المشاركين في الرعاية العاجلة. علاوة على ذلك، فرضت العديد من البلدان قيودًا على وصول الموظفين غير السريريين إلى المنشأة والضيوف. علاوة على ذلك، كان هناك زيادة في انتشار حالات القلب والأوعية الدموية بين مرضى كوفيد-19، مما أدى إلى زيادة الطلب على أجهزة مساعدة البطين الأيسر، مما أدى إلى نمو السوق. اقترحت إرشادات كوفيد-19 الأخيرة لمهنيي الرعاية الصحية التركيز على الرعاية العاجلة وفرز الحالات لتأجيل العمليات الجراحية الاختيارية ومواعيد العيادة، مع الانتقال إلى الرعاية الافتراضية عند الاقتضاء.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق جهاز مساعدة البطين الأيسر: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

علاوة على ذلك، تستجيب شركات تصنيع العديد من أجهزة مساعدة البطين الأيسر لحالات الطوارئ من خلال استراتيجيات مختلفة مثل تصنيع معدات الوقاية الشخصية للعاملين في مجال الرعاية الصحية، وتوزيع الأدوية الصيدلانية، وغيرها من الأنشطة. علاوة على ذلك، في نوفمبر 2020، تعهدت شركة ميدترونيك ومؤسسة ميدترونيك بتقديم دعم مالي بقيمة 3.8 مليون دولار أمريكي على المستوى العالمي لتوفير الدعم للعاملين في مجال الرعاية الصحية من حيث الغذاء والدعم التشغيلي ودعم الصحة العقلية ومجموعات معدات الوقاية الشخصية وغيرها. وبالتالي، كان للوباء تأثير سلبي قصير المدى على سوق أجهزة مساعدة البطين الأيسر.PPEs for healthcare workers, distributing pharmaceutical drugs, and other activities. Further, in November 2020, Medtronic and the Medtronic foundation committed the financial support of US$ 3.8 million on a global level to provide healthcare worker support in terms of food, operational support, mental health support, PPE kits, and others. Thus, the pandemic had a short-term negative impact on the left ventricular assist device market.

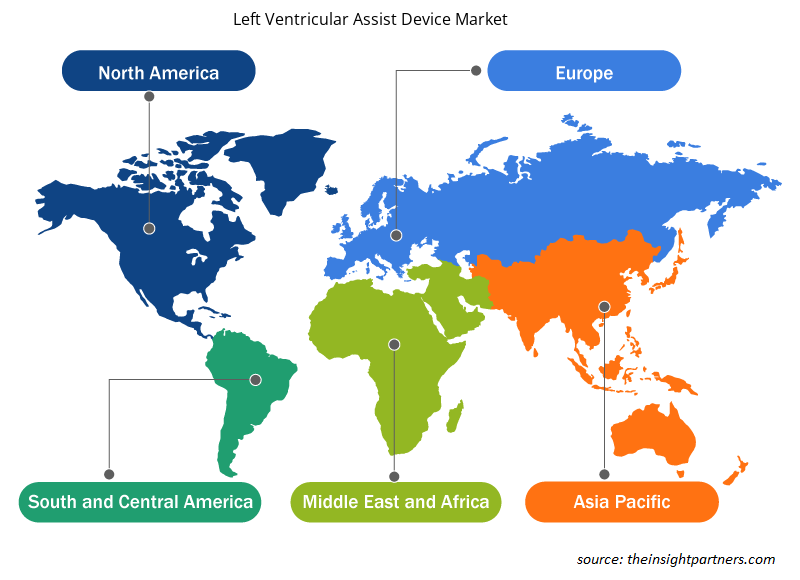

يتم تقسيم سوق أجهزة مساعدة البطين الأيسر على أساس نوع التدفق والتصميم والتطبيق والجغرافيا. حسب المنطقة، يتم تقسيم السوق إلى أمريكا الشمالية وأوروبا وآسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

