Demanda, participación y pronóstico del mercado de dispositivos de artroscopia para 2034

Tamaño y pronóstico del mercado de dispositivos de artroscopia (2021-2034), participación global y regional, tendencias y análisis de oportunidades de crecimiento. Cobertura del informe: por producto (artroscopios, implantes artroscópicos, sistemas de gestión de fluidos, sistemas de radiofrecuencia (RF), sistemas de afeitado motorizado, sistemas de visualización, otros equipos artroscópicos); aplicación/tipo de artroscopia (artroscopia de rodilla, artroscopia de cadera, artroscopia de hombro y codo, artroscopia de columna, artroscopia de pie y tobillo/articulaciones pequeñas y otras); y geografía.

- Estado : Datos publicados

- Código de informe : TIPRE00020213

- Categoría : Ciencias de la vida

- Número de páginas : 150

- Formatos de informe disponibles :

- Fecha de última actualización : January 23, 2026

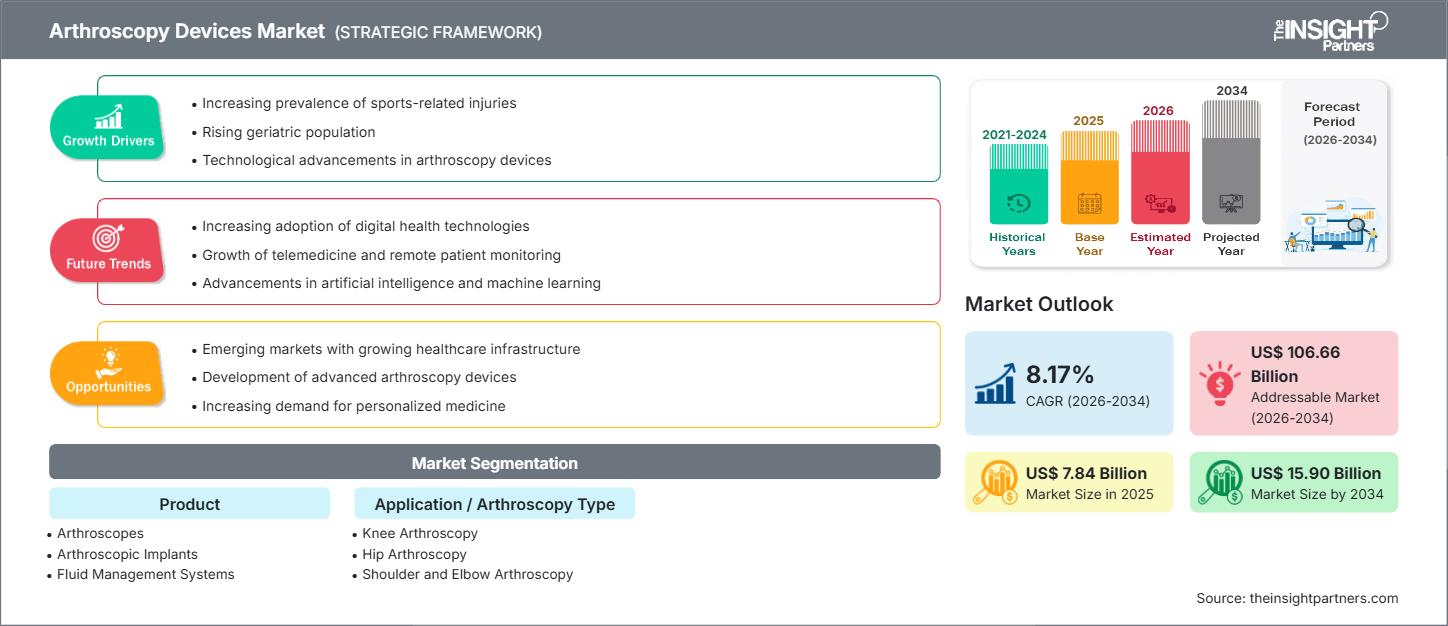

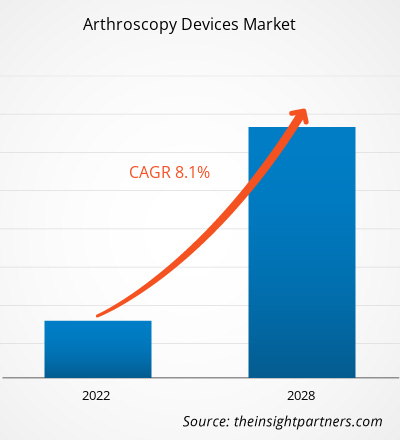

El tamaño del mercado de dispositivos de artroscopia se valoró en US$ 7,84 mil millones en 2025 y se espera que alcance los US$ 15,90 mil millones en 2034, creciendo a una CAGR del 8,17% entre 2026 y 2034.

