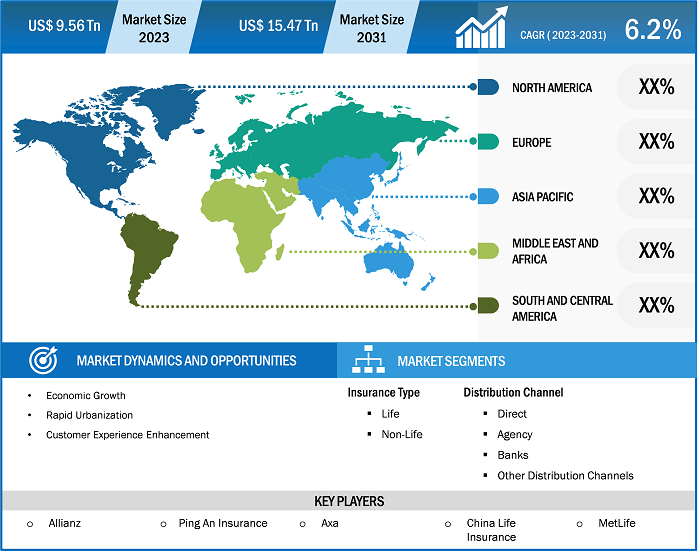

The life and non-life insurance market size is expected to grow from US$ 9561.30 billion in 2023 to US$ 15470.81 billion by 2031; it is anticipated to expand at a CAGR of 6.2% from 2023 to 2031. Currently, the global market has been experiencing volatility, which can be attributed to ever-changing geo-political conditions, climate change, technology shifts, and customer behavior. This has pushed enterprises across the globe to revisit company strategies and revise their business models, organizational culture, and tech infrastructure, among others. In the wake of these developments, the insurance industry has also been evolving to support the risks entailing such changes in enterprises and consumer behavior.

Life and Non-Life Insurance Market Analysis

The life and non-life insurance market forecast is estimated on the basis of various secondary and primary research findings, such as key company publications, association data, and databases. Economic growth, an expanding middle class, innovation, and regulatory assistance are propelling the insurance business forward. The revenue of the global life and non-life insurance market is a function of the economic conditions of developed and developing economies. The insurance industry is an important part of the economy because of the number of premiums it collects, the size of its investments, and, more importantly, the critical social and economic function it plays in covering personal and company risks. Globalization has evolved in recent decades as a result of the expansion of commercial and financial networks that cross national borders, making businesses and workers from other economies increasingly interconnected. Greater globalization creates more chances for international investments, resulting in more investment-linked programs. Globalization has also led to an increase in immigrant numbers. There will be more people in the population eager to sign up for insurance products, creating greater prospects for a company.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Life and Non-Life Insurance Market: Strategic Insights

Market Size Value in US$ 9561.30 billion in 2023 Market Size Value by US$ 15470.81 billion by 2031 Growth rate CAGR of 6.2% from 2023 to 2031 Forecast Period 2023-2031 Base Year 2023

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Life and Non-Life Insurance Market: Strategic Insights

| Market Size Value in | US$ 9561.30 billion in 2023 |

| Market Size Value by | US$ 15470.81 billion by 2031 |

| Growth rate | CAGR of 6.2% from 2023 to 2031 |

| Forecast Period | 2023-2031 |

| Base Year | 2023 |

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Life and Non-Life Insurance

Industry Overview

- Insurance businesses are also beginning to suffer centralization processes as a result of collaborations with banks and reinsurance companies, as well as mergers with smaller and larger competitors.

- The number and variety of insurance services and products are also expanding. For example, we're seeing insurance solutions for newer risks, including informational risk, political risk, security risk, and even military risk.

- InsurTech, like FinTech, is disrupting the financial business. As the insurance business embraces technology innovation and eCommerce, we expect to see more insurance products sold online.

- Urbanization is another factor that has a major influence on the state of the global life and non-life insurance market globally. Urbanization entails massive infrastructure investments, high pace industrialization, and growing population density. This has major risk management and insurance implications. Urbanization brings socio-economic developments, including increased social mobility, education possibilities, and formal employment, which will benefit the life and non-life insurance market growth.

Life and Non-Life Insurance Market Driver

Developments in the InsurTech Industry to Drive the Life and Non-Life Insurance Market

- The insurance industry is undergoing a fundamental transformation fueled by technology and the adoption of innovative InsurTech solutions. As the industry evolves, insurers' ability to fully leverage these disruptive technologies will be critical to keeping ahead of the curve.

- InsurTech visionaries are pioneering innovative insurance technology solutions to address policyholders' increasing needs while streamlining their existing processes. The sector, formerly known for its conventional traditions and paper-intensive processes, is now embracing technology in new ways. For instance, in February 2024, Wipro, a prominent IT business located in Bengaluru, paid $66 million for Aggne, a consultancy and managed services firm that serves the insurance and InsurTech industries. With this, the company aimed at strengthening its P&C insurance sector capabilities. Also, according to a 2023 survey by Delloite, over 86 percent of CE insurers believe that cooperation with InsurTechs can boost their technical development. This has been driving the life and non-life insurance market growth.