رؤى السوق

زيادة حالات الإصابة بالأمراض والإجراءات المستهدفة

وفقًا لمنظمة الصحة العالمية، فإن أمراض القلب والأوعية الدموية هي أحد الأسباب الرئيسية للوفاة في جميع أنحاء العالم. ومن بين العوامل الرئيسية التي تزيد من انتشار أمراض القلب والأوعية الدموية والسكتة الدماغية التاريخ العائلي والعرق والعمر. كما يتزايد انتشار أمراض القلب والأوعية الدموية بسبب تعاطي التبغ وارتفاع ضغط الدم وارتفاع الكوليسترول وقلة التمارين الرياضية والنظام الغذائي غير الصحي والإفراط في تناول الكحول وأمراض مثل خلل شحميات الدم والسمنة والسكري. ووفقًا لجمعية القلب الأمريكية، سيعاني حوالي 41.4٪ من البالغين في الولايات المتحدة من ارتفاع ضغط الدم بحلول عام 2030 (زيادة بنسبة 8.4٪ عن عام 2012). وتقدر المنظمة أيضًا أن العبء العالمي لتكاليف أمراض القلب والأوعية الدموية سيصل إلى 1044 مليار دولار أمريكي بحلول عام 2030، وهو ما كان 863 مليار دولار أمريكي في عام 2010. وعلاوة على ذلك، ووفقًا لتقديرات منظمة الصحة العالمية، فإن الوفيات بسبب أمراض القلب والأوعية الدموية في جميع أنحاء العالم سترتفع من حوالي 17.9 مليون في عام 2016 إلى 23.6 مليون بحلول عام 2030. يذكر تقرير إيموري للرعاية الصحية أن الولايات المتحدة سجلت حوالي 5 ملايين حالة من الفشل الاحتقاني في عام 2022، وتم تشخيص حوالي 550 ألف حالة جديدة كل عام في البلاد. كما تبلغ البلاد عن حوالي 287 ألف حالة وفاة بسبب قصور القلب كل عام.CVD) is one of the leading causes of death across the world. A few main contributors that are increasing the prevalence of CVD and stroke are family history, ethnicity, and age. The prevalence of CVD is also growing due to tobacco use; high blood pressure (hypertension); high cholesterol; exercise lack; unhealthy diet; excessive alcohol consumption; and diseases such as dyslipidemia, obesity, and diabetes. As per the American Heart Association, ~41.4% of adults in the US will have hypertension by 2030 (an 8.4% increase from 2012). The organization also estimates that the global cost burden of CVD will reach US$ 1,044 billion by 2030, which was US$ 863 billion in 2010. Moreover, according to the WHO estimates, deaths due to CVD across the world will rise from ~17.9 million in 2016 to 23.6 million by 2030. Emory Healthcare report states that the US recorded ~5 million cases of congestive failure in 2022, and ~550,000 new cases were diagnosed every year in the country. Also, the country reports ~287,000 deaths due to heart failure every year.

وفقًا لـ Temple Health، تلقى 70.9% من المرضى عمليات زرع قلب في غضون عام، وكان متوسط أقصر قائمة انتظار 55.2% في الولايات المتحدة في عام 2021. أدى تزايد قائمة انتظار زراعة القلب على مستوى العالم إلى دفع استخدام أجهزة مساعدة البطين الأيسر (LVADs) لمرضى قصور القلب في المرحلة النهائية لزيادة نسبة القذف ومنع فشل الأعضاء. لذلك، فإن الانتشار المتزايد لأمراض القلب والأوعية الدموية وفشل القلب وقائمة الانتظار الطويلة لزراعة القلب تدفع إلى اعتماد أجهزة مساعدة البطين الأيسر، مما يدفع نمو سوق أجهزة مساعدة البطين الأيسر.waitlist average was 55.2% in the US in 2021. The increasing the heart transplant waiting list globally has propelled the use of left ventricular assist devices (LVADs) for end-stage heart failure patients to increase the ejection fraction and prevent organ failure. Therefore, the rising prevalence of CVD and heart failure and the long waiting list for a heart transplant propel the adoption of LVADs, which drives the growth of the left ventricular assist devices market.

نوع من الرؤى المستندة إلى التدفق

بناءً على نوع التدفق، يتم تقسيم سوق أجهزة مساعدة البطين الأيسر العالمية إلى نبضية وغير نبضية. في عام 2021، استحوذت الشريحة غير النبضية على حصة سوقية أكبر، ومن المتوقع أيضًا أن تسجل معدل نمو سنوي مركب أعلى في السوق خلال الفترة 2022-2028.pulsatile and non-pulsatile. In 2021, the non-pulsatile segment accounted for a larger market share, and it is further expected to register a higher CAGR in the market during 2022–2028.

رؤى مبنية على التصميم

بناءً على التصميم، ينقسم سوق أجهزة مساعدة البطين الأيسر إلى أجهزة مساعدة البطين القابلة للزرع وأجهزة مساعدة البطين عبر الجلد. احتل قطاع أجهزة مساعدة البطين القابلة للزرع حصة سوقية أكبر في عام 2021 ومن المتوقع أن يسجل معدل نمو سنوي مركب أعلى خلال الفترة المتوقعة.transcutaneous ventricular assist devices. The implantable ventricular assist devices segment held a larger market share in 2021 and is anticipated to register a higher CAGR during the forecast period.

رؤى قائمة على التطبيق

بناءً على التطبيق، يتم تقسيم سوق أجهزة مساعدة البطين الأيسر إلى علاج الوجهة، وجسر الزرع، وجسر الترشيح، وجسر التعافي. احتل قطاع العلاج الوجهة أكبر حصة سوقية في عام 2021 ومن المتوقع أن يسجل أعلى معدل نمو سنوي مركب خلال الفترة المتوقعة.

