نمو سوق أجهزة الوقاية من العدوى وتطهير الجروح قبل الجراحة، والحجم، والمشاركة، والاتجاهات، وتحليل اللاعبين الرئيسيين، والتوقعات حتى عام 2028

البيانات التاريخية : 2019-2020 | سنة الأساس : 2021 | فترة التنبؤ : 2022-2028توقعات سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح حتى عام ٢٠٢٨ - تأثير جائحة كوفيد-١٩ والتحليل العالمي حسب المنتج (أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح قبل الجراحة)، والجراحة (جراحة الساد، والجراحة القيصرية، وتجاوز المعدة، واستئصال الزائدة الدودية، واستئصال القولون وفغر القولون، واستئصال المريء، والخزعة، واستئصال المرارة، واستئصال الثدي، وجراحة التجميل، وغيرها)، والتطبيق (إزالة الشعر قبل الجراحة، وتحضير الجلد قبل الجراحة، ومحلول غسل الجروح أثناء الجراحة، وغيرها).

- تاريخ التقرير : Dec 2022

- رمز التقرير : TIPRE00029801

- الفئة : علوم الحياة

- الحالة : نُشرت

- تنسيقات التقارير المتاحة :

- عدد الصفحات : 281

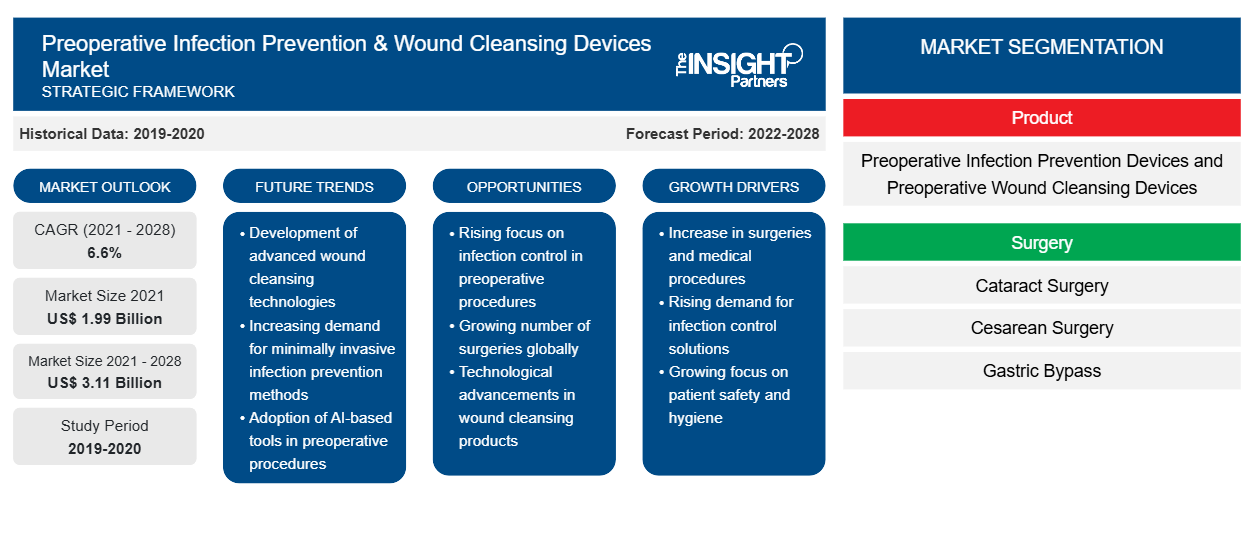

من المتوقع أن ينمو سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح من 1،994.75 مليون دولار أمريكي في عام 2021 إلى 3،112.36 مليون دولار أمريكي بحلول عام 2028؛ ومن المتوقع أن ينمو بمعدل نمو سنوي مركب قدره 6.6٪ من عام 2022 إلى عام 2028.

يتم تقسيم سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح على أساس المنتج والجراحة والتطبيق والمناطق. يقدم التقرير رؤى وتحليلات متعمقة للسوق، مع التركيز على معايير مختلفة مثل الديناميكيات والاتجاهات والفرص في السوق وتحليل المنافسة للاعبين الرئيسيين في السوق عبر مناطق مختلفة. كما يتضمن تحليل تأثير جائحة كوفيد-19 عبر المناطق.

