[Research Report] The cloud computing healthcare market size is projected to grow from

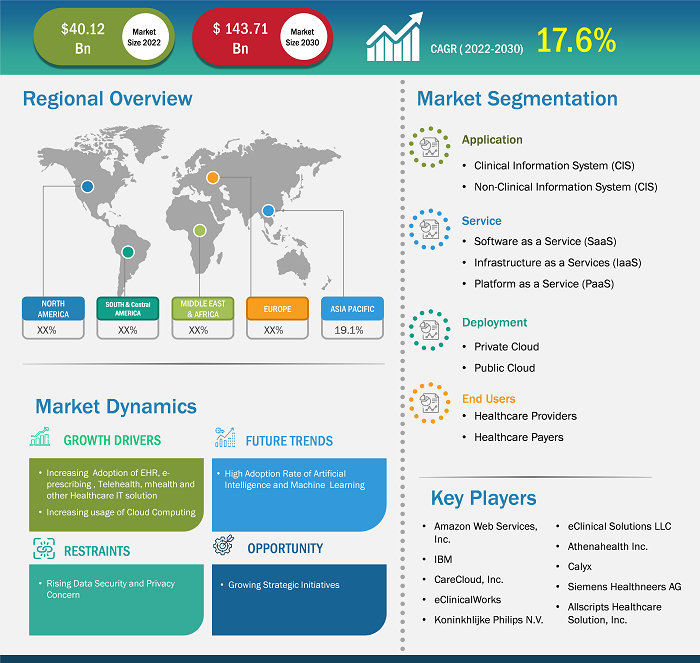

US$ 40.12 billion in 2022 to US$ 143.71 billion by 2031; the market is estimated to record a CAGR of 17.6% during 2022–2031.

Market Insights and Analyst View:

Healthcare cloud computing uses cloud-based services and technologies to store, manage, and analyze healthcare data. This includes electronic health records, medical imaging, genomic data, and other patient information, as well as advanced analytics and predictive modeling to improve patient care and outcomes. Cloud computing in healthcare also supports remote access and collaboration, enabling healthcare organizations to securely share and access patient data from anywhere, supporting telemedicine, remote monitoring, and virtual care delivery. The healthcare cloud computing market is expected to grow due to increasing numbers of startups in the sector. MedRabbits, lvlAlpha, Spire Automation, lifetrons, and Hidoc Dr are some startups.

Electronic health records, a healthcare cloud computing solution, are becoming increasingly popular with the growing digitization of the healthcare industry. As per The New England Journal of Medicine, as soon as the Health Information Technology for Economic and Clinical Health (HITECH) Act became law in 2009, the federal government dedicated US$ 300 million to help healthcare facilities adopt a nationwide health information exchange system. The Centers for Medicare and Medicaid Services (CMS) also offered more than US$ 35,000 million in incentive payments for adopting electronic health records. According to the Office of the National Coordinator for Health Information Technology (ONC), as of 2021, about 4 in 5 office-based physicians (78%) and almost all non-federal acute care hospitals (96%) adopted certified Electronic Health Records. This marked considerable 10-year progress when 28% of hospitals and 34% of physicians had adopted Electronic Health Records since 2011. As per Definitive Healthcare data from 2021, more than 89% of all hospitals had employed inpatient or ambulatory Electronic Health Records. The rapid increase in advanced healthcare analytics has also emerged as a significant growth factor for the market.

Growth Drivers:

Increasing Adoption of EHR, E-prescribing, Telehealth, and Other Healthcare IT solutions

One of the key drivers for the healthcare cloud computing market is the increasing volume and complexity of healthcare data. With the growing adoption of electronic health records, medical imaging, and genomic data, healthcare organizations face the challenge of managing and analyzing large amounts of data. Cloud computing offers a scalable, cost-effective solution for storing, processing, and accessing this data. It is an attractive option for healthcare providers looking to improve their data management capabilities. The shift towards value-based care and population health management also drives the demand for advanced analytics and predictive modeling in healthcare. Cloud computing enables healthcare organizations to leverage these technologies to identify trends, patterns, and risk factors in patient data, ultimately leading to more proactive and personalized care. This aligns with the industry's focus on improving patient outcomes and reducing costs, making cloud-based analytics a valuable driver for the healthcare cloud computing market.

