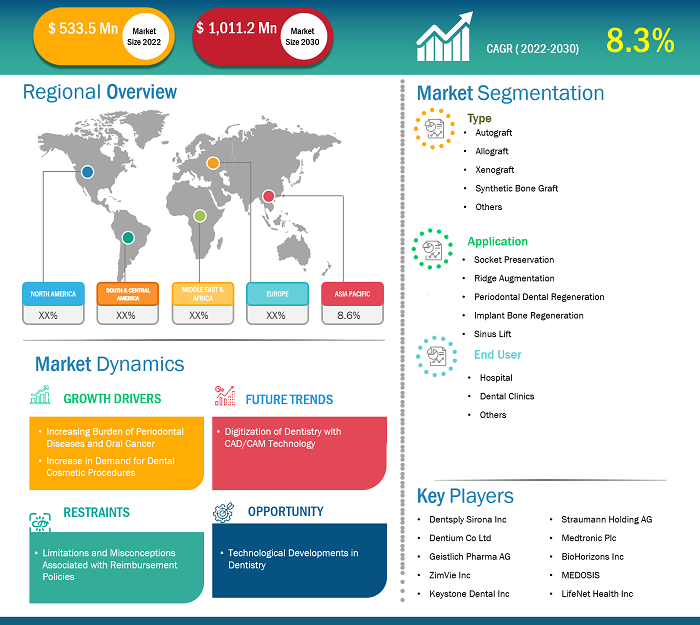

[Research Report] The dental bone graft substitute market size was US$ 533.5 million in 2022 and is projected to reach US$ 1,011.2 million by 2030. It is expected to register a CAGR of 8.3% in 2022-2030.

Market Insights and Analyst View:

The dental bone graft substitute market size is growing rapidly due to the increasing number of dental diseases and growing instances of dental procedures due to cosmetic appearance. The increasing prevalence of dental diseases and the introduction of supportive government initiatives regarding dental bone graft substitutes are among the most enduring growth drivers of the dental bone graft substitute market. These bone graft substitutes are also used in cosmetic dental procedures, owing to which there is notable demand for cosmetic procedures, especially in high-income countries.

Growth Drivers and Challenges:

The increasing burden of periodontal diseases and oral cancer, and the growing demand for dental cosmetic procedures drives the dental bone graft substitute market growth. Oral diseases are highly preventable. However, these diseases are major health issues in many countries and affect people throughout their lifetime. Several common dental issues include periodontal diseases, dental caries (tooth decay), and tooth loss. The increasing prevalence of dental diseases is causing the need for teeth replacement, dental crowns, copings, and dental bridges. As per the World Health Organization (WHO) Global Oral Health Status Report (2022), about 3 out of 4 people are affected due to oral diseases globally, of which ~3.5 billion people live in middle-income countries. Additionally, ~2 billion people globally suffer from dental caries in permanent teeth, and about 514 million children suffer from primary teeth caries. The growing prevalence rate of dental problems such as crooked teeth, overbites, spaces between teeth, and teeth overcrowding is creating the demand for dental bone graft substitute to treat such problems. For instance, as per the Centers for Disease Control and Prevention (CDC), in the US, about 47.2% of the adults above 30 years of age have some periodontal disease, which increases with age; and about 70.1% of adults over the age of 65 years suffered from periodontal disease in 2020. This surging number of people suffering from dental diseases is fueling the demand for dental bone graft substitute for easy and rapid treatment. Therefore, the increase in prevalence of oral diseases worldwide is fueling the growth of the market.

Digitization of dentistry with CAD/CAM technology is expected to bring new dental bone graft substitute market trends in the coming years.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Dental Bone Graft Substitute Market: Strategic Insights

Market Size Value in US$ 533.5 million in 2022 Market Size Value by US$ 1,011.2 million by 2030 Growth rate CAGR of 8.3% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Dental Bone Graft Substitute Market: Strategic Insights

| Market Size Value in | US$ 533.5 million in 2022 |

| Market Size Value by | US$ 1,011.2 million by 2030 |

| Growth rate | CAGR of 8.3% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Report Segmentation and Scope:

The dental bone graft substitute market analysis has been carried out by considering the following segment type, application, end user, and geography. The market, by type, is segmented into autograft, allograft, xenograft, synthetic bone graft, and others. Based on application, the market is segmented into socket preservation, ridge augmentation, periodontal dental regeneration, implant bone regeneration, and sinus lift. The market, by end user, is segmented into hospital, dental clinics, and others. Geographically, the scope of the dental bone graft substitute market report is primarily divided into North America (the US, Canada, and Mexico), Europe (Spain, the UK, Germany, France, Italy, and the Rest of Europe), Asia Pacific (South Korea, China, Japan, India, Australia, and the Rest of Asia Pacific), Middle East & Africa (South Africa, Saudi Arabia, the UAE, and the Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America).