رؤى السوق

ارتفاع معدل الإصابة بالعدوى المكتسبة من المستشفيات يدفع نمو السوق

تشكل المرافق الصحية في مختلف البلدان النامية مثل الهند واليابان خطرًا على المرضى من حيث الإصابة بالعدوى. ففي المستشفيات، تتسبب العدوى في معاناة غير ضرورية ووفاة الملايين من المرضى كل عام. وتعد منطقة آسيا والمحيط الهادئ مصدرًا للأمراض المعدية الناشئة، بما في ذلك الكائنات الحية المقاومة للأدوية المتعددة (MDROs) ومسببات الأمراض ذات القدرة على التسبب في الأوبئة. إن مخاطر الأمراض المعدية الناشئة في المنطقة معقدة ويُعتقد أنها تنطوي على عمليات بيئية واجتماعية واقتصادية وتكنولوجية تفضل ديناميكيات انتقال الميكروبات. ووفقًا لتقديرات المعاهد الوطنية للصحة، فإن خطر الإصابة بالعدوى المكتسبة من المستشفيات (HAIs) في منطقة آسيا والمحيط الهادئ أعلى بمقدار 2-20 مرة من البلدان المتقدمة، حيث يبلغ ما يصل إلى 25٪ من المرضى في المستشفيات عن الإصابة بالعدوى. ووفقًا لمراكز السيطرة على الأمراض والوقاية منها (CDC)، في الولايات المتحدة، يعاني حوالي 1 من كل 31 مريضًا في المستشفيات من عدوى مكتسبة من المستشفيات واحدة على الأقل في أي يوم. وفقًا للبيانات المقدمة من PatientCareLink، في المستشفيات الأمريكية وحدها، تتسبب العدوى المرتبطة بالرعاية الصحية في ما يقدر بنحو 1.7 مليون حالة إصابة و99000 مرض مرتبط بها كل عام، منها 22% عبارة عن عدوى في موقع الجراحة.

تتمتع المرافق الصحية في البلدان المنخفضة والمتوسطة الدخل بمعدلات عالية بشكل استثنائي من العدوى المرتبطة بالرعاية الصحية، وربما يرجع ذلك إلى التحديات الإضافية في تحقيق السيطرة الفعالة على العدوى، ونقص النظافة في المستشفيات، ونقص الوعي فيما يتعلق بمكافحة العدوى. المرضى الذين يعانون من أمراض خطيرة معرضون للإصابة بالعدوى المرتبطة بالرعاية الصحية في البلدان الصناعية والنامية. وقد أدى ارتفاع حالات العدوى المرتبطة بالرعاية الصحية إلى زيادة الحاجة إلى أجهزة الوقاية من العدوى قبل الجراحة، مما أدى إلى نمو سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح.

قم بتخصيص هذا التقرير ليناسب متطلباتك

ستحصل على تخصيص لأي تقرير - مجانًا - بما في ذلك أجزاء من هذا التقرير، أو تحليل على مستوى الدولة، وحزمة بيانات Excel، بالإضافة إلى الاستفادة من العروض والخصومات الرائعة للشركات الناشئة والجامعات

سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح: رؤى استراتيجية

-

احصل على أهم اتجاهات السوق الرئيسية لهذا التقرير.ستتضمن هذه العينة المجانية تحليلاً للبيانات، بدءًا من اتجاهات السوق وحتى التقديرات والتوقعات.