Moreover, the increasing need for remote access and collaboration in healthcare is fueling the demand for cloud computing solutions. With the rise of telemedicine, remote monitoring, and virtual care delivery, healthcare organizations require secure and reliable platforms for sharing and accessing patient data from anywhere. Cloud computing provides the flexibility and accessibility needed to support these remote care models, making it an essential driver for the healthcare cloud computing market. Overall, the growing volume of healthcare data, the demand for advanced analytics, and the need for remote access and collaboration are key drivers for the healthcare cloud computing market. As healthcare organizations continue to prioritize data-driven decision-making, personalized care, and remote care delivery, cloud computing will play a crucial role in enabling these advancements in the industry.

Another driver for the healthcare cloud computing market is the increasing adoption of mobile and wearable devices in healthcare. As more patients use smartphones, tablets, and wearable devices to track their health and communicate with healthcare providers, there is a growing need for secure and efficient cloud-based storage and analysis of the data generated by these devices. Healthcare organizations are also increasingly using mobile and wearable technology to remotely monitor patients and deliver personalized care, creating a demand for cloud computing solutions that can support these initiatives. Additionally, using mobile and wearable devices can generate large amounts of data that can be effectively managed and analyzed through cloud computing, leading to insights that can improve patient care and outcomes. Overall, the increasing use of mobile and wearable devices in healthcare drives the demand for healthcare cloud computing solutions.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Healthcare Cloud Computing Market: Strategic Insights

Market Size Value in US$ 40.12 billion in 2022 Market Size Value by US$ 143.71 billion by 2030 Growth rate CAGR of 17.6% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Healthcare Cloud Computing Market: Strategic Insights

| Market Size Value in | US$ 40.12 billion in 2022 |

| Market Size Value by | US$ 143.71 billion by 2030 |

| Growth rate | CAGR of 17.6% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Report Segmentation and Scope:

The “Healthcare Cloud Computing Market” is segmented based on Application, Services, Deployment, End Users and Geography. The market is segmented based on application into clinical information systems (CIS) and Non-clinical Information Systems (NCIS). Clinical information systems (CIS) are further classified into Electronic Health Record (EHR), Picture Archiving and Communication Systems (PACS), Radiology Information Systems (RIS), Computerized Physician Order Entry (CPOE), and other applications. The Non-clinical Information Systems (NCIS) are segmented into Revenue Cycle Management (RCM), Automatic Patient Billing (APB), Payroll Management System, and other Non-clinical Information Systems. Based on Service, the market is classified into Software as a Service, Infrastructure as a Service, and Platform as a Service. Based on Deployment, the healthcare cloud computing market is bifurcated into Private Cloud and Public Cloud. Based on End Users, the market is bifurcated into Healthcare Providers and Healthcare Payers.

Segmental Analysis:

Based on application, the cloud computing healthcare market is divided into clinical and non-clinical information systems. The clinical information system (CIS)-based solutions segment held a larger market share in 2022, and the same segment is expected to register a higher CAGR during 2022–2031. In contrast, the non-clinical information system will grow at the highest CAGR during the forecasted year. The growth is attributed to the technological developments in the healthcare industry and the increasing adoption of cloud-based solutions in clinical practice. The cloud-based model offers several benefits, such as flexibility, scalability, and collaboration. Such benefits associated with the cloud-based model are expected to propel the market. In addition, the cloud-based model also eliminates the requirement of buying, maintaining, and deploying on-premises services, thereby minimizing installation and maintenance costs and contributing to the overall expansion.

