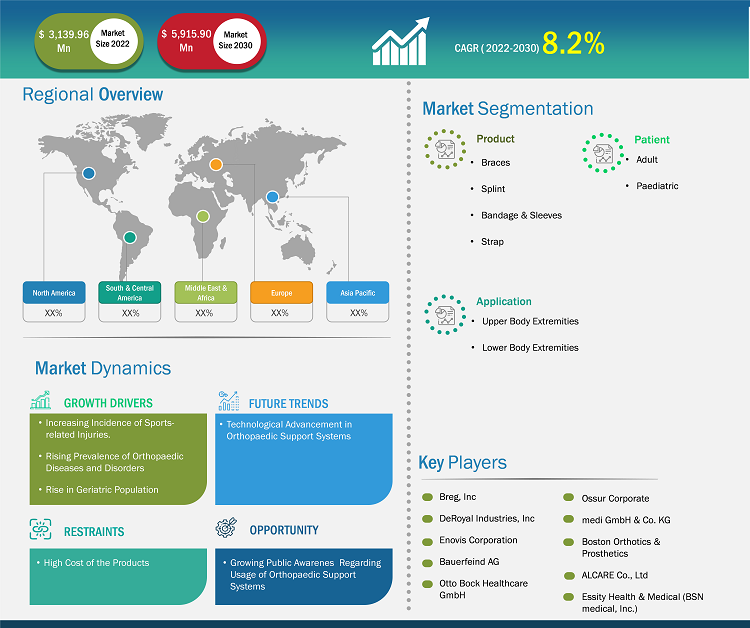

[Research Report] Orthopedic support systems market size is projected to grow from US$ 3,139.96 million in 2022 to US$ 5,915.90 million by 2031; it is estimated to record a CAGR of 8.2% during 2022–2031.

Market Insights and Analyst View:

Orthopedic support systems can help with pain and immobility in the hands, elbows, back, knees, or ankles. In orthopedics, they are used to promote, restore, or support movement within the body and are used in the treatment and prevention of injuries, medical conditions, and damage to the body's motor system. The braces and supports are available in knee braces, ankle braces, leg braces, elbow braces, tennis elbow braces, wrist braces, thumb and hand splints, back and shoulder braces, and many more. The orthopedic support systems market is majorly driven by factors such as growing incidences of orthopedic disorders and diseases, the rise in sports and accident-related injuries cases, rise in the geriatric population, and technological advancement in orthopedic braces and supports. Increasing technological advancements that enable the launch of innovative braces and supports for patients are expected to drive the orthopedic supports systems market due to the comfort and ease of mobility offered to patients. Companies are constantly involved in selling their innovative products through off-the-shelf and e-commerce platforms, which have paved the way for significant growth opportunities for the players operating in the orthopedic braces and support systems field.

Growth Drivers:

Playing sports benefits adolescents physiologically, psychologically, and socially. It helps improve health conditions, self-esteem, and social interactions. However, as the number of sports increases, so does the number of sports-related injuries. Sports injuries are a main issue for athletes, coaches, and sports clubs, which negatively affect the health of the injured athlete. More than 30 million children and teens in the US participated in organized sports in 2021, out of which one-third were reported with sports-related injuries, according to Stanford Medicine Children's Health. In addition, ~3.5 million injuries occur in children each year in the country while playing sports or participating in recreational activities, and ~75,000 children aged 14 and below are treated for these injuries. In the US alone, 3.5 million youth under 15 receive medical care every year for injuries caused during sports practice.

In addition, these injuries burden the healthcare system as the management of such injuries is usually expensive and time-consuming. Handball is a pivoting team sport in which players are mostly affected by injuries and can lead to musculoskeletal injuries. As per a study titled "Prevalence and Determinants of Sports Injuries among the Egyptian National Handball Players," published in August 2022, knee injuries represent the greatest share of extensive injuries in these players. As per a cross-sectional study carried out on all the Egyptian National handball players, ~83% of the total national handball players suffered from one or more sports injuries, 81% of them were injured once, and 40% of total injuries were overuse injuries. The most frequent injured sites were the knee (47.5%), followed by the ankle (19%) and shoulder (13%).

Moreover, the lower extremity accounts for the majority of sports injuries around the world. According to the Federation Internationale de Football Association (FIFA), an ankle sprain is the most common injury sustained by football players globally. Such injuries are expected to generate substantial demand for ankle braces. Ankle braces are recommended after an acute ankle sprain to aid in recovery and help prevent ankle injuries such as sprains, fractures, and tendonitis.

