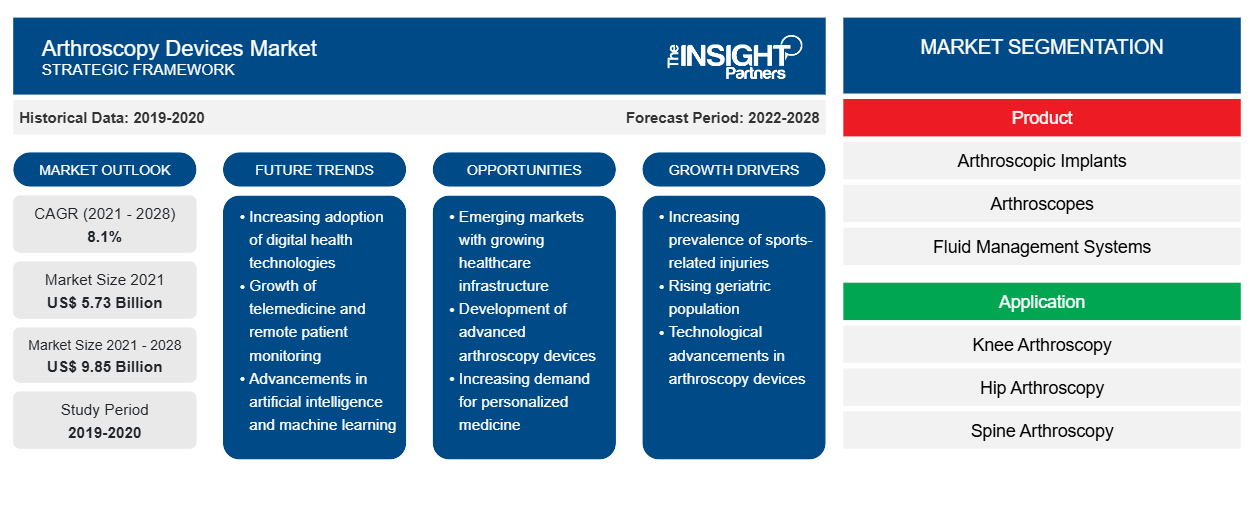

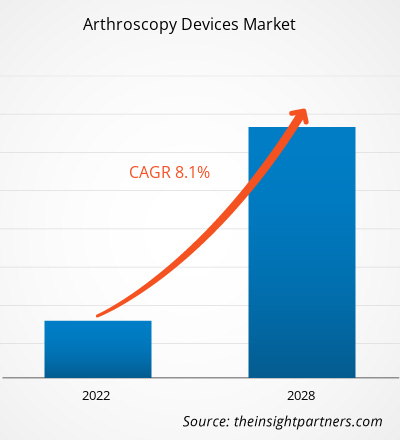

関節鏡検査装置市場は、2021年の57億2,524万米ドルから2028年には98億5,388万米ドルに達すると予測されており、 2021年から2028年にかけて8.1%のCAGRを記録すると予想されています。

関節鏡検査は、関節の問題を診断し、治療するための処置です。外科医は、ボタン穴ほどの小さな切開部から、関節鏡と呼ばれる光ファイバー ビデオ カメラが取り付けられた細いチューブを挿入します。関節鏡は、医師が膝、股関節、脊椎、肩、肘などの体の関節の内部を観察し、検査、診断、治療処置を行うことができる医療機器です。関節鏡検査機器は、関節の変形性関節症、関節リウマチ、腱炎、骨腫瘍などの病気を検査できます。

このレポートは、市場動向、技術の進歩、市場のダイナミクスなど、さまざまなパラメータに重点を置いて、関節鏡検査装置市場の洞察と詳細な分析を提供します。また、世界中の主要な市場プレーヤーの競合状況分析も提供します。さらに、すべての地域の市場に対するCOVID-19パンデミックの影響も含まれています。COVID-19パンデミックは、世界中で公衆衛生危機と経済危機の両方を引き起こしました。パンデミック以前は、定期的なスクリーニング、慰問、治療が行われていたため、世界の関節鏡検査装置市場は継続的に成長していました。COVID-19の第一波は、腫瘍学的症例の診察、フォローアップ、スクリーニングを混乱させました。世界中のヘルスケア業界で制御不能な状況が生まれ、診察件数の減少と、診断された変形性関節症および関節リウマチ症例の数の減少につながりました。いくつかの企業は2019年の第4四半期に深刻な損失を被りました。パンデミックは2020年の第1四半期と第2四半期にも悪影響を及ぼしました。したがって、COVID-19パンデミックが世界市場に与える影響は即時かつ劇的なものでした。世界中のビジネスは、サプライチェーンの混乱とヘルスケア製品およびサービスの需要の増加により妨げられました。病院や診療所でのCOVID-19感染を減らすために、医療従事者と患者は遠隔患者治療を採用し、それを好みました。これらの予測不可能な状況下では、整形外科診療も影響を受けずにはいられませんでした。多くの外科治療と緊急でない診察がキャンセルまたは延期されました。多くの施設で選択的手術が一時停止され、ウイルスの拡散を制限し、医療従事者(看護師、麻酔科医)、医療機器(個人用保護具、人工呼吸器)、ベッドのリソースを確保して再配分するために、整形外科の症例全体が大幅に減少しました。世界中で「ステイホーム」戦略が取られた結果、COVID-19の流行期間中、関節形成術や関節鏡手術が大幅に減少し、変形性関節症の発症率も低下した。

