Analystenperspektive:

In Europa verzeichnete Italien mit 4,4 % den höchsten CAGR, gefolgt vom Vereinigten Königreich und Deutschland, was auf die schnell wachsende Nachfrage nach Möbeln und Sperrholz zurückzuführen ist Holzprodukte für Wohnzwecke im Jahr 2022. Nach Angaben der Europäischen Kommission stiegen die italienischen Möbelexporte um 25,7 %, was im Jahr 2022 im Vergleich zu 2021 einem Wert von rund 53,5 Millionen US-Dollar entspricht.

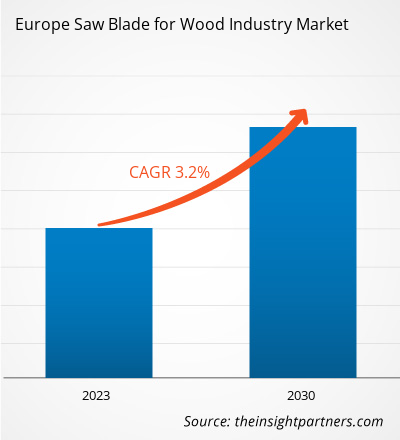

Der Sägeblattmarkt nimmt eine herausragende Stellung ein Europäische Wirtschaft. Holz wird in Europa vor allem für die Energieerzeugung, Möbel und Bodenbeläge bevorzugt. Die Region ist für etwa 5 % der weltweiten Wälder verantwortlich. Wälder sind neben ihrem ökologischen Wert auch eine wirtschaftliche Ressource. Ungefähr 60 % der Waldflächen befinden sich in Privatbesitz, während 40 % in Europa öffentlicher Hand sind. Infolgedessen ist die Kommerzialisierung von Holz im Vergleich zu jeder anderen Region höher. Darüber hinaus steht ein Großteil der Wälder der EU (85 %) für die Holzversorgung zur Verfügung, was eine entscheidende Komponente der Funktion des Waldes bei der Schaffung von Einnahmen, der Beschäftigung und dem Übergang zur Bioökonomie darstellt. Dies hat den Herstellern von Holzprodukten geholfen, Holzprodukte ohne Schwankungen in der Rohstoffversorgung herzustellen.

Marktübersicht:

Sägeblätter sind austauschbare gezahnte Schneidkomponenten, die in vielen handgehaltenen Geräten sowie in tragbaren und stationären Geräten verwendet werden Werkzeuge. Die Holzindustrie in Europa ist eine der bemerkenswertesten Branchen, da sie einen erheblichen Teil der Wirtschaft der Region generiert. Den von Eurostat im Jahr 2022 bereitgestellten Daten zufolge belief sich die Bruttowertschöpfung (BWS) der Holzindustrie in der EU im Jahr 2020 auf 167,04 Milliarden US-Dollar, was 7,2 % der gesamten verarbeitenden Industrie entspricht. Im Jahr 2020 betrug die Bruttowertschöpfung der Produktion von Holz und Holzprodukten 37 Milliarden Euro. Die höchste BWS in der holzbasierten Industrie der EU wurde für Zellstoff, Papier und die Herstellung von Papierprodukten gemeldet (34 %). Druck und druckbezogene Dienstleistungsaktivitäten machten 16 % der BWS der Holzindustrie aus, während die Möbelherstellung und die Herstellung von Holz und Holzprodukten jeweils zwischen 23 % und 27 % ausmachten.

Holz wird hauptsächlich in der Holzindustrie verwendet Bauindustrie in Form von Schnittholz und Holzplatten. Die Nachfrage nach Schnittholz und Holzplatten steigt in Europa aufgrund des Wachstums in der Bauindustrie. Nach Angaben der Europäischen Organisation der Sägeindustrie (EOS) aus dem Jahr 2022 erreichte die Produktion im Jahr 2021 in den EOS-Mitgliedsländern ein Allzeithoch. Die Schnittholzproduktion betrug im Jahr 2021 86 Millionen Kubikmeter. Meter. Darüber hinaus ist das kontinuierliche Wachstum in der Zellstoff- und Papierindustrie ein weiterer Faktor, der die Nachfrage nach Holz und Holzverarbeitungswerkzeugen in Europa antreibt. Den von der europäischen Regierung veröffentlichten Daten zufolge erreichte die Zellstoff- und Papierindustrie in der Region im Jahr 2022 130.226 Millionen US-Dollar, ein Anstieg von 21 % gegenüber 2020. Dies ist auf die steigende Nachfrage nach Holz in der Bau-, Papier- und Zellstoffbranche zurückzuführen Industrien steigt der Bedarf an Holzverarbeitungswerkzeugen, was letztendlich den Sägeblattmarkt in der europäischen Holzindustrie befeuert.