Thus, a high participation rate in sports (both children and adults), coupled with an increase in sports injuries, is creating the demand for orthopedic support systems globally. Athletes also use orthopedic braces to safeguard themselves from further injury during sports activities. It helps them limit unwanted movement during competitions, thereby facilitating convenient play. Therefore, increasing sports injuries drives the growth of the orthopedic support systems market.

Strategic Insights

Report Segmentation and Scope:

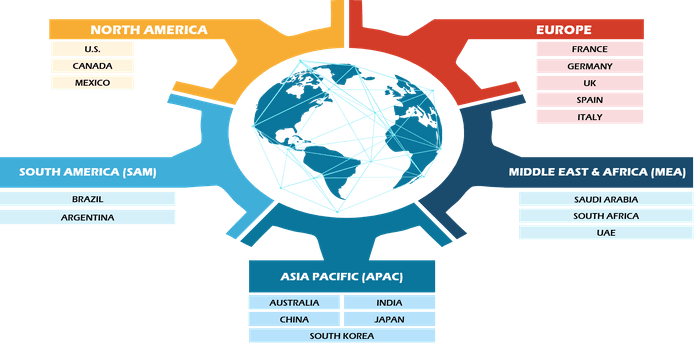

The “Global Orthopedic Support Systems Market” is segmented based on product, patient, application, and geography. Based on product, the orthopedic support systems market is segmented into braces, splint, bandage & sleeves, and strap. Based on patient, the orthopedic support systems market is categorized into adult and paediatric. Based on application, the orthopedic support systems market is segmented into upper body extremities and lower body extremities. The orthopedic support systems market, based on geography is segmented into North America (US, Canada, and Mexico), Europe (Germany, France, Italy, UK, Spain, and Rest of Europe), Asia Pacific (Australia, China, Japan, India, South Korea, and Rest of Asia Pacific), Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Segmental Analysis:

The orthopedic support systems market, by product, is segmented into braces, splint, bandage & sleeves, and strap. The braces segment held the largest share of the market in 2022. Braces segment is growing due to the rising usage of knee braces and their high demand due to the growing number of knee surgeries related to knee injuries such as anterior cruciate ligament (ACL), runner’s knee, patella tendonitis, and torn knee cartilage. Knee brace demand is growing because it is used as a follow-up treatment after knee surgery associated with injuries. Growing number of the target population affected by knee joint-related ailments benefit from knee braces as it helps in pressure relief from knee joints affected by arthritis. Orthopedic doctors also recommend ankle braces to patients for the treatment of acute ankle sprain. Athletes wear an orthopedic brace to prevent further injury during sports activities, prevent unwanted movement during matches, and make play easier.

Based on patient, the orthopedic support systems market is segmented into adult and paediatric. The paediatric segment held the largest market share in 2022. The growth of the segment is due to the rising number of child injuries. Child injuries are a growing global health problem and require immediate attention. Unintentional injuries make up for 90% of child injuries. These injuries are a significant healthcare problem that needs immediate attention. Moreover, the number of children born with musculoskeletal and bone disorders such as spinal and limb deformities is rapidly growing, which is elevating the need for orthopedic support systems worldwide to treat the pediatric patient population. In addition, the growing enthusiasm among the pediatric population to participate in sports activities is associated with sports-related injuries. These factors potentially boost the demand for orthopedic support systems across the globe for these patients.

Based on application, the orthopedic support systems market is segmented into upper body extremities and lower body extremities. The lower body extremities segment held the largest market share in 2022. The growth of the segment is associated with a growing geriatric population suffering from lower body problems, including knee-related disorders such as osteoarthritis and the rise of lower body disabilities. The causes of osteoarthritis are dislocation of joints, ligament injuries, and torn cartilage; in addition to obesity and poor posture, joint malformation can also result in osteoarthritis. The severe osteoarthritis shows symptoms such as severe & increased pain, increased swelling & inflammation, joint instability, and decreased range of movements. The growing need to support the weak ligament contributes to the rising global demand for orthopedic braces and support systems. To treat the condition, braces are prescribed by the doctors. The braces enhance stability, reduce swelling & pain, reduce pressure, and increase confidence in the patients to move independently. The braces used to treat osteoarthritis conditions are prophylactic, unloader, rehabilitative, functional, or supportive. These braces are custom-made, which provides better comfort and better movement.

