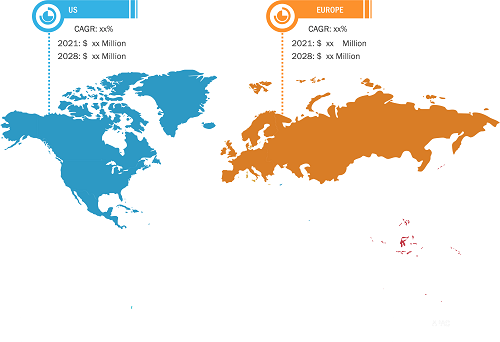

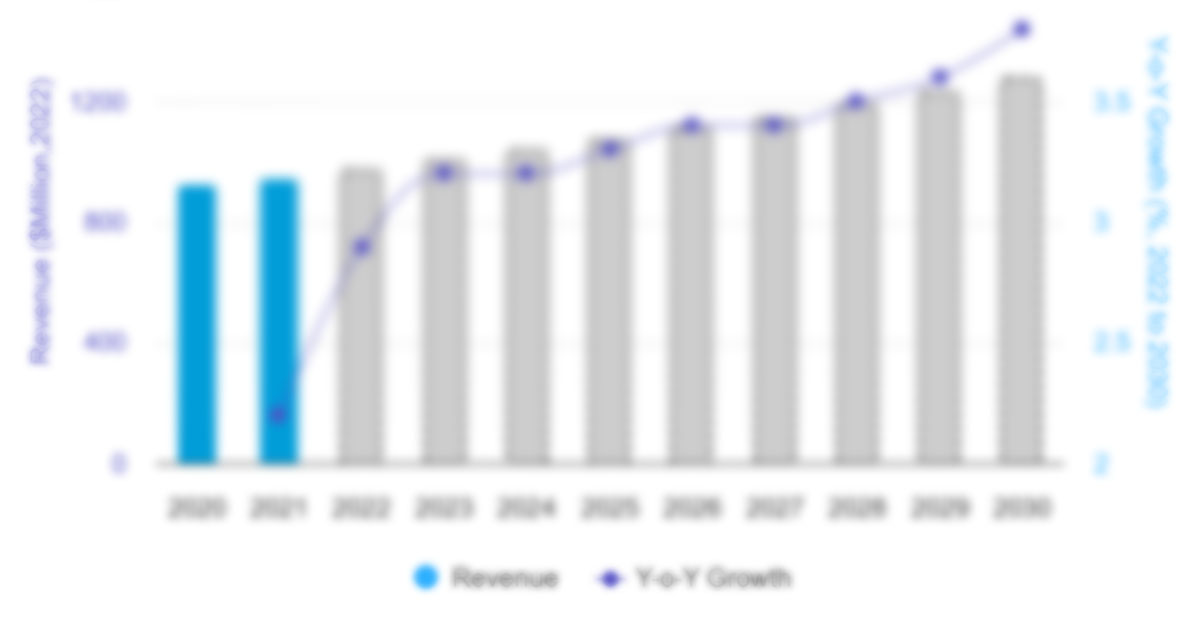

The US and Europe smart hospital beds market is expected to grow from US$ 405.20 million in 2022 to US$ 859.45 million by 2028; it is expected to grow at a CAGR of 13.4% from 2022 to 2028.

Increasing investments in healthcare infrastructure, rising advantages of smart beds, and the growing geriatric population are a few factors driving the US and Europe smart hospital beds market growth.

Automation has led to a reduced dependency on human workforces in many industries. Adopting technically advanced products has impacted ~90% of the work performed daily by individuals. Technological advancements have abundantly benefitted the healthcare sector, and numerous hi-tech medical devices with embedded control functions are now available for the efficient operation of this sector. Smart beds indicate technological progress in the healthcare sector. These beds have become an integral part of hospitals, nursing care facilities, specialized clinics, and home care.

Smart hospital beds are equipped with all necessary specifications that enable efficient operations of healthcare providers or caregivers. They enable faster recovery of patients by making the necessary movements hassle-free. These beds are also equipped with monitoring systems that can be used to send alerts to nurses. Companies also offer smart beds with communication systems that connect directly to nursing departments. Communications allow nurses to remotely monitor patients' medical conditions and vital functions. In addition, smart beds are now combined with remote sensors, further contributing to better infrastructures. Other advantages of modern smart beds include their ability to identify patients’ health patterns, keep healthcare providers well-informed, and assist them in decision-making related to health and intervention.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

US and Europe Smart Hospital Beds Market: Strategic Insights

Market Size Value in US$ 405.20 million in 2022 Market Size Value by US$ 859.45 million by 2028 Growth rate CAGR of 13.4% from 2022 to 2028 Forecast Period 2022 to 2028 Base Year 2022

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

US and Europe Smart Hospital Beds Market: Strategic Insights

| Market Size Value in | US$ 405.20 million in 2022 |

| Market Size Value by | US$ 859.45 million by 2028 |

| Growth rate | CAGR of 13.4% from 2022 to 2028 |

| Forecast Period | 2022 to 2028 |

| Base Year | 2022 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

A few other features of smart hospital beds include height adjustment features, smart side rails, and wireless connections. The transformation of normal hospital beds to highly networked devices that use software solutions is categorized as Class II medical devices. With further upgrades in smart bed technologies, these beds are anticipated to deliver research information on different medical and health aspects, perform statistical analysis, and collect patient data. These potential abilities of smart hospital beds encourage significant investments in the modernization of healthcare infrastructure, leading to the growing demand for smart hospital beds.

