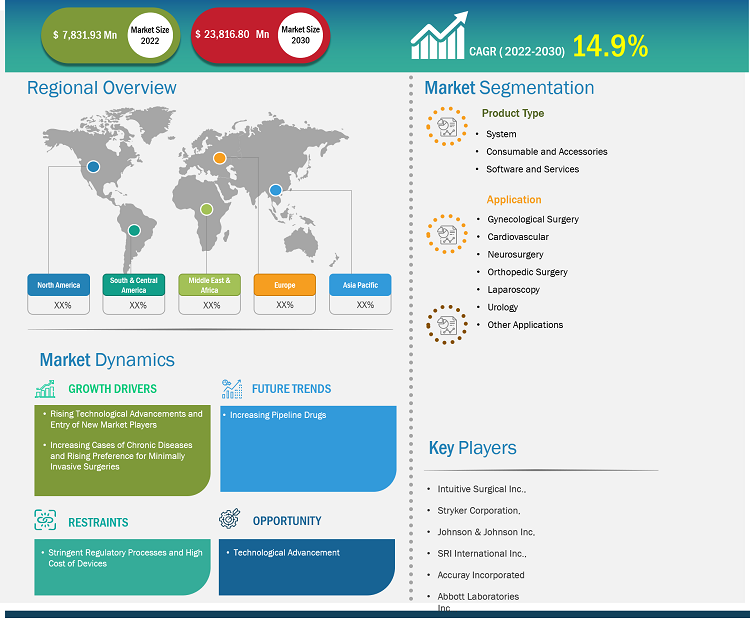

[Research Report] The robotic assisted surgery systems market size is projected to grow from US$ 7,831.93 million in 2022 to US$ 23,816.80 million by 2030; the market is anticipated to record a CAGR of 14.9% from 2022 to 2030.

Market Insights and Analyst View:

The robotic assisted surgery systems market encompasses an array of technologically advanced surgical platforms that integrate robotics, imaging, and navigation systems to assist surgeons in performing minimally invasive procedures with increased precision and control. These systems are designed to enhance surgical capabilities, improve patient outcomes, and minimize the invasiveness of traditional surgical techniques. The noteworthy benefits of robotic assisted surgery systems include enhanced dexterity, three-dimensional visualization, and tremor filtration, allowing surgeons to perform complex procedures with superior accuracy and maneuverability. These systems often enable them to access difficult-to-reach anatomical areas, leading to reduced trauma and faster patient recovery times. Additionally, the integration of robotics in surgeries minimizes the risk of complications and lowers the need for blood transfusions, ultimately contributing to improved post-operative outcomes.

Growth Drivers and Challenges:

The increasing number of research studies exploring the benefits and capabilities of robotically assisted operations is anticipated to fuel market progress in the coming years. In September 2022, a team from the Graduate School of Medical Sciences, Nagoya City University (NCU), conducted a study comparing robotic-assisted, fluoroscopic-guided, ultrasound-guided renal access for percutaneous nephrolithotomy. The study's findings demonstrate the safety and ease of use of revolutionary robotic devices, which may lessen the training burden on surgeons and enable more hospitals to perform PCNL procedures. This method, which uses robotics driven by artificial intelligence, may open a door to the automation of comparable surgical interventions, in turn, speeding up the process and lowering the risk of complications.

A rise in chronic disease cases and the growing popularity of minimally invasive surgeries further favor the robotic assisted surgical systems market. According to news released by The Hindu in August 2022, Apollo Health City in Hyderabad, India, has completed more than 500 robotically assisted gynecological procedures. In November 2022, India Medtronic Private Limited, a wholly-owned subsidiary of Medtronic plc, and Venkateshwar Hospital in Delhi announced the completion of the first urological treatment in north India with the Hugo robotic assisted surgery (RAS) system.