رؤى قائمة على المنتج

بناءً على المنتج، يتم تقسيم سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح إلى أجهزة الوقاية من العدوى قبل الجراحة وأجهزة تنظيف الجروح قبل الجراحة. يتم تقسيم سوق قطاع أجهزة الوقاية من العدوى قبل الجراحة إلى إمدادات الوقاية من العدوى، وأجهزة التخلص من النفايات الطبية، ومعدات الوقاية من العدوى. في عام 2021، احتل قطاع أجهزة الوقاية من العدوى قبل الجراحة حصة سوقية أكبر. علاوة على ذلك، من المتوقع أن يسجل نفس القطاع معدل نمو سنوي مركب أعلى في السوق خلال الفترة 2022-2028. تتطلب الوقاية من العدوى أثناء الجراحة معدات تقنية وتقنيات جراحية جيدة ونظافة مناسبة. الأساس لذلك هو قسم منظم جيدًا مع عمليات روتينية معروفة تُمارس بشكل عام وجدول زمني واقعي قوي. أصبحت الوقاية من عدوى موقع الجراحة بعد الجراحة أكثر أهمية من أي وقت مضى. لن تقوم مراكز الرعاية الصحية والخدمات الطبية (CMS) بتعويض مرافق الرعاية الصحية عن عدوى موقع الجراحة في جراحات متعددة. تعد العدوى المرتبطة بالرعاية الصحية مصدر قلق كبير ومتزايد لأنظمة الرعاية الصحية.

رؤى مستندة إلى الجراحة

بناءً على الجراحة، يتم تقسيم سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح إلى جراحة إعتام عدسة العين، والجراحة القيصرية، وتجاوز المعدة، واستئصال الزائدة الدودية، واستئصال القولون، واستئصال المريء، والخزعة، واستئصال المرارة، واستئصال الثدي، والجراحة التجميلية، وغيرها. في عام 2021، احتل قطاع الجراحة التجميلية أكبر حصة في السوق. ومع ذلك، من المتوقع أن ينمو سوق قطاع جراحة إعتام عدسة العين بأعلى معدل خلال فترة التوقعات. تشمل الجراحة التجميلية إعادة بناء عيوب الوجه والجسم الناتجة عن الولادة والحروق والأمراض والصدمات. في الهند، زادت شعبية الإجراءات التجميلية بشكل كبير بسبب انتشار السمنة المتزايد، وارتفاع عدد السكان المسنين، والتأثير المتزايد للثقافة الغربية. بالإضافة إلى ذلك، بسبب مناخ البلاد الاستوائي، يتزايد الطلب على علاجات مكافحة الشيخوخة. تعتبر كوريا الجنوبية عاصمة الجراحة التجميلية في منطقة آسيا والمحيط الهادئ. علاوة على ذلك، من المتوقع أن تحافظ على هيمنتها على مدى السنوات القليلة القادمة. على مر السنين، أدى ارتفاع الطلب على عمليات شد الوجه، وارتفاع الإنفاق على التحسينات الجمالية، وتوافر الإجراءات المتقدمة إلى زيادة الطلب على الإجراءات التجميلية في جميع أنحاء كوريا الجنوبية. تعد عدوى الجروح من بين المضاعفات الأكثر شيوعًا بعد الجراحة لدى المرضى الذين يخضعون لجراحة التجميل. من شأن الاستشارة المناسبة قبل الجراحة أن تساعد في تحديد التوقعات الصحيحة وتحسين نتائج المرضى ورضاهم في النهاية.

رؤى قائمة على التطبيق

بناءً على التطبيق، يتم تقسيم سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح إلى إزالة الشعر قبل الجراحة، وتحضير الجلد قبل الجراحة، ومحلول ري الجروح أثناء الجراحة، وغيرها. في عام 2021، احتل قطاع إزالة الشعر قبل الجراحة الحصة الأكبر من السوق. علاوة على ذلك، من المتوقع أن ينمو سوق نفس القطاع بأعلى معدل خلال فترة التنبؤ. وفقًا لإرشادات منظمة الصحة العالمية (WHO)، لا ينبغي إزالة الشعر إلا إذا كان يتعارض مع الجراحة. وفقًا لتقرير Cochrane Collaboration، قبل التدخل الجراحي، من الشائع إزالة الشعر من منطقة الجسم لإجراء الجراحة. تتم إزالة الشعر لتجنب المشاكل أثناء الجراحة وبعدها. على سبيل المثال، أثناء خياطة الجروح أو وضع الضمادات، تزعم الدراسات أن إزالة الشعر يمكن أن يسبب التهابات بعد الجراحة ويجب تجنبها.

أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

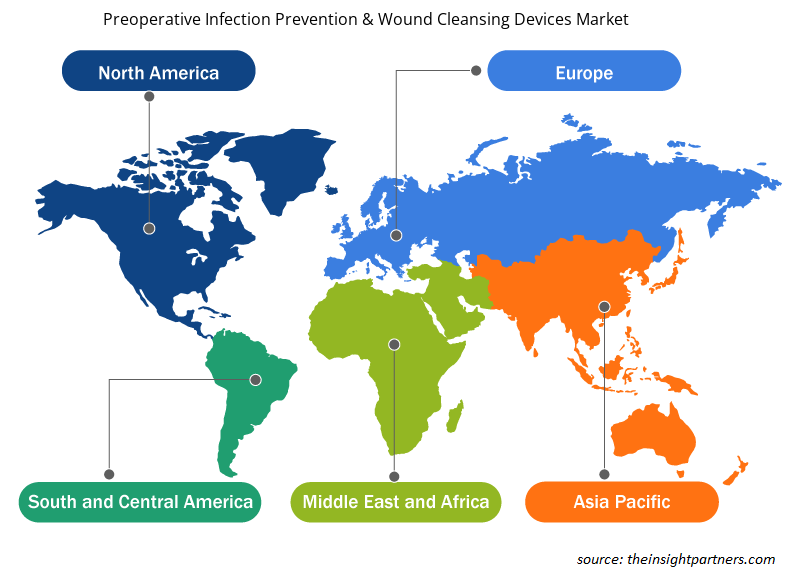

رؤى إقليمية حول سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

لقد قام المحللون في Insight Partners بشرح الاتجاهات والعوامل الإقليمية المؤثرة على سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح طوال فترة التوقعات بشكل شامل. يناقش هذا القسم أيضًا قطاعات سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح والجغرافيا في جميع أنحاء أمريكا الشمالية وأوروبا ومنطقة آسيا والمحيط الهادئ والشرق الأوسط وأفريقيا وأمريكا الجنوبية والوسطى.

- احصل على البيانات الإقليمية المحددة لسوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

نطاق تقرير سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

| سمة التقرير | تفاصيل |

|---|---|

| حجم السوق في عام 2021 | 1.99 مليار دولار أمريكي |

| حجم السوق بحلول عام 2028 | 3.11 مليار دولار أمريكي |

| معدل النمو السنوي المركب العالمي (2021 - 2028) | 6.6% |

| البيانات التاريخية | 2019-2020 |

| فترة التنبؤ | 2022-2028 |

| القطاعات المغطاة |

حسب المنتج

|

| المناطق والدول المغطاة |

أمريكا الشمالية

|

| قادة السوق وملفات تعريف الشركات الرئيسية |

|

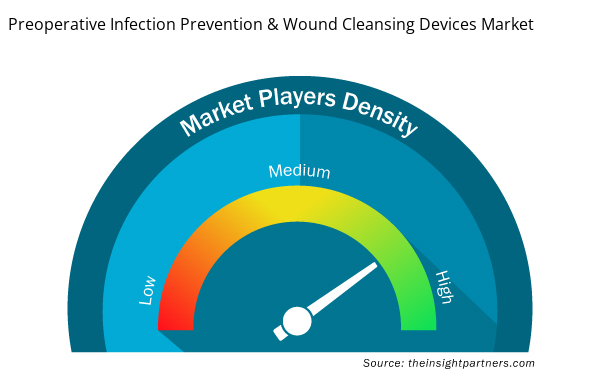

كثافة اللاعبين في سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح: فهم تأثيرها على ديناميكيات الأعمال

يشهد سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح نموًا سريعًا، مدفوعًا بالطلب المتزايد من المستخدم النهائي بسبب عوامل مثل تفضيلات المستهلكين المتطورة والتقدم التكنولوجي والوعي المتزايد بفوائد المنتج. ومع ارتفاع الطلب، تعمل الشركات على توسيع عروضها والابتكار لتلبية احتياجات المستهلكين والاستفادة من الاتجاهات الناشئة، مما يؤدي إلى زيادة نمو السوق.