Análisis del mercado de dispositivos de artroscopia

El crecimiento del mercado de dispositivos de artroscopia está impulsado por una creciente prevalencia de trastornos musculoesqueléticos, una creciente incidencia de lesiones articulares relacionadas con el deporte y una creciente preferencia por procedimientos quirúrgicos mínimamente invasivos.

Los avances en la tecnología quirúrgica, como los sistemas mejorados de visualización artroscópica, los instrumentos motorizados, los sistemas de radiofrecuencia y los implantes biocompatibles, están mejorando los resultados de los procedimientos, reduciendo los tiempos de recuperación y promoviendo una adopción más amplia de procedimientos artroscópicos a nivel mundial.

Además, la expansión de la infraestructura ortopédica, el aumento del gasto sanitario y el crecimiento de la población geriátrica (que es más propensa a sufrir trastornos articulares) respaldan la demanda a largo plazo de dispositivos de artroscopia.

Descripción general del mercado de dispositivos de artroscopia

Los dispositivos de artroscopia se refieren a un amplio conjunto de instrumentos y sistemas médicos utilizados para realizar procedimientos artroscópicos, cirugías mínimamente invasivas para diagnosticar y tratar afecciones articulares. Estos dispositivos incluyen artroscopios, sistemas de visualización, sistemas de gestión de fluidos, sistemas de radiofrecuencia (RF), sistemas de afeitado eléctrico, implantes artroscópicos, taladros y sistemas de fijación, y otros equipos relacionados.

Estas herramientas permiten a los cirujanos ortopédicos visualizar el interior de las articulaciones, ejecutar intervenciones reparadoras (por ejemplo, reparación de ligamentos, restauración de cartílago, reparación de meniscos), gestionar la irrigación y el flujo de líquidos e implantar hardware de estabilización, todo ello mientras minimizan el traumatismo tisular y permiten una recuperación más rápida.

Los dispositivos de artroscopia desempeñan un papel fundamental en una variedad de articulaciones, incluidas la rodilla, la cadera, el hombro, la columna, el pie/tobillo y las articulaciones más pequeñas, lo que ayuda a los médicos a brindar una atención eficaz y menos invasiva en hospitales, centros quirúrgicos ambulatorios (ASC), clínicas ortopédicas y centros especializados.

Personalice este informe según sus necesidades

Obtenga PERSONALIZACIÓN GRATUITAMercado de dispositivos de artroscopia: Perspectivas estratégicas

-

Obtenga las principales tendencias clave del mercado de este informe.Esta muestra GRATUITA incluirá análisis de datos, desde tendencias del mercado hasta estimaciones y pronósticos.

Impulsores y oportunidades del mercado de dispositivos de artroscopia

Factores impulsores del mercado:

- Aumento de la incidencia de trastornos musculoesqueléticos y lesiones articulares: los crecientes casos de osteoartritis, desgarros de ligamentos, daños meniscales y lesiones relacionadas con el deporte impulsan la demanda de intervenciones artroscópicas y dispositivos relacionados.

- Preferencia por la cirugía mínimamente invasiva (CMI): los cirujanos y los pacientes prefieren cada vez más la artroscopia a la cirugía articular abierta debido a beneficios como incisiones más pequeñas, menor riesgo, recuperación más rápida y menor estadía en el hospital.

- Avances tecnológicos en equipos artroscópicos: las innovaciones, que incluyen sistemas de visualización de alta definición, afeitadores motorizados, gestión avanzada de fluidos, implantes bioabsorbibles y metálicos y sistemas de radiofrecuencia, mejoran la precisión quirúrgica, los resultados de los pacientes y amplían el alcance de las afecciones articulares tratables.

- Creciente infraestructura ortopédica e inversión en atención médica: la expansión de hospitales, centros quirúrgicos ambulatorios y clínicas especializadas en ortopedia, particularmente en las economías emergentes, aumenta la accesibilidad a los procedimientos artroscópicos.

Oportunidades:

- Expansión en mercados emergentes: Regiones como Asia-Pacífico (incluidos países como India y China) muestran un fuerte potencial de crecimiento debido a las crecientes inversiones en atención médica, la creciente conciencia de los procedimientos mínimamente invasivos, el aumento de las lesiones deportivas entre las poblaciones más jóvenes y una creciente población de ancianos susceptibles a los trastornos articulares.