Segmental Analysis:

The dental bone graft substitute market, based on type, is segmented into autograft, allograft, xenograft, synthetic bone graft, and others. In 2022, the autograft segment held the largest dental bone graft substitute market share. The xenograft segment is expected to record the highest CAGR of the dental bone graft substitute market during 2022–2030. Autografts are commonly obtained from extraoral and intraoral sites, such as the mandibular ramus, mandibular symphysis, external oblique ridge, proximal ulna, iliac crest, or distal radius, of the individual undergoing treatment, as they are good sources of cortical and cancellous bone. Autografts are associated with higher surgical costs and involve significant surgical risks, e.g., inflammation, excessive bleeding, pain and infection, limiting their application to smaller bone defects. Although other bone substitutes are routinely used to treat localized alveolar bone defects and maxillary bone grafts in dental applications, block-form autografts are still routinely used in alveolar ridge augmentation procedures. Autografts are the preferred material for complex augmentation procedures, such as posterior mandibular edentulous reconstruction, because only a few bone substitute materials can produce a volume of newly formed bone comparable to autograft materials. Xenografts are transplant materials derived from a genetically unrelated species of the host. Natural bone substitutes promote enhanced osteogenic, osteoconductive, and osteoinductive potentials by creating a favorable microenvironment for bone growth. Most xenografts derived from cattle are sterilized and processed for safe implantation into human tissue. These xenografts can be freeze-dried or demineralized and deproteinized. Xenografts are usually distributed only as a calcified matrix. Madrepore and Millepore corals are harvested and processed to become coral-derived granules (CDG) and other coral xenografts. Despite the promising prospects for many xenograft materials, a few limitations are still associated with the use of xenograft bone substitutes. These include the variable rates of resorption, lack of viable cells and biological components, and need for tissue treatment processes that allow retention of osteoinductive cells.

The dental bone graft substitute market, by application, is segmented into socket preservation, ridge augmentation, periodontal dental regeneration, implant bone regeneration, and sinus lift. In 2022, the socket preservation segment held the largest market share and is anticipated to record the highest CAGR during 2022–2030.

The market, by end user, is segmented into hospital, dental clinics, and others. In 2022, the dental clinics segment held the largest dental bone graft substitute market share and is expected to record the highest CAGR during 2022–2030.

Regional Analysis:

Geographically, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. North America is the biggest contributor to the global dental bone graft substitute market growth. Asia Pacific is predicted to show the highest CAGR in the market during 2022–2030. Significant changes have occurred in dental practice over the past 20 years in the US. As per the CDC report, 1 in 4 (26%) adults in the US have untreated tooth decay. Additionally, nearly half (~46%) of all adults aged 30 years or older show signs of gum disease, severe gum disease affecting about 9% of adults. Furthermore, technological advancements in dentistry provide numerous advantages for facilitating the work of dentists and users of dental services that are becoming more demanding in terms of aesthetics.

Dental Bone Graft Substitute Market Report Scope

Industry Developments and Future Opportunities:

The dental bone graft substitute market forecast is estimated on the basis of various secondary and primary research findings such as key company publications, association data, and databases. Strategies by key players operating in the market are listed below:

- In April 2023, ZimVie Inc. announced the launch of two products, RegenerOss CC Allograft Particulate and RegenerOss Bone Graft Plug. The launch of these products has extended ZimVie, Inc.'s biomaterials portfolio intended for filling extraction sockets and periodontal defects. The products are commercially available in North America.