تشير كثافة اللاعبين في السوق إلى توزيع الشركات أو المؤسسات العاملة في سوق أو صناعة معينة. وهي تشير إلى عدد المنافسين (اللاعبين في السوق) الموجودين في مساحة سوق معينة نسبة إلى حجمها أو قيمتها السوقية الإجمالية.

الشركات الرئيسية العاملة في سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح هي:

- شركة كاردينال هيلث

- شركة 3M

- باكتي جارد ايه بي

- بيكتون ديكنسون وشركاه

- جيتنج ايه بي

إخلاء المسؤولية : الشركات المذكورة أعلاه ليست مرتبة بأي ترتيب معين.

- احصل على نظرة عامة على أهم اللاعبين الرئيسيين في سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

يتبنى اللاعبون في سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح استراتيجيات عضوية، مثل إطلاق المنتجات والتوسع، لتوسيع نطاق وجودهم ومحفظة منتجاتهم في جميع أنحاء العالم وتلبية الطلب المتزايد. وتتمثل استراتيجيات النمو غير العضوية التي شهدها السوق في الشراكات والتعاون. وقد سمحت استراتيجيات النمو هذه للاعبين في السوق بتوسيع أعمالهم وتعزيز حضورهم الجغرافي. بالإضافة إلى ذلك، تساعد عمليات الاستحواذ والشراكات واستراتيجيات النمو الأخرى في تعزيز قاعدة عملاء الشركة وزيادة محفظة منتجاتها.

- في مايو 2021، أعلنت شركة Medline عن إطلاق منتج جديد وهو مناديل ReadyPrep CHG. ويستحوذ هذا المنتج الجديد منذ إطلاقه على حصة 40% من السوق المحلية خلال عامين.

- في أكتوبر 2018،أعلنت شركة 3M عن حل متقدم لتحضير الجلد قبل الجراحة من أجل الاستفادة منه في الوقاية من عدوى المرضى. ويستفيد المنتج الجديد من خبرة شركة 3M في تكنولوجيا البوليمر والمواد اللاصقة في هيئة "فيلم حماية التحضير من 3M". ويتمتع هذا المنتج بقدرة عالية على البقاء على جلد المريض ويمكنه تحمل قسوة الظروف الجراحية المحاكاة، بما في ذلك المسح المتكرر.

نبذة عن الشركة

- شركة كاردينال هيلث

- شركة 3M

- باكتي جارد ايه بي

- بيكتون ديكنسون وشركاه

- جيتنج ايه بي

- شركة بيوميريو المحدودة

- شركة ميدلاين للصناعات

- شركة ديناريكس

- شركة كارون للحلول الصحية المحدودة

- شركة ستيريس المحدودة

مرينال محللة أبحاث مخضرمة، تتمتع بخبرة تزيد عن 8 سنوات في مجال استخبارات واستشارات سوق علوم الحياة. بفضل عقليتها الاستراتيجية والتزامها الراسخ بالتميز، اكتسبت خبرة واسعة في التنبؤ بالصناعات الدوائية، وتقييم فرص السوق، وتطوير معايير الصناعة. يرتكز عملها على تقديم رؤى عملية تُمكّن العملاء من اتخاذ قرارات استراتيجية مدروسة.

تكمن قوة مرينال الأساسية في ترجمة مجموعات البيانات الكمية المعقدة إلى معلومات استخباراتية قيّمة. وتُعدّ براعتها التحليلية ركيزةً أساسيةً في صياغة استراتيجيات دخول السوق (GTM) واكتشاف فرص النمو في قطاعي الأدوية والأجهزة الطبية. وبصفتها مستشارةً موثوقةً، تُركز مرينال باستمرار على تبسيط إجراءات سير العمل وترسيخ أفضل الممارسات، مما يُعزز الابتكار والكفاءة التشغيلية لعملائها.

- التحليل التاريخي (سنتان)، سنة الأساس، التوقعات (7 سنوات) مع معدل النمو السنوي المركب

- تحليل PEST و SWOT

- حجم السوق والقيمة / الحجم - عالمي، إقليمي، بلد

- الصناعة والمنافسة

- مجموعة بيانات إكسل

التقارير الحديثة

شهادات العملاء

تقرير سوق أنظمة SCADA من Insight Partners شامل، ويقدم رؤى قيّمة حول الاتجاهات الحالية والتوقعات المستقبلية. تميّز الفريق باحترافية عالية وسرعة في الاستجابة ودعم مستمر طوال الوقت. نحن راضون جدًا ونوصي بشدة بخدماتهم.