On the other hand, the high cost of robotic surgical systems hampers the financial viability and operational sustainability of healthcare providers. While these systems offer advantages such as enhanced precision, minimal invasiveness, and reduced patient recovery times, the substantial upfront investment and ongoing maintenance costs necessitate careful financial planning and resource allocation for healthcare facilities. Additionally, the need for specialized training and certification of surgical personnel to operate these systems adds further operational costs, impacting the overall affordability and practicality of integrating robotic surgery into existing clinical practices. The cost burden associated with robotic surgical systems has the potential to influence healthcare reimbursement models and coverage decisions. Reimbursement rates for procedures performed with robotic assistance may vary, and coverage by insurance providers could affect the economic rationale for adopting these technologies. This creates a complex landscape where healthcare facilities need to weigh the clinical advantages of robotic surgery against the financial implications, potentially affecting the pace and scale of adoption across different healthcare systems.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Robotic Assisted Surgery Systems Market: Strategic Insights

Market Size Value in US$ 7,831.93 million in 2022 Market Size Value by US$ 23,816.80 million by 2030 Growth rate CAGR of 14.9% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Robotic Assisted Surgery Systems Market: Strategic Insights

| Market Size Value in | US$ 7,831.93 million in 2022 |

| Market Size Value by | US$ 23,816.80 million by 2030 |

| Growth rate | CAGR of 14.9% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Report Segmentation and Scope:

The robotic assisted surgery systems market is segmented on the basis of product type, application, and end user. Based on product type, the market is divided into systems, instruments and accessories, and services. By application, the robotic assisted surgery systems market is segmented into gynecological surgery, cardiovascular, neurosurgery, orthopedic surgery, laparoscopy, urology, general surgery, and others. The market, based on end user, is classified into hospitals, ambulatory surgery centers, and other end users. In terms of geography, the robotic assisted surgery systems market is divided into North America (US, Canada, and Mexico), Europe (UK, Germany, France, Italy, Spain, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, and Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, South Africa, and Rest of Middle East & Africa), and South & Central America (Brazil, Argentina, and Rest of South & Central America).

Segmental Analysis:

Based on product type, the surgical robot segment held a substantial revenue share of the robotic assisted surgery systems market in 2022. The need for surgical robots to perform precise and accurate procedures is predicted to increase due to the surging global incidence of cardiovascular and cancer disorders. The US is expected to report 1.9 million new cancer cases in 2023, according to the American Cancer Society's Cancer Statistics 2023. As per the Australian Institute of Health and Welfare's (AIHW) 2021 report, the estimated new cases of cancer in Australia in 2021 were 150,800. The March 2022 report from the Australian Bureau of Statistics states that 4.0% of Australians, or 1.0 million people, were estimated to have heart disease in 2021.

Based on application, the robot-assisted surgical systems market is classified into gynecological surgery, cardiovascular, neurosurgery, orthopedic surgery, laparoscopy, urology, general surgery, and others. The neurology sector is expected to record the fastest CAGR during 2022–2030. The increasing usage of surgical robots in general surgeries and the benefits they offer over conventional surgical methods benefit the overall market. Furthermore, improvements in technology and the successful results of robotic neurosurgery are anticipated to propel the expansion of the robot-assisted surgical systems market in the coming years. According to SS Innovations Interventional Inc., approximately 1.6 million robotic surgeries were performed globally in 2020.

By end user, the robot-assisted surgical systems market is segmented into hospitals, ambulatory surgical centers, and other end users. The hospital segment dominated the market in 2022 and is anticipated to register a high CAGR during 2022–2030. The growth of the market for hospitals segment is ascribed to rising healthcare costs across several economies. Hospitals provide superior quality of care by utilizing the latest robotic assisted surgical equipment. Moreover, physicians and surgeons prefer robot-assisted systems. The use of robot-assisted operations in overall surgical procedures surged multifold from 1.8% in 2013 to 15.1% in 2019, according to a paper published in the JAMA network.