Competitive Landscape and Key Companies:

Dentsply Sirona Inc, Dentium Co Ltd, Geistlich Pharma AG, ZimVie Inc, Keystone Dental Inc, Straumann Holding AG, Medtronic Plc, BioHorizons Inc, MEDOSIS, and LifeNet Health Inc are among the prominent players profiled in the dental bone graft substitute market report. In addition, several other players have been studied and analyzed during the study to get a holistic view of the market and its ecosystem. These companies focus on geographic expansions and new product launches to meet the growing demand from consumers worldwide and increase their product range in specialty portfolios. Their global presence allows them to serve a large customer base, subsequently facilitating market expansion.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Type, Causes, Disorder Type, Age Group, End User, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

The dental bone graft substitute market, based on type, is segmented into autograft, allograft, xenograft, synthetic bone graft, and others. In 2022, the autograft segment held the largest dental bone graft substitute market share. The xenograft segment is expected to record the highest CAGR of the dental bone graft substitute market during 2022–2030. The dental bone graft substitute market, by application, is segmented into socket preservation, ridge augmentation, periodontal dental regeneration, implant bone regeneration, and sinus lift. In 2022, the socket preservation segment held the largest dental bone graft substitute market share and is anticipated to record the highest CAGR during 2022–2030. The dental bone graft substitute market, by end user, is segmented into hospital, dental clinics, and others. In 2022, the dental clinics segment held the largest dental bone graft substitute market share and is expected to record the highest CAGR during 2022–2030.

The dental bone graft substitute market majorly consists of the players such Dentsply Sirona Inc, Dentium Co Ltd, Geistlich Pharma AG, ZimVie Inc, Keystone Dental Inc, Straumann Holding AG, Medtronic Plc, BioHorizons Inc, MEDOSIS, and LifeNet Health Inc

A dental bone graft is necessary when bone loss has occurred in the jaw. This procedure is commonly performed prior to dental implant placement or when bone loss is negatively affecting neighboring teeth. A dental bone graft adds volume and density to jaw in areas where bone loss has occurred. The bone graft material may be taken from own body (autogenous), or it may be purchased from a human tissue bank (allograft) or an animal tissue bank (xenograft). In some instances, the bone graft material may be synthetic (alloplast). The dental bone graft substitute market size is growing rapidly due to increasing number of dental diseases and growing instances of dental procedures due to cosmetic appearance. The increasing prevalence of dental diseases and the introduction of supportive government initiatives regarding the dental bone graft substitutes are among the most enduring growth drivers of the dental bone graft substitute market.

Based on geography, the dental bone graft substitute market is segmented into North America (the US, Canada, and Mexico), Europe (the UK, Germany, France, Italy, Spain, and the Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, and the Rest of Asia Pacific), the Middle East & Africa (the UAE, Saudi Arabia, South Africa, and Rest of the Middle East & Africa), and South & Central America (Brazil, Argentina, and the Rest of South & Central America). North America is the largest contributor to the growth of the global dental bone graft substitute market. Asia Pacific is expected to register the highest CAGR in the dental bone graft substitute market during 2022–2030.

The increasing burden of periodontal diseases and oral cancer, and the growing demand for dental cosmetic procedures bolster the dental bone graft substitute market size. However, the limitations and misconceptions associated with reimbursement policies hinder the dental bone graft substitute market growth.