Based on end users, the healthcare cloud computing market is segmented into healthcare providers and healthcare payers. The healthcare provider segment held a larger market share in 2022. It is expected to register a higher CAGR during 2022–2031. Global expansion of the information technology sector is expected to boost market revenue. The market demand is also anticipated to be further fuelled by a growing trend of outsourcing healthcare IT solutions, which lowers the overall cost of healthcare services. Therefore, increasing adoption of healthcare IT solutions after COVID-19, followed by increasing technological advancement in the healthcare IT sector, will positively impact market growth in the upcoming year.

Furthermore, partnerships with multinational companies or local market players drive the healthcare provider market growth. For instance, in February 2022, IBM acquired Neudesic, LLC, a move aimed at expanding IBM's portfolio of hybrid multi-cloud services and further advancing the company's hybrid cloud and AI strategy. Moreover, the company witnessed rapid growth during the COVID-19 pandemic due to increasing demand for technologically advanced healthcare assistance.

Regional Analysis:

Based on geography, the global cloud computing healthcare market is segmented into five key regions: North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. In 2022, North America contributed the largest global cloud computing healthcare market share. Asia Pacific is expected to register the highest CAGR during 2022-2031.

North America holds the largest share of the cloud computing healthcare market. The market in this region is split into the US, Canada, and Mexico. The market growth in the region is ascribed to factors such as the presence of key players and the increasing adoption of technology in research and development. Favorable regulatory policies and increasing investment by pharmaceutical and medical companies also favor regional growth. In March 2022, The largest academic medical system in New York, Mount Sinai Health System, announced Accenture and Microsoft would assist it with a five-year cloud migration process to ensure a fast and smooth transition. Shifting towards the cloud will allow the healthcare system to reinvest cost savings and focus on its mission.

The US is the largest contributor to the cloud computing healthcare market in North America and the world. In March 2022, Microsoft announced it completed the acquisition of Nuance Communication, a speech recognition company and leading provider of conversational artificial intelligence to enhance healthcare artificial intelligence. The increasing usage of electronic health records and e-prescriptions, followed by the penetration of telehealth, will likely drive the market’s growth.

Research and development budgets of pharmaceutical companies have also increased in the last few years in the region. For instance, In September 2022, LifePoint Health, a diversified healthcare delivery network dedicated to making communities healthier, and Google Cloud entered a multi-year strategic partnership to transform healthcare delivery in communities across the United States through LifePoint's implementation of Google Cloud's Healthcare Data Engine (HDE). Thus, the market is projected to grow during the forecast period due to rapid technological advancement and investments in the healthcare cloud computing market.

Competitive Landscape and Key Companies:

Amazon Web Services, Inc., IBM, CareCloud, Inc., eClinicalWorks, Koninklijke Philips N.V., eClinical Solutions LLC, Athenahealth Inc., Siemens Healthneers AG, and Allscripts Healthcare Solution, Inc. are the prominent cloud computing healthcare market companies. These companies focus on new technologies, existing product advancements, and geographic expansions to meet the growing consumer demand worldwide.

Industry Developments and Future Opportunities:

Various initiatives taken by leading players operating in the cloud computing healthcare market are listed below:

- In November 2023, Mental health startup UpLift announced it acquired a women-focused digital psychiatry platform. The New York-based companies will allow California, Illinois, Pennsylvania, New York, and Texas residents to access Uplift's platform, which will now include team-based therapy and psychiatric care.

- In February 2022, IBM acquired Neudesic, LLC, which was aimed at expanding IBM's portfolio of hybrid multi-cloud services and further advancing the company's hybrid cloud and AI strategy.

- In February 2022, Lyniate acquired SAP SE to provide technology and consulting expertise to make it easier for clients to embrace a hybrid cloud approach and move mission-critical workloads from SAP solutions to the cloud for regulated and non-regulated industries.

- In January 2022, Francisco Partners signed an agreement with IBM to acquire healthcare data and analytics assets from IBM that are currently part of the Watson Health business, including Health Insights, MarketScan, Clinical Development, Social Program Management, Micromedex, and imaging software offerings.

- In January 2022, IBM acquired ENVIZI aimed at building on IBM's growing investments in AI-powered Software.