Regional Analysis:

Based on geography, the robotic assisted surgery systems market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. North America is the most significant contributor to the growth of this market. The market progress in this region is attributed to the growing use of automated surgical instruments and the adoption of next-generation healthcare systems in the US. Furthermore, the lack of surgeons and medical professionals in the US compared to the patient population is projected to benefit the market for robot-assisted surgical systems. The increased prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disease propels the demand for robot-assisted surgical systems in the US.

The growing popularity of minimally invasive procedures as opposed to conventional operations favors the robotic assisted surgery systems market. In December 2022, Hugo extended the clinical trials of its robotic assisted surgery (RAS) systems in the US by enrolling their first patient, according to Medtronic plc. Further, in 2022,a doctor at Duke University Hospital in Durham, North Carolina, carried out the robotic assisted prostatectomy procedure.

The Asia Pacific robotic assisted surgical systems market is expected to grow at the fastest CAGR during 2022–2030 owing to the growing patient population and rising use of sophisticated automated surgical instruments. Additionally, expanding contemporary healthcare facilities and increasing public awareness of the advantages of cutting-edge medical technologies are anticipated to benefit the market growth in this region in the future. Governments of countries in Asia Pacific are making attempts to establish sophisticated healthcare infrastructure, which is drawing international businesses to invest in the establishment of automated instrument development facilities in this region. China holds the largest share of the robot-assisted surgical systems market in Asia Pacific, and India is expected to record the highest CAGR during 2022–2030. Companies in the surgical robotics business in China have shortened their time to market by taking advantage of a special approval pathway that expedites regulatory approval for innovative medical products. Moreover, an increasingly large number of medtech firms specializing in surgical robotics are emerging in the country. In recent years, JianJia Robots and Hurwa entered the Chinese market to develop surgical robotics solutions alongside TINAVI, a domestic company specializing in orthopedic surgical robots. Beijing reimburses TINAVI robot-assisted surgeries for the spine, hip, and knee.

Robotic Assisted Surgery Systems Market Report Scope

Industry Developments and Future Opportunities:

Various initiatives taken by key players operating in the global robotic assisted surgery systems market are listed below:

- In October 2023, Johnson & Johnson MedTech, an orthopedics business of DePuy Synthes, introduced the VELYS Robotic Assisted Solution. The solution has been used in total knee replacement procedures in Germany, Belgium, and Switzerland. With this launch, DePuy Synthes expands the networked technologies within its Digital Surgery Platform to meet unmet demands for orthopedic robots

- In November 2022, an Indian Medtech business partnered with Avra Medical Robotics, an American company listed on the Nasdaq. The first surgical robot to be entirely "Made in India," SSI Mantra, was introduced by SS Innovations. It is a highly developed surgical robotic system with more capabilities and applications than other systems on the market.

- In November 2022, FDA in the United States approved Accelus's software update for the Remi Robotic Navigation System, which allows surgeons performing lumbar spine fixation to place pedicle screws with robotic assistance. Accelus is a private medical technology company that focuses on the adoption of minimally invasive surgery (MIS) as the standard of care in the spine.

Competitive Landscape and Key Companies:

Intuitive Surgical Inc., Stryker Corporation, Johnson & Johnson Inc., SRI International Inc., Accuray Incorporated, Renishaw PLC, Medtronic PLC, Brainlab, Smith & Nephew PLC, Globus Medical, and Zimmer Biomet are among the prominent players in the robotic assisted surgery systems market. These companies focus on expanding their offerings to meet the growing consumer demand worldwide. Their global presence allows them to serve a large set of customers, subsequently allowing them to expand their market share.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Product Type, Application, End User, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

The robotic assisted surgery systems market has major market players, including Intuitive Surgical Inc., Stryker Corporation, Johnson & Johnson Inc., SRI International Inc., Accuray Incorporated, Renishaw PLC, Medtronic PLC, Brainlab, Smith & Nephew PLC, Globus Medical, and Zimmer Biomet.