1. Introduction

1.1 Scope of the Study

1.2 Market Definition, Assumptions and Limitations

1.3 Market Segmentation

2. Executive Summary

2.1 Key Insights

2.2 Market Attractiveness Analysis

3. Research Methodology

4. Dental Bone Graft Substitute Market Landscape

4.1 Overview

4.2 PEST Analysis

4.3 Ecosystem Analysis

4.3.1 List of Vendors in the Value Chain

5. Dental Bone Graft Substitute Market - Key Market Dynamics

5.1 Key Market Drivers

5.2 Key Market Restraints

5.3 Key Market Opportunities

5.4 Future Trends

5.5 Impact Analysis of Drivers and Restraints

6. Dental Bone Graft Substitute Market - Global Market Analysis

6.1 Dental Bone Graft Substitute - Global Market Overview

6.2 Dental Bone Graft Substitute - Global Market and Forecast to 2030

7. Dental Bone Graft Substitute Market – Revenue Analysis (USD Million) – By Type, 2020-2030

7.1 Overview

7.2 Synthetic Bone Graft

7.3 Xenograft

7.4 Allograft

7.5 Autograft

7.6 Others

8. Dental Bone Graft Substitute Market – Revenue Analysis (USD Million) – By Application, 2020-2030

8.1 Overview

8.2 Socket Preservation

8.3 Ridge Augmentation

8.4 Periodontal Defect Regeneration

8.5 Implant Bone Regeneration

8.6 Others

9. Dental Bone Graft Substitute Market – Revenue Analysis (USD Million) – By End-User, 2020-2030

9.1 Overview

9.2 Hospitals

9.3 Dental Clinics

9.4 Others

10. Dental Bone Graft Substitute Market - Revenue Analysis (USD Million), 2020-2030 – Geographical Analysis

10.1 North America

10.1.1 North America Dental Bone Graft Substitute Market Overview

10.1.2 North America Dental Bone Graft Substitute Market Revenue and Forecasts to 2030

10.1.3 North America Dental Bone Graft Substitute Market Revenue and Forecasts and Analysis - By Type

10.1.4 North America Dental Bone Graft Substitute Market Revenue and Forecasts and Analysis - By Application

10.1.5 North America Dental Bone Graft Substitute Market Revenue and Forecasts and Analysis - By End-User

10.1.6 North America Dental Bone Graft Substitute Market Revenue and Forecasts and Analysis - By Countries

10.1.6.1 United States Dental Bone Graft Substitute Market

10.1.6.1.1 United States Dental Bone Graft Substitute Market, by Type

10.1.6.1.2 United States Dental Bone Graft Substitute Market, by Application

10.1.6.1.3 United States Dental Bone Graft Substitute Market, by End-User

10.1.6.2 Canada Dental Bone Graft Substitute Market

10.1.6.2.1 Canada Dental Bone Graft Substitute Market, by Type

10.1.6.2.2 Canada Dental Bone Graft Substitute Market, by Application

10.1.6.2.3 Canada Dental Bone Graft Substitute Market, by End-User

10.1.6.3 Mexico Dental Bone Graft Substitute Market

10.1.6.3.1 Mexico Dental Bone Graft Substitute Market, by Type

10.1.6.3.2 Mexico Dental Bone Graft Substitute Market, by Application

10.1.6.3.3 Mexico Dental Bone Graft Substitute Market, by End-User

Note - Similar analysis would be provided for below mentioned regions/countries

10.2 Europe

10.2.1 Germany

10.2.2 France

10.2.3 Italy

10.2.4 Spain

10.2.5 United Kingdom

10.2.6 Rest of Europe

10.3 Asia-Pacific

10.3.1 Australia

10.3.2 China

10.3.3 India

10.3.4 Japan

10.3.5 South Korea

10.3.6 Rest of Asia-Pacific

10.4 Middle East and Africa

10.4.1 South Africa

10.4.2 Saudi Arabia

10.4.3 U.A.E

10.4.4 Rest of Middle East and Africa

10.5 South and Central America

10.5.1 Brazil

10.5.2 Argentina

10.5.3 Rest of South and Central America

11. Industry Landscape

11.1 Mergers and Acquisitions

11.2 Agreements, Collaborations, Joint Ventures

11.3 New Product Launches

11.4 Expansions and Other Strategic Developments

12. Competitive Landscape

12.1 Heat Map Analysis by Key Players

12.2 Company Positioning and Concentration

13. Dental Bone Graft Substitute Market - Key Company Profiles

13.1 Dentsply Sirona

13.1.1 Key Facts

13.1.2 Business Description

13.1.3 Products and Services

13.1.4 Financial Overview

13.1.5 SWOT Analysis

13.1.6 Key Developments

Note - Similar information would be provided for below list of companies

13.2 Medtronic PLC

13.3 Geistlich Pharma AG

13.4 Straumann Holding AG

13.5 ZimVie Inc

13.6 MEDOSIS

13.7 BioHorizons Inc.

13.8 Dentium Co Ltd

13.9 Keystone Dental Inc

13.10 LifeNet Health Inc

14. Appendix

14.1 Glossary

14.2 About The Insight Partners

14.3 Market Intelligence Cloud

The List of Companies - Dental Bone Graft Substitute Market

- Dentsply Sirona Inc

- Dentium Co Ltd

- Geistlich Pharma AG

- ZimVie Inc

- Keystone Dental Inc

- Straumann Holding AG

- Medtronic Plc

- BioHorizons Inc

- MEDOSIS

- LifeNet Health Inc

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For