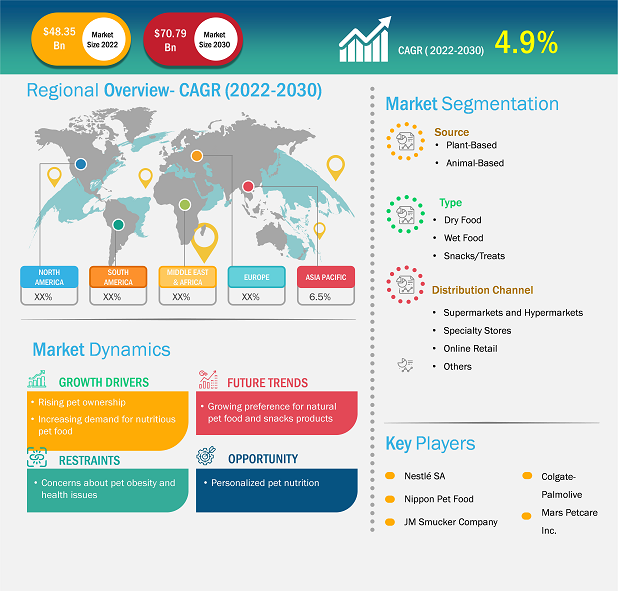

[Research Report] The dog food and snacks market size was valued at US$ 48.35 billion in 2022 and is expected to reach US$ 70.79 billion by 2031; it is estimated to register a CAGR of 4.9% from 2022 to 2031

Market Insights and Analyst View:

Dog food refers to nutritionally balanced meals specifically formulated for dogs to meet their dietary requirements. These meals come in various forms, including dry kibble, wet canned food, and raw or homemade options. They are designed to provide essential nutrients such as protein, carbohydrates, fats, vitamins, and minerals, promoting overall health in dogs. Dog snacks, on the other hand, are treats or supplementary food items given to dogs between their regular meals. Snacks can serve various purposes, including training rewards, dental care, or simply as a tasty indulgence. They come in diverse textures and flavors to cater to different preferences and dietary needs.

The demand for dog food and snacks has experienced a surge in recent years due to several factors. First, the growing awareness of pet health and nutrition among owners has led to an increased preference for high-quality, specialized dog food that addresses specific dietary requirements and health concerns. Additionally, the humanization of pets has influenced owners to seek premium and organic options, mirroring their own food choices. The pet industry has witnessed a trend towards more convenient and on-the-go snack options, aligning with the busy lifestyles of pet owners. Furthermore, the rise of e-commerce has made it easier for consumers to access a wide range of dog food and snacks, contributing to the industry's growth. Overall, the increasing focus on pet well-being, coupled with a desire for convenient and premium pet products, has fueled the demand for dog food and snacks in the market.

Dog food and snacks play a crucial role in ensuring the health and well-being of our canine companions. Dog food encompasses a variety of nutritionally balanced meals, available in formats like dry kibble, wet canned options, and even raw or homemade varieties. These formulations aim to provide dogs with essential nutrients such as protein, carbohydrates, fats, vitamins, and minerals, contributing to their overall health. On the other hand, dog snacks serve as supplementary food items or treats offered between regular meals. These snacks serve diverse purposes, from acting as training rewards to supporting dental care, and they come in various textures and flavors to accommodate different preferences and dietary needs.

The surge in demand for dog food and snacks can be attributed to several interconnected factors. Firstly, a heightened awareness of pet health and nutrition among owners has driven a preference for high-quality and specialized dog food, addressing specific dietary requirements and health concerns. The evolving perception of pets as family members has led to an increased emphasis on providing them with nutritious and well-balanced meals. Moreover, the trend of humanization of pets has significantly influenced the pet food market. Pet owners seek premium and organic options, reflecting their own food choices and values. This inclination toward healthier and more natural alternatives has contributed to the demand for specialized dog food and snacks. Additionally, the pet industry's adaptation to the fast-paced lifestyles of pet owners has led to a surge in on-the-go snack options. The convenience of these snacks aligns with the busy schedules of pet owners, providing easy and accessible solutions for treating their pets. The growth of e-commerce has further facilitated this trend, making a wide range of dog food and snacks readily available to consumers. In summary, the increasing focus on pet well-being, coupled with the humanization of pets, convenience-driven demands, and the availability of premium options, collectively contribute to the burgeoning demand for dog food and snacks in the market. This dynamic interplay of factors continues to shape the pet food industry in North America and beyond.