要件に合わせてレポートをカスタマイズする

このレポートの一部、国レベルの分析、Excelデータパックなど、あらゆるレポートを無料でカスタマイズできます。また、スタートアップや大学向けのお得なオファーや割引もご利用いただけます。

関節鏡検査装置市場:

- このレポートの主要な市場動向を入手してください。この無料サンプルには、市場動向から見積もりや予測に至るまでのデータ分析が含まれます。

COVID-19の発生により医療インフラが混乱し、COVID-19の治療に重点が移ったため、さまざまな疾患の診断が軽視されました。さらに、筋骨格系疾患の検出と治療もCOVID-19のパンデミックによって妨げられました。これにより、世界中の関節鏡検査装置市場の成長が大きく抑制されました。

市場分析

筋骨格系疾患の増加が市場を牽引

筋骨格系障害(MSD)は、世界中で最も一般的な健康状態です。世界保健機関(WHO)が発表したデータによると、2021年2月には、世界中で約17億1,000万人が筋骨格系の問題に苦しんでいました。腰痛は広範囲にわたる筋骨格系の疾患で、世界中で5億6,800万人が罹患しています。腰痛は160か国で障害の主な原因となっています。筋骨格系障害は、運動能力と器用さを著しく損なうため、仕事からの早期退職、幸福感の低下、社交能力の低下につながります。筋骨格系の疾患によって障害を持つ人の数は増加しており、この傾向は今後数十年続くと予想されています。

さらに、WHO によれば、人口で見ると高所得国が最も影響を受けており (4 億 4,100 万人)、WHO 西太平洋地域の国々が 4 億 2,700 万人でこれに続き、東南アジアが 3 億 6,900 万人となっている。筋骨格系疾患は、世界中で障害生存年数 ( YLD ) の主な原因でもあり、およそ 1 億 4,900 万YLD、全YLDの 17% を占めている。世界中で 4 億 3,600 万人が罹患している骨折、変形性関節症 (3 億 4,300 万人)、その他の傷害 (3 億 500 万人)、首の痛み (2 億 2,200 万人)、切断 (1 億 7,500 万人)、関節リウマチ (1,400 万人) はすべて、筋骨格系疾患の全体的な負担に寄与している。

外科的関節鏡検査は、慢性的な関節痛や機能障害のある患者にとって、確立された治療法です。関節鏡検査は、関節を開放する手術に比べて侵襲性が低く、症状の治療、入院、構造的回復、長期的な結果など、患者の全体的な転帰が改善されます。したがって、筋骨格障害、変形性関節症、関節リウマチの罹患率の増加が、予測期間中に市場を牽引すると予想されます。

製品ベースの洞察

製品に基づいて、関節鏡検査装置市場は、関節鏡、関節鏡検査インプラント、流体管理システム、無線周波数システム、可視化システム、電動シェーバーシステム、およびその他の関節鏡検査装置に分類されます。 2021年には、関節鏡セグメントが市場で最大のシェアを占め、予測期間中に9.1%という最速のCAGRを記録すると予想されています。

アプリケーションベースの洞察

用途に基づいて、関節鏡検査装置市場は、膝関節鏡検査、股関節鏡検査、脊椎関節鏡検査、足と足首の関節鏡検査、肩と肘の関節鏡検査、その他に分類されます。2021年には、股関節鏡検査セグメントが市場で最大のシェアを占め、2021年から2028年の間に8.9%という最高のCAGRを記録すると予想されています。