ران كيديم شريك, شركة ريالي تكنولوجيز المحدودةطلبتُ تقريرًا عن سوق برمجيات محدد، وأعدّه الفريق في غضون أيام قليلة. كانت المعلومات ذات صلة وثيقة وعرضها جيد. ثم طلبتُ بعض التعديلات والإضافات على التقرير. وكان الفريق متجاوبًا للغاية، وحصلتُ على التقرير النهائي في أقل من أسبوع.

جان هيرفيه جين رئيس مجلس الإدارة, فيوتشر أناليتيكاعملنا مع شركة "إنسايت بارتنرز" لإجراء دراسة سوقية وتوقعات مهمة. زودونا برؤى واضحة حول الفرص والمخاطر، مما ساعدنا في صياغة خططنا. كانت أبحاثهم سهلة الاستخدام ومبنية على بيانات دقيقة، مما ساعدنا على اتخاذ قرارات ذكية وواثقة. نوصي بهم بشدة.

بيوش ناجبال نائب الرئيس الأول, شعاع عالي عالميقدّمت شركة Insight Partners أبحاثًا سوقية ثاقبة ومنظمة جيدًا بخبرة واسعة في هذا المجال. تميّز فريقهم بالاحترافية وسرعة الاستجابة طوال الوقت. وسهّل موقعهم الإلكتروني سهل الاستخدام الوصول إلى تقارير القطاع. نوصي بهم بشدة لخدمات بحثية موثوقة وعالية الجودة.

يوكيهيكو أداتشي المدير التنفيذي, ديب بلو، ذ.م.م.هذه أول مرة أشتري فيها تقرير سوق من The Insight Partners. رغم أنني كنت مترددًا في البداية، إلا أنني زرت موقعهم الإلكتروني وشعرت براحة أكبر للمخاطرة وشراء تقرير السوق. أنا راضٍ تمامًا عن جودة التقرير وخدمة العملاء. كانت لديّ عدة أسئلة وتعليقات حول التقرير الأولي، ولكن بعد بضع محادثات عبر البريد الإلكتروني مع محللهم، أعتقد أن لديّ تقريرًا يمكنني استخدامه كمدخل لعملية التخطيط الاستراتيجي لدينا. شكرًا جزيلاً لكم على تخصيص وقتكم الإضافي وجعل هذه التجربة إيجابية. سأوصي بخدماتكم للآخرين بالتأكيد، وستكونون أول من ألجأ إليه عندما نحتاج إلى المزيد من بيانات السوق.

جون سوزوكي الرئيس والرئيس التنفيذي وعضو مجلس الإدارة, بي كيه تكنولوجيزأود أن أقدّر دعمكم واحترافيتكم في الاستجابة لطلبي للحصول على معلومات بشأن سوق التشخيص المخبري للأمراض المعدية في نيجيريا. كما أُقدّر صبركم وتوجيهكم، واستعدادكم لتقديم خصم، مما مكّننا في النهاية من إتمام الصفقة. أتطلع إلى التعامل مع "ذا إنسايت بارتنرز" مستقبلًا، كل ذلك بفضل الانطباع الذي تركتموه لديّ نتيجةً لهذا اللقاء الأول.

الدكتور تشيجيوك أونيا المدير الإداري, شركة باينكريست للرعاية الصحية المحدودةسبب الشراء

- اتخاذ قرارات مدروسة

- فهم ديناميكيات السوق

- تحليل المنافسة

- رؤى العملاء

- توقعات السوق

- تخفيف المخاطر

- التخطيط الاستراتيجي

- مبررات الاستثمار

- تحديد الأسواق الناشئة

- تحسين استراتيجيات التسويق

- تعزيز الكفاءة التشغيلية

- مواكبة التوجهات التنظيمية

احصل على عينة مجانية ل - سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح

احصل على عينة مجانية ل - سوق أجهزة الوقاية من العدوى قبل الجراحة وتنظيف الجروح