Growth Drivers and Challenges:

The increasing humanization of pets has become a key driver in surging the demand for the dog food and snacks market. As pets take on more prominent roles within families, owners are inclined to treat them with the same level of care and consideration as other family members. This shift in mindset has translated into a growing demand for pet products that reflect human food trends, resulting in an elevated interest in high-quality and specialized dog food and snacks. Owners now seek pet food options that go beyond basic nutrition, mirroring their own dietary preferences. This trend has fueled the demand for premium dog food and snacks that cater to specific health needs and lifestyle choices. Pet owners are increasingly drawn to products that are organic, natural, and free from artificial additives, aligning with their concerns for the well-being of their furry companions. The humanization of pets has also influenced the types of ingredients and formulations that are preferred in dog food and snacks. Pet owners are more conscious of the nutritional content of pet food, opting for options that boast balanced and wholesome ingredients. This has led to a surge in the development and marketing of specialized diets, catering to various health considerations such as weight management, digestive health, and allergies. Furthermore, the desire to pamper pets with indulgent treats has contributed to the growth of the snacks market. Pet owners are increasingly looking for tasty and innovative snack options for their dogs, viewing these treats not only as rewards for good behavior but also as a way to enhance the overall quality of their pets' lives. The humanization trend, therefore, acts as a catalyst, driving pet owners to seek premium, health-conscious, and enjoyable food options for their beloved companions. In turn, this trend continues to shape and expand the dog food and snacks market.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Dog Food and Snacks Market: Strategic Insights

Market Size Value in US$ 48.35 billion in 2022 Market Size Value by US$ 70.79 billion by 2030 Growth rate CAGR of 4.9% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Shejal

Have a question?

Shejal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Dog Food and Snacks Market: Strategic Insights

| Market Size Value in | US$ 48.35 billion in 2022 |

| Market Size Value by | US$ 70.79 billion by 2030 |

| Growth rate | CAGR of 4.9% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Shejal

Have a question?

Shejal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Report Segmentation and Scope:

The global dog food and snacks market is segmented based on source, type, distribution channel, and geography. The market is categorized into plant-based and animal-based by source. The market is categorized into dry food, wet food, and snacks/treats based on type. The market is categorized into supermarkets and hypermarkets, specialty stores, online retail, and others by distribution channel. The global dog food and snacks market is broadly segmented by geography into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America.

Segmental Analysis:

The market is categorized into dry food, wet food, and snacks/treats based on type. Dry dog food, commonly known as kibble, is a popular pet food option with a surge in demand attributed to several factors. Its convenience and longer shelf life make it a preferred choice for pet owners. Dry dog food is easy to store, handle, and portion, offering a hassle-free feeding experience. Additionally, it addresses pet health concerns, providing balanced nutrition crucial for dogs' well-being. The demand for dry dog food has surged due to increased awareness of pet nutrition, convenience in storage and serving, and a growing emphasis on pet owners seeking high-quality, specialized, and easily accessible options that contribute to their dogs' overall health. The convenience and nutritional benefits associated with dry dog food make it a staple for pet owners seeking practical and nutritious solutions for their furry companions.

Regional Analysis:

The dog food and snacks market is segmented into five key regions: North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa. North America dominated the global dog food and snacks market. The demand for dog food and snacks in North America is experiencing a surge owing to several interconnected factors. One prominent driver is the changing perception of pets as integral family members. As pets are increasingly considered companions, owners are willing to invest in their well-being, including their dietary needs. The growing awareness of pet health has led to a heightened demand for high-quality, nutritionally balanced dog food and snacks. Furthermore, the humanization of pets has influenced consumer preferences, with owners seeking premium and organic options mirroring their own food choices. In North America, the prevalence of busy lifestyles has also contributed to the rise in demand for convenient and on-the-go pet snacks. The ease of access to a wide variety of pet products through online platforms and retail channels further fuels this trend. Overall, the combination of pet humanization, health consciousness, and convenience-driven demands has led to a notable increase in the consumption of dog food and snacks in the North American market.

COVID-19 Pandemic Impact:

The COVID-19 pandemic initially hindered the global dog food and snacks market due to the shutdown of manufacturing units, shortage of labor, disruption of supply chains, and financial instability. The disruption of various industries due to the economic slowdown caused by the COVID-19 outbreak restrained the dog food and snacks supply. Various stores were closed. However, businesses started gaining ground as previously imposed limitations were eased across various countries. Moreover, the introduction of COVID-19 vaccines by governments of different countries eased the situation, leading to a rise in business activities worldwide. Several markets, including the dog food and snacks market, reported growth after the ease of lockdowns and movement restrictions.

Competitive Landscape and Key Companies:

Mars Petcare Inc., Colgate-Palmolive Co, Deuerer, Nestlé SA, Diamond Pet Foods, Heristo AG, Nippon Pet Food, JM Smucker Company, United Pet Group, and Champion Petfoods are among the prominent players operating in the global dog food and snacks market.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Source, Type, Distribution Channel

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

The List of Companies

- Mars Petcare Inc.

- Colgate-Palmolive Co

- Deuerer, Nestlé SA

- Diamond Pet Foods

- Heristo AG

- Nippon Pet Food

- JM Smucker Company

- United Pet Group

- Champion Petfoods

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For