- Innovación y diferenciación de productos: el desarrollo de implantes de última generación, sistemas de visualización mejorados, dispositivos portátiles de gestión de fluidos y herramientas RF/motorizadas avanzadas permite a los fabricantes de dispositivos ofrecer soluciones de valor agregado y, potencialmente, capturar una mayor participación de mercado.

- Crecimiento de los centros quirúrgicos ambulatorios (ASCs) y de los procedimientos ambulatorios mínimamente invasivos: a medida que los ASCs se expanden globalmente, es probable que crezca la demanda de dispositivos de artroscopia optimizados para entornos ambulatorios (sistemas compactos, eficientes y de menor costo).

- Aumento de la demanda de reparación y rehabilitación de articulaciones debido al envejecimiento de la población: el aumento mundial de la población anciana propensa a la osteoartritis, enfermedades articulares degenerativas, impulsa la demanda a largo plazo de dispositivos e intervenciones artroscópicas.

Análisis de segmentación del mercado de dispositivos de artroscopia

El mercado suele segmentarse en múltiples dimensiones de la siguiente manera:

Por producto:

- Artroscopios

- Implantes artroscópicos

- Sistemas de gestión de fluidos

- Sistemas de radiofrecuencia (RF)

- Sistemas de afeitado eléctrico

- Sistemas de visualización

- Otros equipos artroscópicos

Por aplicación / tipo de artroscopia:

- Artroscopia de rodilla

- Artroscopia de cadera

- Artroscopia de hombro y codo

- Artroscopia de columna

- Artroscopia de pie y tobillo / Pequeñas articulaciones y otras

Por geografía:

- América del norte

- Europa

- Asia-Pacífico

- Oriente Medio y África

- América del Sur y Central / América Latina

Perspectivas regionales del mercado de dispositivos de artroscopia

Los analistas de The Insight Partners han explicado detalladamente las tendencias regionales y los factores que influyen en el mercado de dispositivos de artroscopia durante el período de pronóstico. Esta sección también analiza los segmentos y la geografía del mercado de dispositivos de artroscopia en América del Norte, Europa, Asia Pacífico, Oriente Medio y África, y América del Sur y Central.

Alcance del informe de mercado de dispositivos de artroscopia

| Atributo del informe | Detalles |

|---|---|

| Tamaño del mercado en 2025 | US$ 7.84 mil millones |

| Tamaño del mercado en 2034 | US$ 15.90 mil millones |

| CAGR global (2026-2034) | 8,17% |

| Datos históricos | 2021-2024 |

| Período de pronóstico | 2026-2034 |

| Segmentos cubiertos |

Por producto

|

| Regiones y países cubiertos |

América del norte

|

| Líderes del mercado y perfiles de empresas clave |

|

Densidad de actores del mercado de dispositivos de artroscopia: comprensión de su impacto en la dinámica empresarial

El mercado de dispositivos de artroscopia está creciendo rápidamente, impulsado por la creciente demanda de los usuarios finales debido a factores como la evolución de las preferencias de los consumidores, los avances tecnológicos y un mayor conocimiento de los beneficios del producto. A medida que aumenta la demanda, las empresas amplían su oferta, innovan para satisfacer las necesidades de los consumidores y aprovechan las tendencias emergentes, lo que impulsa aún más el crecimiento del mercado.

- Obtenga una descripción general de los principales actores clave del mercado de dispositivos de artroscopia

Análisis de la cuota de mercado de dispositivos de artroscopia por geografía

- En la actualidad, América del Norte ocupa una participación líder en el mercado de dispositivos de artroscopia, respaldada por una infraestructura de atención médica avanzada, una alta adopción de procedimientos ortopédicos mínimamente invasivos, una gran población geriátrica y deportista activa y políticas de reembolso favorables.

- Europa sigue siendo un mercado clave debido a la creciente incidencia de osteoartritis y enfermedades articulares degenerativas, sistemas de atención sanitaria bien establecidos y una creciente demanda de reparaciones articulares mínimamente invasivas.

- Se proyecta que Asia-Pacífico será testigo del crecimiento más rápido durante el período de pronóstico, impulsado por la expansión de la infraestructura ortopédica, el aumento del ingreso disponible, la mayor conciencia de los procedimientos mínimamente invasivos, el crecimiento del turismo médico y un número creciente de casos de lesiones articulares entre las poblaciones de personas mayores y jóvenes que practican deportes activos.