Based on product type, the surgical robot segment held a substantial revenue share of the robotic assisted surgery systems market in 2022. The need for surgical robots to perform precise and accurate procedures is predicted to increase due to the surging global incidence of cardiovascular and cancer disorders. The US is expected to report 1.9 million new cancer cases in 2023, according to the American Cancer Society's Cancer Statistics 2023. As per the Australian Institute of Health and Welfare's (AIHW) 2021 report, the estimated new cases of cancer in Australia in 2021 were 150,800. The March 2022 report from the Australian Bureau of Statistics states that 4.0% of Australians, or 1.0 million people, were estimated to have heart disease in 2021.

Growing preference for robotically assisted treatments, rising inclination toward minimally invasive surgeries, and the increasing number of product launches are the key factors driving the robotic assisted surgery systems market progress. However, the stringent regulatory processes and high cost of devices hinder the robotic assisted surgery systems market growth.

The robotic assisted surgery systems market was valued at US$ 7,831.93 million in 2022.

The robotic assisted surgery systems market is expected to be valued at US$ 23,816.80 million in 2030.

The robotic assisted surgery systems market encompasses an array of technologically advanced surgical platforms that integrate robotics, imaging, and navigation systems to assist surgeons in performing minimally invasive procedures with increased precision and control. These systems are designed to enhance surgical capabilities, improve patient outcomes, and minimize the invasiveness of traditional surgical techniques.

Based on application, the robot-assisted surgical systems market is classified into gynecological surgery, cardiovascular, neurosurgery, orthopedic surgery, laparoscopy, urology, general surgery, and others. The neurology sector is expected to record the fastest CAGR during 2022–2030. The increasing usage of surgical robots in general surgeries and the benefits they offer over conventional surgical methods benefit the overall market. Furthermore, improvements in technology and the successful results of robotic neurosurgery are anticipated to propel the expansion of the robot-assisted surgical systems market in the coming years. According to SS Innovations Interventional Inc., approximately 1.6 million robotic surgeries were performed globally in 2020.