Markttreiber:

Die gestiegene Nachfrage nach Holzprodukten in der Bauindustrie treibt das Sägeblatt an für das Marktwachstum in der Holzindustrie

Die Bauindustrie ist die bedeutendste Branche in Europa und macht 9 % des gesamten europäischen BIP aus. Den von der Europäischen Union im Jahr 2019 bereitgestellten Daten zufolge hat die Bauindustrie in Europa einen Mehrwert von ca. 615 Milliarden US-Dollar geschaffen. Die wachsende Nachfrage nach Wohnhochhäusern ist einer der treibenden Faktoren für die Bauindustrie auf dem europäischen Markt. So verzeichnete Deutschland im Jahr 2020 einen Umsatz von 175 Milliarden US-Dollar, während der Umsatz der französischen Bauindustrie im Jahr 2020 bei 540 Milliarden US-Dollar lag. Die Bauindustrie ist ein wichtiger Teil der französischen Wirtschaft. Es hält mehr als 25 % der Gesamtinvestitionen und 5 % des BIP des Landes.

Nach Angaben der European Panel Federation (EPF) erreichte die Produktion von Holzwerkstoffplatten 65 Millionen Kubikmeter. Meter im Vergleich zu 2020 und 2019, der unter 60 Millionen Kubikmeter lag. Meter. Die Holzplattenproduktionsindustrie verzeichnete im Jahr 2021 ein Wachstum von 10 %. Darüber hinaus entfielen laut der European Panel Federation im Jahr 2022 38 % des gesamten Holzplattenverbrauchs auf die Bauindustrie Das kontinuierliche Wachstum in der Bauindustrie hat die Nachfrage nach Holzbearbeitungswerkzeugen wie Sägeblättern auf dem europäischen Sägeblattmarkt erhöht.

Segmentanalyse:

Das Produkttypsegment der Sägeblätter für den Holzindustriemarkt umfasst Sägeblätter, die verwendet werden in verschiedenen Arten von Sägewerkzeugen, wie Kreissägewerkzeugen, Bandsägemaschinen und Hackmessern. Es wird erwartet, dass Kreissägen im Prognosezeitraum den Sägeblattmarkt dominieren werden. Der Motor der Kreissäge dreht das Sägeblatt mit hoher Geschwindigkeit, sodass die Zähne mühelos durch Materialien schneiden können. Die hohe Marktdurchdringung von Kreissägen und kontinuierliche Produktentwicklungsaktivitäten gehören zu den Faktoren, die das Marktwachstum von Kreissägen vorantreiben. Die steigende Rundholzproduktion in den europäischen Ländern treibt den Markt für Sägeblätter für die Holzindustrie voran. Laut einem Bericht der Europäischen Kommission erreichte die Rundholzproduktion im Jahr 2022 510 Millionen Kubikmeter. Meter, ein Wachstum von 26 % im Zeitraum 2000 bis 2022. Das größte geerntete Holz gibt es in den Niederlanden, Tschechien, Slowenien und Polen. Außerdem war Deutschland im Jahr 2022 mit 79 Millionen Kubikmetern der größte Rundholzproduzent in der Europäischen Union. Meter, gefolgt von Finnland und Schweden mit 77 Millionen Kubikmetern. Meter und 66 Millionen Kubikmeter. Meter bzw. Die steigende Produktion von Rundholz hat zu einer enormen Nachfrage nach Kreissägeblättern im Sägeblattmarkt geführt.

Regionale Analyse:

In Europa hat Deutschland den größten Anteil an der Produktion von Rundholz für den Wohn- und Bausektor. Laut dem Organisationsbericht der Europäischen Kommission war Deutschland im Jahr 2022 mit rund 79 Millionen Kubikmetern die größte Produktion. Meter Rundholz, gefolgt von Finnland und Schweden mit einer Produktion von 77 Millionen Kubikmetern. Meter und 66 Millionen Kubikmeter. Meter Rundholz bzw. Die Produktion von Rundholz erfordert den Einsatz von Sägeblättern in großer Zahl, was wiederum den Sägeblattmarkt für die Holzindustrie in Europa antreibt.