- In September 2022, LifePoint Health, a diversified healthcare delivery network dedicated to making communities healthier, and Google Cloud entered a multi-year strategic partnership to transform healthcare delivery in communities across the United States through LifePoint's implementation of Google Cloud's Healthcare Data Engine (HDE).

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Application, Service, Deployment, End Users, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

TABLE OF CONTENTS

1. INTRODUCTION

1.1. SCOPE OF THE STUDY

1.2. THE INSIGHT PARTNERS RESEARCH REPORT GUIDANCE

1.3. MARKET SEGMENTATION

1.3.1 Healthcare Cloud Computing Market - By Service

1.3.2 Healthcare Cloud Computing Market - By Deployment Model

1.3.3 Healthcare Cloud Computing Market - By Application

1.3.4 Healthcare Cloud Computing Market - By Region

1.3.4.1 By Country

2. KEY TAKEAWAYS

3. RESEARCH METHODOLOGY

4. HEALTHCARE CLOUD COMPUTING MARKET LANDSCAPE

4.1. OVERVIEW

4.2. PEST ANALYSIS

4.2.1 North America - Pest Analysis

4.2.2 Europe - Pest Analysis

4.2.3 Asia-Pacific - Pest Analysis

4.2.4 Middle East and Africa - Pest Analysis

4.2.5 South and Central America - Pest Analysis

4.3. EXPERT OPINIONS

5. HEALTHCARE CLOUD COMPUTING MARKET - KEY MARKET DYNAMICS

5.1. KEY MARKET DRIVERS

5.2. KEY MARKET RESTRAINTS

5.3. KEY MARKET OPPORTUNITIES

5.4. FUTURE TRENDS

5.5. IMPACT ANALYSIS OF DRIVERS AND RESTRAINTS

6. HEALTHCARE CLOUD COMPUTING MARKET - GLOBAL MARKET ANALYSIS

6.1. HEALTHCARE CLOUD COMPUTING - GLOBAL MARKET OVERVIEW

6.2. HEALTHCARE CLOUD COMPUTING - GLOBAL MARKET AND FORECAST TO 2028

6.3. MARKET POSITIONING

7. HEALTHCARE CLOUD COMPUTING MARKET - REVENUE AND FORECASTS TO 2028 - SERVICE

7.1. OVERVIEW

7.2. SERVICE MARKET FORECASTS AND ANALYSIS

7.3. SOFTWARE-AS-A-SERVICE (SAAS)

7.3.1. Overview

7.3.2. Software-As-A-Service (SAAS) Market Forecast and Analysis

7.4. PLATFORM-AS-A-SERVICE (PAAS)

7.4.1. Overview

7.4.2. Platform-As-A-Service (PAAS) Market Forecast and Analysis

7.5. INFRASTRUCTURE-AS-A-SERVICE (IAAS)

7.5.1. Overview

7.5.2. Infrastructure-As-A-Service (IAAS) Market Forecast and Analysis

8. HEALTHCARE CLOUD COMPUTING MARKET - REVENUE AND FORECASTS TO 2028 - DEPLOYMENT MODEL

8.1. OVERVIEW

8.2. DEPLOYMENT MODEL MARKET FORECASTS AND ANALYSIS

8.3. PUBLIC CLOUD

8.3.1. Overview

8.3.2. Public Cloud Market Forecast and Analysis

8.4. PRIVATE CLOUD

8.4.1. Overview

8.4.2. Private Cloud Market Forecast and Analysis

8.5. HYBRID CLOUD

8.5.1. Overview

8.5.2. Hybrid Cloud Market Forecast and Analysis

9. HEALTHCARE CLOUD COMPUTING MARKET - REVENUE AND FORECASTS TO 2028 - APPLICATION

9.1. OVERVIEW

9.2. APPLICATION MARKET FORECASTS AND ANALYSIS

9.3. CLINICAL INFORMATION SYSTEMS MARKET

9.3.1. Overview

9.3.2. Clinical Information Systems Market Market Forecast and Analysis

9.3.3. Pharmacy Information System Market Market

9.3.3.1. Overview

9.3.3.2. Pharmacy Information System Market Market Forecast and Analysis

9.3.4. Electronic Medical Records Market Market

9.3.4.1. Overview

9.3.4.2. Electronic Medical Records Market Market Forecast and Analysis

9.3.5. Radiology Information System Market Market

9.3.5.1. Overview