- Moreover, the integration of AI and ML technologies into the InsurTech platforms is expected to bring new life and non-life insurance market trends.

Life and Non-Life Insurance

Market Report Segmentation Analysis

- Based on insurance type, the life and non-life insurance market is segmented into life and non-life. The non-life segment is expected to hold a substantial life and non-life insurance market share in 2023.

- Non-life insurance, often known as general insurance, covers assets such as a car, home, travel, accidents, etc. Health insurance in the segment driving the growth in the non-life insurance sector. This can be attributed to the rapid urbanization and rise in disposable income in the hands of the urban workforce. Also, in many countries, investing in health insurance also offers tax benefits, thus driving the non-life insurance market.

Life and Non-Life Insurance

Market Analysis by Geography

The scope of the life and non-life insurance market report is primarily divided into five regions - North America, Europe, Asia Pacific, Middle East & Africa, and South America. Asia Pacific (APAC) is experiencing rapid growth and is anticipated to hold a significant life and non-life insurance market share. The region's significant economic development, growing population, and increasing focus on risk management and insurance have contributed to this growth. APAC is home to many developing countries like India and China, driving the growth of the market.

Life and Non-Life Insurance

Market Report Scope

The "Life and Non-Life Insurance Market Analysis" was carried out based on insurance type, distribution channel, and geography. In terms of insurance type, the market is segmented into life and non-life. Based on distribution channels, the life and non-life insurance market is segmented into direct, agency, banks, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

Life and Non-Life Insurance

Market News and Recent Developments

Companies adopt inorganic and organic strategies such as mergers and acquisitions in the life and non-life insurance market. A few recent key market developments are listed below:

- In January 2024, Generali, Italy's largest insurer, announced that it would take full control of a non-life insurance joint venture in China by buying out local partner CNPC Capital for approximately 99 million euros (US$108 million). Generali announced plans to expand its distribution network in China, focusing on green business insurance to capitalize on the country's goal of becoming carbon neutral by 2060. The acquisition of a 51% holding in Generali China Insurance (GCI) comes after CNPC Capital announced in November that it will run a public sale for its stake in its collaboration with the Italian insurer. According to Generali, this is the first time a foreign insurer has acquired a controlling position in a Chinese property and casualty insurer from a single state-owned business through a public auction.

[Source: Assicurazioni Generali S.p.A., Company Website]

- In October 2022, Berkshire Hathaway Inc. and Alleghany Corporation announced the completion of Berkshire Hathaway's acquisition of Alleghany. Holders of Alleghany common stock, as of immediately prior to the closing of the transaction, were entitled to receive $848.02 per share in cash, representing a total equity value of approximately $11.6 billion. Upon the closing of the transaction, Alleghany became a wholly-owned subsidiary of Berkshire Hathaway. Alleghany continues to be led by Joe Brandon. Goldman Sachs & Co. LLC served as a financial advisor, and Willkie Farr & Gallagher LLP served as a legal advisor to Alleghany. Munger, Tolles & Olson LLP served as legal advisor to Berkshire Hathaway.

[Source: Berkshire Hathaway Inc., Company Website]

Life and Non-Life Insurance

Market Report Coverage & Deliverables

The market report "Life and Non-Life Insurance Market Size and Forecast (2021–2031)" provides a detailed analysis of the market covering below areas-

- Market size & forecast at global, regional, and country levels for all the key market segments covered under the scope.

- Market dynamics such as drivers, restraints, and key opportunities.

- Key future trends.

- Detailed PEST & SWOT analysis

- Global and regional market analysis covering key market trends, key players, regulations, and recent market developments.

- Industry landscape and competition analysis covering market concentration, heat map analysis, key players, and recent developments.

- Detailed company profiles.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Insurance Type, Distribution Channel, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

Digital transformation is anticipated to play a significant role in the global Life and Non-Life Insurance market in the coming years.

Economic growth and rapid urbanization are the major factors that propel the global Life and Non-Life Insurance market.

The global Life and Non-Life Insurance market is expected to reach US$ 15470.81 billion by 2031.

The key players holding majority shares in the global Life and Non-Life Insurance market are Allianz; Ping An Insurance; Axa; China Life Insurance; MetLife; United Health Group; Cigna; Aia; Berkshire Hathway; Zurich Insurance Group.

The global Life and Non-Life Insurance market was estimated to be US$ 9561.30 billion in 2023 and is expected to grow at a CAGR of 6.2% during the forecast period 2023 - 2031.

- Allianz

- Ping An Insurance

- Axa

- China Life Insurance

- MetLife

- United Health Group

- Cigna

- Aia

- Berkshire Hathway

- Zurich Insurance Group

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For