Key-Player-Analyse:

Robert Rontgen GmbH, SNA Europe, Wespa Metallsagenfabrik Simonds Industries, Koll & Cie GmbH & Co. KG., Säge- und Werkzeugfabrik WAPIENICA Sp Zoo, RUKO GmbH, FABA SA, Aspi Spolka ZOO Spolka Komandytowa, Kanefusa Europe BV, Pilana Wood SRO, Ake Knebel GmbH & Co KG, Ledermann GmbH & Co KG, Metabowerke GmbH, GDA SRL, TKM Austria GmbH und Leitz GmbH & Co KG gehören zu den führenden Sägeblättern für die Holzindustrie-Marktteilnehmern im Sägeblattmarkt.

Neueste Entwicklungen:

Anorganische und organische Strategien B. Fusionen und Übernahmen, werden von Unternehmen auf dem Sägeblattmarkt in hohem Maße übernommen, um der wachsenden Kundennachfrage gerecht zu werden. Die auf dem Sägeblattmarkt vertretenen Marktteilnehmer für Sägeblätter für die Holzindustrie konzentrieren sich hauptsächlich auf Produkt- und Serviceverbesserungen durch die Integration fortschrittlicher Funktionen und Technologien in ihre Angebote. Nachfolgend sind einige aktuelle Entwicklungen der wichtigsten Akteure auf dem Sägeblattmarkt aufgeführt:

Jahr

Neuigkeiten

Okt. 2020

Shenzhen Welldon Tools Co., Ltd. hat Diamantsägeblätter für den nationalen und internationalen Schnitzmarkt auf den Markt gebracht im September. Der Durchmesser der Klinge beträgt 200 mm. Schärfe und Haltbarkeit wurden deutlich verbessert, um die Arbeitsintensität der Arbeiter zu reduzieren und gleichzeitig Kosten für Geschäftsinhaber zu sparen.

Okt. 2023

Die Serie wurde von Engr. entwickelt. Giorgio Pozzo, Gründer von Freud und Designer der Diablo-Sägeblattlinie. ITK X-Treme Chorme ist das einzige voll ausgestattete Sägeblatt in Premium-Industriequalität auf dem Markt, das zum gleichen Mittelpreis angeboten wird wie die Sägeblätter der Konkurrenz.

- Historische Analyse (2 Jahre), Basisjahr, Prognose (7 Jahre) mit CAGR

- PEST- und SWOT-Analyse

- Marktgröße Wert/Volumen – Global, Regional, Land

- Branche und Wettbewerbsumfeld

- Excel-Datensatz

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Häufig gestellte Fragen

In Europe, Germany has the largest share in the production of roundwood for the residential and construction sector. According to the European Commission Organization Report in 2022, Germany was the largest production of around 79 million m3 of roundwood followed by Finland and followed by Sweden producing 77 and 66 million m3 of round wood. These roundwood production requires saw blades in huge amount which drives the saw blade market in Europe for the wood industry.

The construction industry is the notable industry in Europe, accounting for 9% of the total Europe's GDP. As per the data provided by the European Union in 2019, the construction industry added a value of ~US$ 615 billion in Europe. Growing demand for high-rise residential construction is one of the factors driving the construction industry in the European market.

The adoption of wooden pallets in the region is more common compared to plastic pallets due to increased awareness about sustainability. Further, the demand for wood pallets and packaging is increasing mainly due to continuous growth in the retail and e-commerce industry. The retail industry is the most important industrial ecosystem, accounting for 11.5% of the total European Union value added.

Robert Rontgen GmbH, SNA Europe, Wespa Metallsagenfabrik Simonds Industries, RUKO GmbH, GDA srl, and Leitz GmbH & Co KG are the top key market players operating in the Europe saw blade for wood industry market.

The manufacturing of saw blades in its early days included smelting copper and casting it in a blade cast. However, as the technology improved, copper was replaced by steel. In the modern era, many saw blade and tool manufacturers are focusing on undertaking research and development strategies to develop innovative blade materials that are more efficient and effective for working in diverse conditions.

Trends and growth analysis reports related to Manufacturing and Construction : READ MORE..

The List of Companies - Europe Saw Blade for Wood Industry Market

- Robert Rontgen GmbH

- SNA Europe

- Wespa Metallsagenfabrik Simonds Industries

- Koll & Cie GmbH & Co. KG.

- Saw and Tool Factory WAPIENICA Sp Zoo

- RUKO GmbH

- FABA SA

- Aspi Spolka ZOO Spolka Komandytowa

- Kanefusa Europe BV

- Leitz GmbH & Co KG

- Pilana Wood SRO

- Ake Knebel GmbH & Co KG

- Ledermann GmbH & Co KG

- Metabowerke GmbH

- GDA SRL

- TKM Austria GmbH

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Holen Sie sich ein kostenloses Muster für diesen Bericht

Holen Sie sich ein kostenloses Muster für diesen Bericht