9.3.5.2. Radiology Information System Market Market Forecast and Analysis

9.3.6. Computerized Physician Order Entry (CPOE) Market Market

9.3.6.1. Overview

9.3.6.2. Computerized Physician Order Entry (CPOE) Market Market Forecast and Analysis

9.3.7. Others Market Market

9.3.7.1. Overview

9.3.7.2. Others Market Market Forecast and Analysis

9.4. NON-CLINICAL INFORMATION SYSTEMS MARKET

9.4.1. Overview

9.4.2. Non-Clinical Information Systems Market Market Forecast and Analysis

9.4.3. Cost Accounting Market Market

9.4.3.1. Overview

9.4.3.2. Cost Accounting Market Market Forecast and Analysis

9.4.4. Payroll Management Systems Market Market

9.4.4.1. Overview

9.4.4.2. Payroll Management Systems Market Market Forecast and Analysis

9.4.5. Revenue Cycle Management (RCM) Market Market

9.4.5.1. Overview

9.4.5.2. Revenue Cycle Management (RCM) Market Market Forecast and Analysis

9.4.6. Automatic Patient Billing (APB) Market Market

9.4.6.1. Overview

9.4.6.2. Automatic Patient Billing (APB) Market Market Forecast and Analysis

9.4.7. Others Market Market

9.4.7.1. Overview

9.4.7.2. Others Market Market Forecast and Analysis

10. HEALTHCARE CLOUD COMPUTING MARKET REVENUE AND FORECASTS TO 2028 - GEOGRAPHICAL ANALYSIS

10.1. NORTH AMERICA

10.1.1 North America Healthcare Cloud Computing Market Overview

10.1.2 North America Healthcare Cloud Computing Market Forecasts and Analysis

10.1.3 North America Healthcare Cloud Computing Market Forecasts and Analysis - By Service

10.1.4 North America Healthcare Cloud Computing Market Forecasts and Analysis - By Deployment Model

10.1.5 North America Healthcare Cloud Computing Market Forecasts and Analysis - By Application

10.1.6 North America Healthcare Cloud Computing Market Forecasts and Analysis - By Countries

10.1.6.1 United States Healthcare Cloud Computing Market

10.1.6.1.1 United States Healthcare Cloud Computing Market by Service

10.1.6.1.2 United States Healthcare Cloud Computing Market by Deployment Model

10.1.6.1.3 United States Healthcare Cloud Computing Market by Application

10.1.6.2 Canada Healthcare Cloud Computing Market

10.1.6.2.1 Canada Healthcare Cloud Computing Market by Service

10.1.6.2.2 Canada Healthcare Cloud Computing Market by Deployment Model

10.1.6.2.3 Canada Healthcare Cloud Computing Market by Application

10.1.6.3 Mexico Healthcare Cloud Computing Market

10.1.6.3.1 Mexico Healthcare Cloud Computing Market by Service

10.1.6.3.2 Mexico Healthcare Cloud Computing Market by Deployment Model

10.1.6.3.3 Mexico Healthcare Cloud Computing Market by Application

10.2. EUROPE

10.2.1 Europe Healthcare Cloud Computing Market Overview

10.2.2 Europe Healthcare Cloud Computing Market Forecasts and Analysis

10.2.3 Europe Healthcare Cloud Computing Market Forecasts and Analysis - By Service

10.2.4 Europe Healthcare Cloud Computing Market Forecasts and Analysis - By Deployment Model

10.2.5 Europe Healthcare Cloud Computing Market Forecasts and Analysis - By Application

10.2.6 Europe Healthcare Cloud Computing Market Forecasts and Analysis - By Countries

10.2.6.1 Germany Healthcare Cloud Computing Market

10.2.6.1.1 Germany Healthcare Cloud Computing Market by Service

10.2.6.1.2 Germany Healthcare Cloud Computing Market by Deployment Model