- Medio Oriente, África y América Latina representan mercados emergentes donde el creciente acceso a la atención médica, las inversiones en infraestructura médica y la creciente demanda de procedimientos asequibles de reparación de articulaciones presentan oportunidades significativas para la expansión de la adopción de dispositivos de artroscopia.

Mercado de dispositivos de artroscopia, panorama competitivo y actores clave

El mercado global de dispositivos de artroscopia se caracteriza por una combinación de fabricantes multinacionales consolidados de dispositivos médicos y empresas especializadas en dispositivos ortopédicos. Las empresas líderes compiten frecuentemente en función de la innovación tecnológica, la amplitud de su cartera de productos (implantes, instrumental, visualización y sistemas de fluidos), la calidad y la distribución global.

Informes anteriores de The Insight Partners identificaron la segmentación por productos como artroscopios, implantes, sistemas de gestión de fluidos, sistemas de visualización, afeitadoras eléctricas, sistemas de radiofrecuencia y otros equipos artroscópicos.

Con la creciente demanda en las regiones emergentes y los crecientes volúmenes de procedimientos en todo el mundo, la competencia se está intensificando a medida que las empresas buscan diferenciarse a través de tecnología avanzada (por ejemplo, visualización de alta definición, instrumentación mínimamente invasiva, implantes biocompatibles), soluciones rentables y penetración geográfica.

Los actores clave del mercado son:

- Arthrex, Inc.

- Corporación CONMED

- Servicios Johnson y Johnson, Inc.

- KARL STORZ SE & Co. KG

- Medtronic

- Richard Wolf GmbH.

- Smith y sobrino

- Corporación Stryker

- Zimmer Biomet

Otros jugadores analizados durante el tiempo de la investigación:

- Corporación Ortopédica Unida

- Instrumentos quirúrgicos Sklar

- Cannuflow Inc.

- Parcus Medical

- Bioventus LLC

- Grupo Médico Wright NV

- Compañía de Implantes Ortopédicos (OIC)

- GPC Medical Ltd.

- Hofer GmbH

- Shenzhen Mindray Electrónica Biomédica Co., Ltd.

- B. Braun Melsungen AG

Noticias y desarrollos recientes del mercado de dispositivos de artroscopia

- Stryker presentó una plataforma de visualización de artroscopia mejorada que incluye imágenes 4K mejoradas y una mejor diferenciación de tejidos blandos para respaldar la precisión en procedimientos mínimamente invasivos.

- Arthrex amplió su cartera con nuevos anclajes de sutura bioabsorbibles diseñados para promover la integración ósea y reducir las complicaciones asociadas con los implantes metálicos.

- Smith+Nephew lanzó una plataforma de medicina deportiva integrada digitalmente que conecta instrumentos de artroscopia inteligentes con herramientas de planificación quirúrgica para mejorar la eficiencia del flujo de trabajo.

- ConMed recibió la autorización regulatoria para un sistema de resección motorizada de próxima generación equipado con tecnología de detección de torsión para mejorar el control de corte y la precisión quirúrgica.

- Karl Storz lanzó un software de optimización de imágenes habilitado con IA para torres de artroscopia, automatizando los ajustes de iluminación y contraste para mejorar la visualización en tiempo real.

Informe de mercado sobre dispositivos de artroscopia: cobertura y resultados

El informe "Mercado de procedimientos y productos para artroscopia (2021-2034)" de The Insight Partners ofrece un análisis completo y estructurado que incluye:

- Tamaño y pronóstico del mercado a nivel global, regional y nacional (USD) en todos los segmentos clave (producto, aplicación, usuario final, geografía).

- Dinámica del mercado: examen detallado de los impulsores, las restricciones, las oportunidades y las tendencias emergentes en el dominio de los dispositivos de artroscopia.

- Panorama competitivo: elaboración de perfiles de fabricantes clave, análisis de concentración del mercado, evaluación comparativa tecnológica y perspectivas estratégicas.

- Análisis profundo basado en segmentación: segmentación por tipos de productos, tipos de aplicación/artroscopia, categorías de usuarios finales y mercados regionales.

- Escenarios de pronóstico: proyecciones de demanda probables, optimistas y conservadoras durante el horizonte de pronóstico (hasta 2031), que permiten a las partes interesadas evaluar las oportunidades a corto y largo plazo.

- Análisis de apoyo: cadena de valor, entorno regulatorio, visión general de la oferta y la demanda, y facilitadores y limitaciones del crecimiento.

