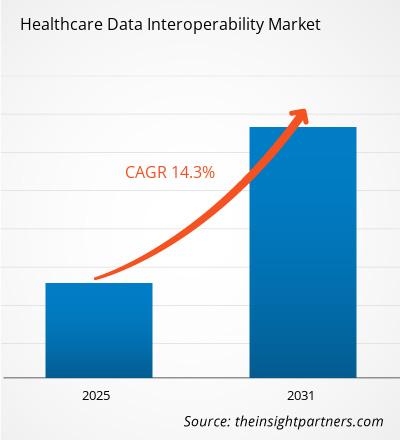

The Healthcare Data Interoperability Market is expected to register a CAGR of 14.3% from 2025 to 2031, with a market size expanding from US$ XX million in 2024 to US$ XX Million by 2031.

The report is segmented by Interoperability Level (Foundational Interoperability, Structural Interoperability, and Semantic Interoperability), Type (Solutions and Services), End User (Healthcare Providers, Healthcare Payers, and Pharmacies). The global analysis is further broken-down at regional level and major countries. The report offers the value in USD for the above analysis and segments

Purpose of the Report

The report Healthcare Data Interoperability Market by The Insight Partners aims to describe the present landscape and future growth, top driving factors, challenges, and opportunities. This will provide insights to various business stakeholders, such as:

- Technology Providers/Manufacturers: To understand the evolving market dynamics and know the potential growth opportunities, enabling them to make informed strategic decisions.

- Investors: To conduct a comprehensive trend analysis regarding the market growth rate, market financial projections, and opportunities that exist across the value chain.

- Regulatory bodies: To regulate policies and police activities in the market with the aim of minimizing abuse, preserving investor trust and confidence, and upholding the integrity and stability of the market.

Healthcare Data Interoperability Market Segmentation

Interoperability Level

- Foundational Interoperability

- Structural Interoperability

- Semantic Interoperability

Type

- Solutions and Services

End User

- Healthcare Providers

- Healthcare Payers

- Pharmacies

Geography

- North America

- Europe

- Asia Pacific

- Middle East and Africa

- South and Central America

Customize This Report To Suit Your Requirement

You will get customization on any report - free of charge - including parts of this report, or country-level analysis, Excel Data pack, as well as avail great offers and discounts for start-ups & universities

Healthcare Data Interoperability Market: Strategic Insights

- Get Top Key Market Trends of this report.This FREE sample will include data analysis, ranging from market trends to estimates and forecasts.

Healthcare Data Interoperability Market Growth Drivers

- Regulatory Mandates: Governments and regulatory bodies are increasingly focused on the need for interoperability in healthcare systems. Initiatives such as the 21st Century Cures Act in the US mandate that healthcare organizations need to adopt interoperable systems to improve patient access to health information and enhance care coordination.

- Rising Demand for Integrated Care: As healthcare shifts towards value-based care models, there is a growing need for integrated care solutions for seamless data sharing among providers. Interoperability facilitates better communication and collaboration among healthcare professionals, leading to improved patient outcomes.

Healthcare Data Interoperability Market Future Trends

- Increased Adoption of APIs: There is a future increase in the use of APIs. This will allow applications in the healthcare sector to communicate and share information more efficiently. More innovative solutions that improve interoperability between different platforms will be possible through the use of APIs.

- Focus on Data Security and Privacy: Data sharing is going to increase with greater emphasis placed on data security and patient confidentiality. Interoperability solutions will incorporate enhanced security functionalities, such as encryption and access controls, to shield sensitive health information.

Healthcare Data Interoperability Market Opportunities

- Investment in Interoperability Solutions: Healthcare organizations have been investing more in interoperability solutions to make their operations more efficient and to improve the care that patients receive. Companies with innovative and scalable interoperability solutions can exploit this the most.

- Focus on Emerging Markets: As healthcare systems in emerging markets evolve, there is an opportunity to introduce interoperability solutions tailored to their specific needs.

Healthcare Data Interoperability Market Regional Insights

The regional trends and factors influencing the Healthcare Data Interoperability Market throughout the forecast period have been thoroughly explained by the analysts at Insight Partners. This section also discusses Healthcare Data Interoperability Market segments and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America.

- Get the Regional Specific Data for Healthcare Data Interoperability Market

Healthcare Data Interoperability Market Report Scope

| Report Attribute | Details |

|---|---|

| Market size in 2024 | US$ XX million |

| Market Size by 2031 | US$ XX Million |

| Global CAGR (2025 - 2031) | 14.3% |

| Historical Data | 2021-2023 |

| Forecast period | 2025-2031 |

| Segments Covered |

By Interoperability Level

|

| Regions and Countries Covered | North America

|

| Market leaders and key company profiles |

Healthcare Data Interoperability Market Players Density: Understanding Its Impact on Business Dynamics

The Healthcare Data Interoperability Market market is growing rapidly, driven by increasing end-user demand due to factors such as evolving consumer preferences, technological advancements, and greater awareness of the product's benefits. As demand rises, businesses are expanding their offerings, innovating to meet consumer needs, and capitalizing on emerging trends, which further fuels market growth.

Market players density refers to the distribution of firms or companies operating within a particular market or industry. It indicates how many competitors (market players) are present in a given market space relative to its size or total market value.

Major Companies operating in the Healthcare Data Interoperability Market are:

- InterSystems Corporation

- Allscripts CareInMotion

- Orion Health group of companies

- Infor

- Cerner Corporation

Disclaimer: The companies listed above are not ranked in any particular order.

- Get the Healthcare Data Interoperability Market top key players overview

Key Selling Points

- Comprehensive Coverage: The report comprehensively covers the analysis of products, services, types, and end users of the Healthcare Data Interoperability Market, providing a holistic landscape.

- Expert Analysis: The report is compiled based on the in-depth understanding of industry experts and analysts.

- Up-to-date Information: The report assures business relevance due to its coverage of recent information and data trends.

- Customization Options: This report can be customized to cater to specific client requirements and suit the business strategies aptly.

The research report on the Healthcare Data Interoperability Market can, therefore, help spearhead the trail of decoding and understanding the industry scenario and growth prospects. Although there can be a few valid concerns, the overall benefits of this report tend to outweigh the disadvantages.

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

Some of the customization options available based on the request are an additional 3–5 company profiles and country-specific analysis of 3–5 countries of your choice. Customizations are to be requested/discussed before making final order confirmation#as our team would review the same and check the feasibility

Regulatory mandates and rising demand for integrated care are the major factors driving the healthcare data interoperability market.

The report can be delivered in PDF/PPT format; we can also share excel dataset based on the request

Increased adoption of APIs and focus on data security and privacy are likely to remain a key trend in the market.

The Healthcare Data Interoperability Market is estimated to witness a CAGR of 14.3% from 2024 to 2031

Trends and growth analysis reports related to Technology, Media and Telecommunications : READ MORE..

The List of Companies

1. Allscripts Healthcare Solutions, Inc.

2. Cerner Corporation

3. Intersystems Corporation

4. Orion Health Group Limited

5. Koninklijke Philips N.V.

6. Visolve Inc.

7. Infor, Inc.

8. Nextgen Healthcare, Inc.

9. EPIC Systems Corporation

10. iNTERFACEWARE

Get Free Sample For

Get Free Sample For