10.2.6.1.3 Germany Healthcare Cloud Computing Market by Application

10.2.6.2 France Healthcare Cloud Computing Market

10.2.6.2.1 France Healthcare Cloud Computing Market by Service

10.2.6.2.2 France Healthcare Cloud Computing Market by Deployment Model

10.2.6.2.3 France Healthcare Cloud Computing Market by Application

10.2.6.3 Italy Healthcare Cloud Computing Market

10.2.6.3.1 Italy Healthcare Cloud Computing Market by Service

10.2.6.3.2 Italy Healthcare Cloud Computing Market by Deployment Model

10.2.6.3.3 Italy Healthcare Cloud Computing Market by Application

10.2.6.4 Spain Healthcare Cloud Computing Market

10.2.6.4.1 Spain Healthcare Cloud Computing Market by Service

10.2.6.4.2 Spain Healthcare Cloud Computing Market by Deployment Model

10.2.6.4.3 Spain Healthcare Cloud Computing Market by Application

10.2.6.5 United Kingdom Healthcare Cloud Computing Market

10.2.6.5.1 United Kingdom Healthcare Cloud Computing Market by Service

10.2.6.5.2 United Kingdom Healthcare Cloud Computing Market by Deployment Model

10.2.6.5.3 United Kingdom Healthcare Cloud Computing Market by Application

10.2.6.6 Rest of Europe Healthcare Cloud Computing Market

10.2.6.6.1 Rest of Europe Healthcare Cloud Computing Market by Service

10.2.6.6.2 Rest of Europe Healthcare Cloud Computing Market by Deployment Model

10.2.6.6.3 Rest of Europe Healthcare Cloud Computing Market by Application

10.3. ASIA-PACIFIC

10.3.1 Asia-Pacific Healthcare Cloud Computing Market Overview

10.3.2 Asia-Pacific Healthcare Cloud Computing Market Forecasts and Analysis

10.3.3 Asia-Pacific Healthcare Cloud Computing Market Forecasts and Analysis - By Service

10.3.4 Asia-Pacific Healthcare Cloud Computing Market Forecasts and Analysis - By Deployment Model

10.3.5 Asia-Pacific Healthcare Cloud Computing Market Forecasts and Analysis - By Application

10.3.6 Asia-Pacific Healthcare Cloud Computing Market Forecasts and Analysis - By Countries

10.3.6.1 Australia Healthcare Cloud Computing Market

10.3.6.1.1 Australia Healthcare Cloud Computing Market by Service

10.3.6.1.2 Australia Healthcare Cloud Computing Market by Deployment Model

10.3.6.1.3 Australia Healthcare Cloud Computing Market by Application

10.3.6.2 China Healthcare Cloud Computing Market

10.3.6.2.1 China Healthcare Cloud Computing Market by Service

10.3.6.2.2 China Healthcare Cloud Computing Market by Deployment Model

10.3.6.2.3 China Healthcare Cloud Computing Market by Application

10.3.6.3 India Healthcare Cloud Computing Market

10.3.6.3.1 India Healthcare Cloud Computing Market by Service

10.3.6.3.2 India Healthcare Cloud Computing Market by Deployment Model

10.3.6.3.3 India Healthcare Cloud Computing Market by Application

10.3.6.4 Japan Healthcare Cloud Computing Market

10.3.6.4.1 Japan Healthcare Cloud Computing Market by Service

10.3.6.4.2 Japan Healthcare Cloud Computing Market by Deployment Model

10.3.6.4.3 Japan Healthcare Cloud Computing Market by Application

10.3.6.5 South Korea Healthcare Cloud Computing Market

10.3.6.5.1 South Korea Healthcare Cloud Computing Market by Service

10.3.6.5.2 South Korea Healthcare Cloud Computing Market by Deployment Model

10.3.6.5.3 South Korea Healthcare Cloud Computing Market by Application