関節鏡検査装置市場のプレーヤーは、製品の発売や拡張などの有機的な戦略を採用して、世界中で事業展開と製品ポートフォリオを拡大し、高まる需要に応えています。

地理別

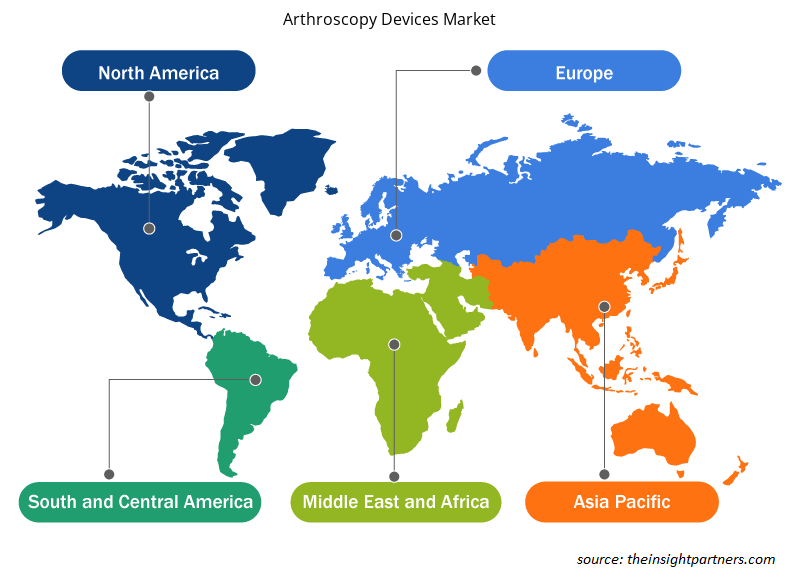

地理に基づいて、関節鏡検査装置市場は、北米(米国、カナダ、メキシコ)、欧州(英国、ドイツ、フランス、イタリア、スペイン、その他の欧州)、アジア太平洋(中国、日本、インド、オーストラリア、韓国、その他のアジア太平洋)、中東およびアフリカ(UAE 、サウジアラビア、南アフリカ、その他の中東およびアフリカ)、南米および中米(ブラジル、アルゼンチン、その他の南米および中米)に分類されます。

関節鏡検査装置市場の地域別分析

予測期間を通じて関節鏡検査装置市場に影響を与える地域的な傾向と要因は、Insight Partners のアナリストによって徹底的に説明されています。このセクションでは、北米、ヨーロッパ、アジア太平洋、中東およびアフリカ、南米および中米にわたる関節鏡検査装置市場のセグメントと地理についても説明します。

- 関節鏡検査装置市場の地域別データを入手

関節鏡検査装置市場レポートの範囲

| レポート属性 | 詳細 |

|---|---|

| 2021年の市場規模 | 57億3千万米ドル |

| 2028年までの市場規模 | 98.5億米ドル |

| 世界のCAGR(2021年~2028年) | 8.1% |

| 履歴データ | 2019-2020 |

| 予測期間 | 2022-2028 |

| 対象セグメント | 製品別

|

| 対象地域と国 | 北米

|

| 市場リーダーと主要企業プロフィール |

|

関節鏡検査機器市場のプレーヤー密度:ビジネスダイナミクスへの影響を理解する

関節鏡検査装置市場は、消費者の嗜好の変化、技術の進歩、製品の利点に対する認識の高まりなどの要因により、エンドユーザーの需要が高まり、急速に成長しています。需要が高まるにつれて、企業は提供を拡大し、消費者のニーズを満たすために革新し、新たなトレンドを活用し、市場の成長をさらに促進しています。

市場プレーヤー密度とは、特定の市場または業界内で活動している企業または会社の分布を指します。これは、特定の市場スペースに、その市場規模または総市場価値に対してどれだけの競合相手 (市場プレーヤー) が存在するかを示します。

関節鏡検査装置市場で事業を展開している主要企業は次のとおりです。

- アースレックス株式会社

- コンメッド株式会社

- ジョンソン・エンド・ジョンソン・サービス株式会社

- カールストルツ SE & Co. KG

- メドトロニック

免責事項:上記の企業は、特定の順序でランク付けされていません。

- 関節鏡検査装置市場のトップキープレーヤーの概要を入手

企業プロフィール

- アースレックス株式会社

- コンメッド株式会社

- ジョンソン・エンド・ジョンソン・サービス株式会社

- カールストルツ SE & Co. KG

- メドトロニック

- リチャード・ウルフ GmbH。

- スミス・アンド・ネフュー

- ストライカーコーポレーション

- ジマーバイオメット

- 株式会社ニューベイシブ

- 過去2年間の分析、基準年、CAGRによる予測(7年間)