1. Introduction

1.1 Scope of the Study

1.2 Market Definition, Assumptions and Limitations

1.3 Market Segmentation

2. Executive Summary

2.1 Key Insights

2.2 Market Attractiveness Analysis

3. Research Methodology

4. Robotic Assisted Surgery Systems Market Landscape

4.1 Overview

4.2 PEST Analysis

4.3 Ecosystem Analysis

4.3.1 List of Vendors in the Value Chain

5. Robotic Assisted Surgery Systems Market - Key Market Dynamics

5.1 Key Market Drivers

5.2 Key Market Restraints

5.3 Key Market Opportunities

5.4 Future Trends

5.5 Impact Analysis of Drivers and Restraints

6. Robotic Assisted Surgery Systems Market - Global Market Analysis

6.1 Robotic Assisted Surgery Systems - Global Market Overview

6.2 Robotic Assisted Surgery Systems - Global Market and Forecast to 2030

7. Robotic Assisted Surgery Systems Market – Revenue Analysis (USD Million) – By Product Type, 2020-2030

7.1 Overview

7.2 System

7.3 Consumable and Accessories

7.4 Software and Services

8. Robotic Assisted Surgery Systems Market – Revenue Analysis (USD Million) – By Application, 2020-2030

8.1 Overview

8.2 Gynecological Surgery

8.3 Cardiovascular

8.4 Neurosurgery

8.5 Orthopedic Surgery

8.6 Laparoscopy

8.7 Urology

8.8 Other Applications

9. Robotic Assisted Surgery Systems Market – Revenue Analysis (USD Million) – By End User, 2020-2030

9.1 Overview

9.2 Hospitals

9.3 Ambulatory Surgery Centers

9.4 Other End Users

10. Robotic Assisted Surgery Systems Market - Revenue Analysis (USD Million), 2020-2030 – Geographical Analysis

10.1 North America

10.1.1 North America Robotic Assisted Surgery Systems Market Overview

10.1.2 North America Robotic Assisted Surgery Systems Market Revenue and Forecasts to 2030

10.1.3 North America Robotic Assisted Surgery Systems Market Revenue and Forecasts and Analysis - By Product Type

10.1.4 North America Robotic Assisted Surgery Systems Market Revenue and Forecasts and Analysis - By Application

10.1.5 North America Robotic Assisted Surgery Systems Market Revenue and Forecasts and Analysis - By End User

10.1.6 North America Robotic Assisted Surgery Systems Market Revenue and Forecasts and Analysis - By Countries

10.1.6.1 United States Robotic Assisted Surgery Systems Market

10.1.6.1.1 United States Robotic Assisted Surgery Systems Market, by Product Type

10.1.6.1.2 United States Robotic Assisted Surgery Systems Market, by Application

10.1.6.1.3 United States Robotic Assisted Surgery Systems Market, by End User

10.1.6.2 Canada Robotic Assisted Surgery Systems Market

10.1.6.2.1 Canada Robotic Assisted Surgery Systems Market, by Product Type

10.1.6.2.2 Canada Robotic Assisted Surgery Systems Market, by Application

10.1.6.2.3 Canada Robotic Assisted Surgery Systems Market, by End User

10.1.6.3 Mexico Robotic Assisted Surgery Systems Market

10.1.6.3.1 Mexico Robotic Assisted Surgery Systems Market, by Product Type

10.1.6.3.2 Mexico Robotic Assisted Surgery Systems Market, by Application

10.1.6.3.3 Mexico Robotic Assisted Surgery Systems Market, by End User

Note - Similar analysis would be provided for below mentioned regions/countries

10.2 Europe

10.2.1 Germany

10.2.2 France

10.2.3 Italy

10.2.4 Spain

10.2.5 United Kingdom

10.2.6 Rest of Europe

10.3 Asia-Pacific

10.3.1 Australia

10.3.2 China

10.3.3 India

10.3.4 Japan

10.3.5 South Korea

10.3.6 Rest of Asia-Pacific

10.4 Middle East and Africa

10.4.1 South Africa

10.4.2 Saudi Arabia

10.4.3 U.A.E

10.4.4 Rest of Middle East and Africa

10.5 South and Central America

10.5.1 Brazil

10.5.2 Argentina

10.5.3 Rest of South and Central America

11. Pre and Post Covid-19 Impact

12. Industry Landscape

12.1 Mergers and Acquisitions

12.2 Agreements, Collaborations, Joint Ventures

12.3 New Product Launches

12.4 Expansions and Other Strategic Developments

13. Competitive Landscape

13.1 Heat Map Analysis by Key Players

13.2 Company Positioning and Concentration

14. Robotic Assisted Surgery Systems Market - Key Company Profiles

14.1 Intuitive Surgical Inc.

14.1.1 Key Facts

14.1.2 Business Description

14.1.3 Products and Services

14.1.4 Financial Overview

14.1.5 SWOT Analysis

14.1.6 Key Developments

Note - Similar information would be provided for below list of companies

14.2 Stryker Corporation

14.3 Johnson and Johnson Inc.

14.4 SRI International Inc.

14.5 Accuray Incorporated

14.6 Renishaw PLC

14.7 Medtronic PLC

14.8 Smith and Nephew PLC

14.9 Brainlab

14.10 Globus Medical

15. Appendix

15.1 Glossary

15.2 About The Insight Partners

15.3 Market Intelligence Cloud

The List of Companies - Robotic Assisted Surgery Systems Market

- Intuitive Surgical Inc.

- Stryker Corporation

- Johnson & Johnson Inc.

- SRI International Inc.

- Accuray Incorporated

- Renishaw PLC

- Medtronic PLC

- Brainlab

- Smith & Nephew PLC

- Globus Medical

- Zimmer Biomet

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For