10.3.6.6 Rest of Asia-Pacific Healthcare Cloud Computing Market

10.3.6.6.1 Rest of Asia-Pacific Healthcare Cloud Computing Market by Service

10.3.6.6.2 Rest of Asia-Pacific Healthcare Cloud Computing Market by Deployment Model

10.3.6.6.3 Rest of Asia-Pacific Healthcare Cloud Computing Market by Application

10.4. MIDDLE EAST AND AFRICA

10.4.1 Middle East and Africa Healthcare Cloud Computing Market Overview

10.4.2 Middle East and Africa Healthcare Cloud Computing Market Forecasts and Analysis

10.4.3 Middle East and Africa Healthcare Cloud Computing Market Forecasts and Analysis - By Service

10.4.4 Middle East and Africa Healthcare Cloud Computing Market Forecasts and Analysis - By Deployment Model

10.4.5 Middle East and Africa Healthcare Cloud Computing Market Forecasts and Analysis - By Application

10.4.6 Middle East and Africa Healthcare Cloud Computing Market Forecasts and Analysis - By Countries

10.4.6.1 South Africa Healthcare Cloud Computing Market

10.4.6.1.1 South Africa Healthcare Cloud Computing Market by Service

10.4.6.1.2 South Africa Healthcare Cloud Computing Market by Deployment Model

10.4.6.1.3 South Africa Healthcare Cloud Computing Market by Application

10.4.6.2 Saudi Arabia Healthcare Cloud Computing Market

10.4.6.2.1 Saudi Arabia Healthcare Cloud Computing Market by Service

10.4.6.2.2 Saudi Arabia Healthcare Cloud Computing Market by Deployment Model

10.4.6.2.3 Saudi Arabia Healthcare Cloud Computing Market by Application

10.4.6.3 U.A.E Healthcare Cloud Computing Market

10.4.6.3.1 U.A.E Healthcare Cloud Computing Market by Service

10.4.6.3.2 U.A.E Healthcare Cloud Computing Market by Deployment Model

10.4.6.3.3 U.A.E Healthcare Cloud Computing Market by Application

10.4.6.4 Rest of Middle East and Africa Healthcare Cloud Computing Market

10.4.6.4.1 Rest of Middle East and Africa Healthcare Cloud Computing Market by Service

10.4.6.4.2 Rest of Middle East and Africa Healthcare Cloud Computing Market by Deployment Model

10.4.6.4.3 Rest of Middle East and Africa Healthcare Cloud Computing Market by Application

10.5. SOUTH AND CENTRAL AMERICA

10.5.1 South and Central America Healthcare Cloud Computing Market Overview

10.5.2 South and Central America Healthcare Cloud Computing Market Forecasts and Analysis

10.5.3 South and Central America Healthcare Cloud Computing Market Forecasts and Analysis - By Service

10.5.4 South and Central America Healthcare Cloud Computing Market Forecasts and Analysis - By Deployment Model

10.5.5 South and Central America Healthcare Cloud Computing Market Forecasts and Analysis - By Application

10.5.6 South and Central America Healthcare Cloud Computing Market Forecasts and Analysis - By Countries

10.5.6.1 Brazil Healthcare Cloud Computing Market

10.5.6.1.1 Brazil Healthcare Cloud Computing Market by Service

10.5.6.1.2 Brazil Healthcare Cloud Computing Market by Deployment Model

10.5.6.1.3 Brazil Healthcare Cloud Computing Market by Application

10.5.6.2 Argentina Healthcare Cloud Computing Market

10.5.6.2.1 Argentina Healthcare Cloud Computing Market by Service

10.5.6.2.2 Argentina Healthcare Cloud Computing Market by Deployment Model

10.5.6.2.3 Argentina Healthcare Cloud Computing Market by Application