- PEST分析とSWOT分析

- 市場規模価値/数量 - 世界、地域、国

- 業界と競争環境

- Excel データセット

- Airport Runway FOD Detection Systems Market

- Aesthetic Medical Devices Market

- Quantitative Structure-Activity Relationship (QSAR) Market

- Ceramic Injection Molding Market

- Adaptive Traffic Control System Market

- Embolization Devices Market

- Influenza Vaccines Market

- Aircraft Wire and Cable Market

- Rugged Phones Market

- Public Key Infrastructure Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

よくある質問

The North America region secures the major share of the global arthroscopy devices market. Rapid increase in the number of arthroscopies in the region, advancements in arthroscopy products and the highly active research ecosystem for arthroscopic applications is projected to accelerate the growth of the market. Moreover, increasing prevalence of chronic diseases and orthopedic ailments, especially among the aging population in this region of arthroscopy devices is propelling the market's expansion in this region.

Due to an increasing number of infected patients worldwide, several research institutes and leading organizations put an effort to develop efficient methods of COVID 19 treatment and ways to combat pandemic. Many companies manufacturing arthroscopy devices focused on responding emergencies by various strategies such as manufacturing PPEs to healthcare workers, distribution of pharmaceutical drugs and various other activities. For instance, in September 2020, Arthrex, a global leader in minimally invasive orthopedic technology, announced it is using its innovative production capabilities to manufacture and donate more than 6,000 protective face shields to school systems across the region.

According to World Health Organization (WHO). As the epidemic has become a global pandemic, many health authorities focused pandemic-related care and avoided human contact in reaction to growing transmission and strain on health-care resources by postponing elective surgeries, suspending outpatient clinics, and triaging employees involved in urgent care. For instance, as per the British Journal of Surgery published in May 2020 stated that orthopedic procedures would be affected most, with 6.3 million operations cancelled worldwide. Recent COVID-19 guidelines for pediatric orthopedic surgeons suggested focus on urgent care and triaging cases to postpone elective surgeries and clinic appointments, with transition to virtual-based care when appropriate.

Thus, the pandemic had a negative impact on the arthroscopy market in the region.

Johnson and Johnson Services, Inc and CONMED Corporation are the top two companies that hold huge market shares in the arthroscopy devices market.

The arthroscopy devices market majorly consists of players such as Arthrex, Inc.; CONMED Corporation; Johnson and Johnson Services, Inc.; KARL STORZ SE & Co. KG; Medtronic; Richard Wolf GmbH.; Smith & Nephew; Stryker Corporation; Zimmer Biomet; and NuVasive, Inc amongst others.

In 2021, the hip arthroscopy held the largest share of the market, by application. The similar application segment of the arthroscopy devices market is expected to witness growth in its demand at the fastest CAGR from 2021 to 2028.

Arthroscopy is a procedure for diagnosing and treating joint problems. A surgeon inserts a narrow tube attached to a fiber-optic video camera through a small incision about the size of a buttonhole which is called an arthroscope. An arthroscope is a medical device that allows doctors to see within bodily joints such as the knee, hip, spine, shoulder, and elbow to inspect, diagnose, and perform therapeutic procedures. Arthroscopy devices can examine for illnesses like osteoarthritis, rheumatoid arthritis, tendinitis, and bone tumors in the joints.

Key factors that are driving the growth of this market are the growing prevalence of musculoskeletal disorders osteoarthritis and rheumatoid arthritis, rising number of sport injuries requiring arthroscopy procedure to prevent complete joint and rising elderly population. Additionally, the increasing prevalence of obesity and rising number of product launches and approvals are likely to emerge as a significant future trend in the market during the forecast period.

The CAGR value of the arthroscopy devices market during the forecasted period of 2021–2028 is 8.1%.

In 2021, the arthroscopes segment accounted for the largest share of the market; it is further expected to continue its dominance over the forecast period. The arthroscopes are primarily used in the minimally invasive strategy. It aids patients' recovery and reduces scarring. Moreover, the decrease in the life span of arthroscopes due to the sterilization process used to prevent contamination and the launch of single-use arthroscopes. Thus, due to above factors, the arthroscopes segment is expected to dominate the arthroscopy devices market by product segment. Moreover, arthroscopes are expected to register the highest CAGR in arthroscopy devices market during 2021-2028.

Trends and growth analysis reports related to Life Sciences : READ MORE..

The List of Companies - Arthroscopy Devices Market

- Arthrex, Inc.

- CONMED Corporation

- Johnson and Johnson Services, Inc.

- KARL STORZ SE & Co. KG

- Medtronic

- Richard Wolf GmbH.

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

- NuVasive, Inc.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

このレポートの無料サンプルを入手する

このレポートの無料サンプルを入手する