يتبنى لاعبو سوق أجهزة مساعدة البطين الأيسر استراتيجيات عضوية مثل إطلاق المنتجات، والموافقة على المنتجات، والتوسع لتوسيع نطاق وجودهم ومحفظة منتجاتهم في جميع أنحاء العالم وتلبية الطلب المتزايد. في يونيو 2020، أعلنت شركة Abiomed عن موافقة إدارة الغذاء والدواء الأمريكية (FDA) على طلب إعفاء جهازها التجريبي لبدء دراسة جدوى مبكرة مع أول تجربة بشرية لمضخة القلب Impella ECP.

رؤى مبنية على الجغرافيا

من حيث الجغرافيا، يتم تقسيم سوق جهاز مساعدة البطين الأيسر إلى أمريكا الشمالية (الولايات المتحدة وكندا والمكسيك)، وأوروبا (فرنسا وألمانيا والمملكة المتحدة وإسبانيا وإيطاليا وبقية أوروبا)، وآسيا والمحيط الهادئ (الصين والهند واليابان وأستراليا وكوريا الجنوبية وبقية دول آسيا والمحيط الهادئ)، والشرق الأوسط وأفريقيا (المملكة العربية السعودية والإمارات العربية المتحدة وجنوب أفريقيا وبقية دول الشرق الأوسط وأفريقيا)، وأمريكا الجنوبية والوسطى (البرازيل والأرجنتين وبقية دول أمريكا الجنوبية والوسطى).

رؤى إقليمية حول سوق أجهزة مساعدة البطين الأيسر

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق أجهزة مساعدة البطين الأيسر طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق أجهزة مساعدة البطين الأيسر والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق جهاز مساعدة البطين الأيسر

نطاق تقرير سوق جهاز مساعدة البطين الأيسر

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2021 | 1.27 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 1.81 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2021 - 2028) | 5.1% |

| البيانات التاريخية | 2019-2020 |

| فترة التنبؤ | 2022-2028 |

| القطاعات المغطاة |

حسب نوع التدفق

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

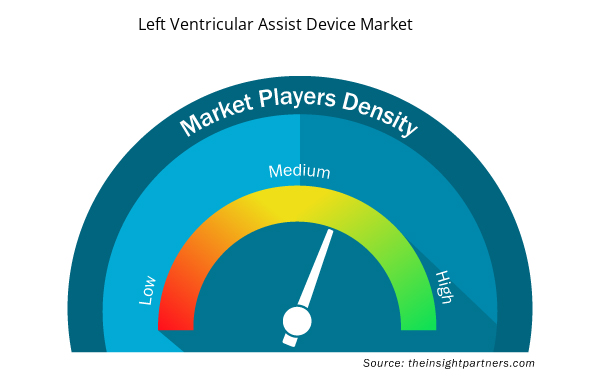

كثافة اللاعبين في سوق أجهزة مساعدة البطين الأيسر: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق أجهزة مساعدة البطين الأيسر نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي الأكبر بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق جهاز مساعدة البطين الأيسر هي:

- شركة أبيوميد

- مختبرات أبوت

- شركة ميدترونيك المحدودة

- شركة ليفانوفا المحدودة

- جارفيك هارت إنك

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق أجهزة مساعدة البطين الأيسر

رؤى مستندة إلى الشركة

تعد شركة ABIOMED Inc، وAbbott Laboratories، وMedtronic Plc، وLivaNova Plc، وJarvik Heart Inc، وTerumo Corp، وBerlin Heart GmbH، وBiVACOR Inc، وEvaheart Inc، وBioVentrix Inc من بين الشركات الرائدة العاملة في سوق جهاز مساعدة البطين الأيسر.

مرينال محللة أبحاث مخضرمة، تتمتع بخبرة تزيد عن 8 سنوات في مجال استخبارات واستشارات سوق علوم الحياة. بفضل عقليتها الاستراتيجية والتزامها الراسخ بالتميز، اكتسبت خبرة واسعة في التنبؤ بالصناعات الدوائية، وتقييم فرص السوق، وتطوير معايير الصناعة. يرتكز عملها على تقديم رؤى عملية تُمكّن العملاء من اتخاذ قرارات استراتيجية مدروسة.

تكمن قوة مرينال الأساسية في ترجمة مجموعات البيانات الكمية المعقدة إلى معلومات استخباراتية قيّمة. وتُعدّ براعتها التحليلية ركيزةً أساسيةً في صياغة استراتيجيات دخول السوق (GTM) واكتشاف فرص النمو في قطاعي الأدوية والأجهزة الطبية. وبصفتها مستشارةً موثوقةً، تُركز مرينال باستمرار على تبسيط إجراءات سير العمل وترسيخ أفضل الممارسات، مما يُعزز الابتكار والكفاءة التشغيلية لعملائها.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق أجهزة مساعدة البطين الأيسر

احصل على عينة مجانية ل - سوق أجهزة مساعدة البطين الأيسر