10.5.6.3 Rest of South and Central America Healthcare Cloud Computing Market

10.5.6.3.1 Rest of South and Central America Healthcare Cloud Computing Market by Service

10.5.6.3.2 Rest of South and Central America Healthcare Cloud Computing Market by Deployment Model

10.5.6.3.3 Rest of South and Central America Healthcare Cloud Computing Market by Application

11. IMPACT OF COVID-19 PANDEMIC ON GLOBAL HEALTHCARE CLOUD COMPUTING MARKET

11.1 North America

11.2 Europe

11.3 Asia-Pacific

11.4 Middle East and Africa

11.5 South and Central America

12. INDUSTRY LANDSCAPE

12.1. MERGERS AND ACQUISITIONS

12.2. AGREEMENTS, COLLABORATIONS AND JOIN VENTURES

12.3. NEW PRODUCT LAUNCHES

12.4. EXPANSIONS AND OTHER STRATEGIC DEVELOPMENTS

13. HEALTHCARE CLOUD COMPUTING MARKET, KEY COMPANY PROFILES

13.1. DELL INC

13.1.1. Key Facts

13.1.2. Business Description

13.1.3. Products and Services

13.1.4. Financial Overview

13.1.5. SWOT Analysis

13.1.6. Key Developments

13.2. CARESTREAM HEALTH

13.2.1. Key Facts

13.2.2. Business Description

13.2.3. Products and Services

13.2.4. Financial Overview

13.2.5. SWOT Analysis

13.2.6. Key Developments

13.3. VMWARE, INC

13.3.1. Key Facts

13.3.2. Business Description

13.3.3. Products and Services

13.3.4. Financial Overview

13.3.5. SWOT Analysis

13.3.6. Key Developments

13.4. IRON MOUNTAIN INCORPORATED

13.4.1. Key Facts

13.4.2. Business Description

13.4.3. Products and Services

13.4.4. Financial Overview

13.4.5. SWOT Analysis

13.4.6. Key Developments

13.5. CLEARDATA

13.5.1. Key Facts

13.5.2. Business Description

13.5.3. Products and Services

13.5.4. Financial Overview

13.5.5. SWOT Analysis

13.5.6. Key Developments

13.6. CARECLOUD CORPORATION

13.6.1. Key Facts

13.6.2. Business Description

13.6.3. Products and Services

13.6.4. Financial Overview

13.6.5. SWOT Analysis

13.6.6. Key Developments

13.7. IBM WATSON HEALTH

13.7.1. Key Facts

13.7.2. Business Description

13.7.3. Products and Services

13.7.4. Financial Overview

13.7.5. SWOT Analysis

13.7.6. Key Developments

13.8. GLOBAL NET ACCESS (GNAX)

13.8.1. Key Facts

13.8.2. Business Description

13.8.3. Products and Services

13.8.4. Financial Overview

13.8.5. SWOT Analysis

13.8.6. Key Developments

13.9. ATHENAHEALTH, INC

13.9.1. Key Facts

13.9.2. Business Description

13.9.3. Products and Services

13.9.4. Financial Overview

13.9.5. SWOT Analysis

13.9.6. Key Developments

13.10. MERGE HEALTHCARE, INC

13.10.1. Key Facts

13.10.2. Business Description

13.10.3. Products and Services

13.10.4. Financial Overview

13.10.5. SWOT Analysis

13.10.6. Key Developments

13.11. MERGE HEALTHCARE, INC

13.11.1. Key Facts

13.11.2. Business Description

13.11.3. Products and Services

13.11.4. Financial Overview

13.11.5. SWOT Analysis

13.11.6. Key Developments

14. APPENDIX

14.1. ABOUT THE INSIGHT PARTNERS

14.2. GLOSSARY OF TERMS

The List of Companies

1. Global Net Access (GNAX)

2. Carecloud Corporation

3. Dell Inc.

4. Athenahealth, Inc.

5. Carestream Health, Inc.

6. VMWare, Inc.

7. Iron Mountain, Inc.

8. IBM Corporation

9. Cleardata Networks, Inc.

10. Merge Healthcare, Inc.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For