Mrinal es una experimentada analista de investigación con más de 8 años de experiencia en inteligencia de mercado y consultoría en ciencias de la vida. Con una mentalidad estratégica y un firme compromiso con la excelencia, ha desarrollado una amplia experiencia en pronósticos farmacéuticos, evaluación de oportunidades de mercado y desarrollo de indicadores de referencia para la industria. Su trabajo se centra en brindar información práctica que permita a los clientes tomar decisiones estratégicas informadas.

La principal fortaleza de Mrinal reside en convertir conjuntos de datos cuantitativos complejos en inteligencia de negocios significativa. Su perspicacia analítica es fundamental para definir estrategias de salida al mercado (GTM) y descubrir oportunidades de crecimiento en los sectores farmacéutico y de dispositivos médicos. Como consultora de confianza, se centra constantemente en optimizar los procesos de flujo de trabajo y establecer las mejores prácticas, impulsando así la innovación y la eficiencia operativa para sus clientes.

- Análisis exhaustivo del tamaño del mercado y previsiones

- Análisis detallado de la segmentación

- Evaluación en profundidad de la dinámica del mercado

- Información a nivel regional y nacional

- Panorama competitivo y análisis comparativo de empresas

- Inteligencia empresarial estratégica

Testimonios

El informe de mercado de sistemas SCADA de Insight Partners es completo y ofrece información valiosa sobre las tendencias actuales y las previsiones futuras. El equipo fue altamente profesional, receptivo y me brindó un gran apoyo en todo momento. Estamos muy satisfechos y recomendamos ampliamente sus servicios.

RAN KEDEM Socio, Reali Technologies LTDsSolicité un informe sobre un mercado de software muy específico y el equipo lo elaboró en pocos días. La información era muy relevante y estaba bien presentada. Posteriormente, solicité algunos cambios y adiciones al informe. El equipo fue muy receptivo y recibí el informe final en menos de una semana.

JEAN-HERVE JENN Presidente, Future AnalyticaTrabajamos con The Insight Partners para un importante estudio y pronóstico de mercado. Nos brindaron una visión clara de las oportunidades y los riesgos, lo que nos ayudó a definir nuestros planes. Su investigación fue fácil de usar y se basó en datos sólidos. Nos ayudó a tomar decisiones inteligentes y seguras. Los recomendamos ampliamente.

PIYUSH NAGPAL Vicepresidente Sénior, , High Beam GlobalThe Insight Partners realizó una investigación de mercado profunda y bien estructurada con una sólida experiencia en el sector. Su equipo fue profesional y receptivo en todo momento. El sitio web, fácil de usar, facilitó el acceso a los informes del sector. Los recomendamos ampliamente por sus servicios de investigación confiables y de alta calidad.

YUKIHIKO ADACHI Director Ejecutivo, , Deep Blue, LLCEsta es la primera vez que compro un informe de mercado de The Insight Partners. Aunque al principio tenía dudas, visité su sitio web y me sentí más cómodo al arriesgarme y comprarlo. Estoy completamente satisfecho con la calidad del informe y el servicio al cliente. Tenía varias preguntas y comentarios sobre el informe inicial, pero después de un par de conversaciones por correo electrónico con su analista, creo que tengo un informe que puedo usar como base para nuestro proceso de planificación estratégica. Muchas gracias por tomarse el tiempo y hacer de esta una experiencia positiva. Sin duda, recomendaré sus servicios y serán mi primera opción cuando necesitemos más datos de mercado.

JOHN SUZUKI Presidente y Director Ejecutivo, Director de la Junta Directiva, BK TechnologiesAgradezco su apoyo y la profesionalidad que demostraron al atender mi solicitud de información sobre el mercado de diagnóstico in vitro (IVD) para enfermedades infecciosas en Nigeria. Agradezco su paciencia, su orientación y su disposición a ofrecerme un descuento, lo que finalmente nos permitió cerrar un trato. Espero poder colaborar con The Insight Partners en el futuro, gracias a la impresión que me causó este primer encuentro.

DRA. CHIJIOKE ONYIA, DIRECTORA GENERAL, PineCrest Healthcare Ltd.Razón para comprar

- Toma de decisiones informada

- Comprensión de la dinámica del mercado

- Análisis competitivo

- Información sobre clientes

- Pronósticos del mercado

- Mitigación de riesgos

- Planificación estratégica

- Justificación de la inversión

- Identificación de mercados emergentes

- Mejora de las estrategias de marketing

- Impulso de la eficiencia operativa

- Alineación con las tendencias regulatorias