Regional Analysis:

Based on geography, the orthopedic support systems market is divided into five key regions: North America, Europe, Asia Pacific, South & Central America, and Middle East & Africa. North America is likely to acquire a significant share of the global market in 2022. The market growth in the region is attributed to the increasing geriatric population, growing developments by the market players for orthopedic braces and supports, growing awareness about product availability, and rising adoption of orthopedic braces to offer mobility and prevent further injury in the ligament. According to the facts provided by the National Safety Council, a US-based non-profit organization, exercise-related injuries accounted for ~468,000 injuries in 2021. In addition, the US government offers various funds and support for the usage of orthopedic braces & support and various programs for the betterment of the population. For instance, the Orthopedic Research Program (US) supports clinical, epidemiological, and outcomes research in orthopedics and musculoskeletal rehabilitation. Such initiatives are expected to drive the demand for orthopedic braces and supports.

The increasing geriatric population is one factor propelling the market's growth. According to the National Institutes of Health (NIH) report, America’s 65-and-over population is projected to nearly double over the next three decades, from 48 million to 88 million by 2050. As per SingleCare article data, ~350 million people have arthritis worldwide. Per the same source, a quarter of American adults have arthritis. 1 in 4 adults in the US have arthritis in 2021, and the number of US adults suffering from arthritis is estimated to reach 78 million by 2040. Therefore, the high rate of age-related problems, increasing government support for funding, and awareness of orthopedic braces and supports indicate the potential growth for wider adoption of the orthopedic support system products in the region.

Moreover, Europe is the second leading region in the global orthopedic support systems market. The Europe orthopedic braces and supports market is in a growth phase due to the rising aging population, increasing focus of market players in Germany and France, grants & funds by the government, and rising number of conferences in the UK. These factors upsurge the orthopedic support systems adoption in the region. In addition, the rising prevalence of osteoarthritis also promotes the growth of the market in Europe.

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global orthopedic support systems market are listed below:

- In April 2023, DJO Global Inc. (now known as Envois) expanded its ankle and foot portfolio with a knotless syndesmotic repair system by launching Enofix with Constrictor technology. This technology is a repair system demonstrating superior fixation under cyclic loading and is useful in stabilizing syndesmosis, thus making an effective contribution to the field of orthopedic braces and supports.

- In September 2021, Ossur, a global orthotics and prosthetics industry leader, launched the Rebound ACL brace, designed to help patients recovering from anterior cruciate ligament (ACL) injury. The brace’s proprietary Dynamic Tension System (DTS) allows for custom, adjustable settings based on individual anatomy and rehabilitation needs, whether the patient is undergoing non-surgical conservative treatment approaches or recovering from post-operative reconstruction.

- In February 2021, Breg, Inc. launched two new lines of spinal orthoses (braces) products under the brand names Pinnacle and Ascenda. Breg is the leading orthopedic bracing and billing services company, which has developed 15 products to elevate care for patients with spinal injuries.

- In June 2021, DJO launched the DonJoy X-ROM Post-Op Knee Brace into the market. The knee brace features the most advanced range of motion protection, and its design is improved for ease of user and easier application and adjustment. The X-ROM brace technology allows patients to recover faster from ACL repair and other knee surgeries. In addition, it improves patients’ confidence, comfort, and stability.

Competitive Landscape and Key Companies:

Breg, Inc; DeRoyal Industries, Inc; Enovis Corporation; Bauerfeind AG; Otto Bock Healthcare GmbH; Ossur Corporate; medi GmbH & Co. KG; Boston Orthotics & Prosthetics; Essity Health & Medical (BSN medical, Inc); and ALCARE Co., Ltd are the major orthopedic braces and support systems companies. These companies focus on various growth strategies such as new technologies, advancements in existing products, and geographic expansions to meet the growing consumer demand worldwide.

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

Have a question?

Mrinal

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

- Breg, Inc

- DeRoyal Industries, Inc

- Enovis Corporation

- Bauerfeind AG

- Otto Bock Healthcare GmbH

- Ossur Corporate

- medi GmbH & Co. KG

- Boston Orthotics & Prosthetics

- Essity Health & Medical (BSN medical, Inc)

- ALCARE Co., Ltd

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For