According to estimates provided by the Organization for Economic Cooperation and Development (OECD) in 2021, OECD member countries have increased the overall healthcare expenditure from 3% in 2018 to 8% by 2030. For instance, European Union (EU) launched EU4Health Programme with an investment of US$ 5 billion (€5.3 billion), focusing on reinforcing health data collected from patients, digital tools and services, and digital transformation of healthcare. The UK has plans to invest US$ 1.6 billion (£2 billion) in the digital transformation of the National Health Services (NHS). Such investments are likely to enhance the installation of smart hospital beds in the healthcare sectors in European countries.

Lucrative Regions for US and Europe Smart Hospital Beds Market

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

Application Segment Insight

Based on application, the smart hospital beds market is segmented into less than product and fall prevention, pressure injury prevention, patient deterioration and monitoring, and others. The fall prevention segment held the largest market share in 2022, and the others segment is anticipated to register the highest CAGR during the forecast period. Patients fall prevention in hospitals is an important part of a patient safety plan. Also, patient falls are among the leading cause of morbidity and mortality in hospitals and healthcare systems, accounting for at least 30% of occurrences resulting in severe injuries to the patient. The CareView company article reveals that hospital falls have increased costs by ~US$ 14,000 per patient stay on average. Also, the average fall costs about US$ 8,000 in diagnostic testing. Therefore, companies are designing smart hospital beds with five main features: low height beds, bed-exit detection systems, bed event data and history logs, staff communication, and a clear view of surroundings. The Centrella smart beds incorporated at the University Hospital involve technology to reinforce patient safety measures and make it convenient for nurses. The new smart bed offers a variety of safety features, such as a motion-activated night light, and is connected to the hospital's call system for alerts to be intimate directly in the nurse's smartphone. Such technological advancement and innovative smart hospital bed designs ultimately influence the fall prevention segment growth, thereby dominating the smart hospital beds market growth.

A rise in the prevalence of chronic diseases such as diabetes, cancer, etc.; lifestyle diseases such as obesity; rapid growth of the geriatric population; longer hospital stay after necessary surgery procedure; technological advancements in smart hospital beds; and favorable reimbursement policies are a few factors expected to fuel the growth of the smart hospital beds market in the US.

In addition, patients suffering from chronic diseases such as diabetes, cancer, cardiovascular disease, immune deficiencies, multiple sclerosis, and rheumatoid arthritis need long-term monitoring and treatment. This leads to regular hospital visits, and in the condition of multiple chronic diseases, the patient is required to stay in the hospital for a longer period of time. Smart beds are expected to benefit patients and improve health systems by delivering research information on medical and health status, statistical analysis, and data collection. Collecting data on patients increases efficiency and accurate diagnostics for healthcare providers and medical professionals while paving the way to reduce the number of hospital readmissions. Smart beds can create a network of connected devices, mechanical and digital gear, or people with unique identifiers and the ability to send data rapidly. Also, the market players are introducing advanced technology in smart hospital beds; for example, in October 2020, Stryker introduced the ProCuity smart bed, a completely wireless hospital bed with many smart patient monitoring capabilities. Stryker's Secure Connect technology, which offers a wireless connection to nurse call systems, has been incorporated into ProCuity.

US and Europe Smart Hospital Beds Market, by Product Type – 2022 and 2028

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

- Sample PDF showcases the content structure and the nature of the information with qualitative and quantitative analysis.

- Request discounts available for Start-Ups & Universities

Companies operating in the smart hospital beds market adopt the product innovation strategy to meet the evolving customer demands worldwide, permitting them to maintain their brand name in the global market.

Smart Hospital Beds Market – Segmentation

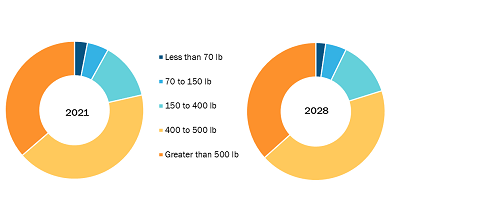

Based on patient weight, the smart hospital beds market is segmented into less than 70 lb, 70 to 150 lb, 150 to 400 lb, 400 to 500 lb, and greater than 500 lb. Based on offerings, the smart hospital beds market is segmented into products & accessories, software & solution, and services. Based on application, the market is categorized into fall prevention, pressure injury prevention, patient deterioration and monitoring, and others. Based on smart hospital beds end user, the market is segmented into hospitals, clinics & nursing home, ambulatory surgical centers, medical laboratories, long-term care centers, and others. Based on region, the market is primarily bifurcated into the US and Europe. The market in Europe is further segmented into Germany, the UK, France, Italy, Spain, and the Rest of Europe.

A few of the leading companies operating in the US and Europe smart hospital beds market are Hill-Rom Holdings, Inc.; Stryker; Arjo; Invacare Corporation; PARAMOUNT BED CO., LTD.; GF Health Products, Inc.; Malvestio Spa; Span America; Savion Industries; and Stiegelmeyer GmbH & Co. KG.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Patient Weight, Offering, Application, and End User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

The CAGR value of the smart hospital beds market during the forecasted period of 2022-2028 is 13.4%.

400 to 500 lb segment held the largest share of the market in the US and Europe smart hospital beds market and held the largest market share in 2022.

Key factors that are driving the growth of this market are increasing investments in healthcare infrastructure and advantages of smart beds growing geriatric population to boost the market growth for the smart hospital beds over the years.

Smart hospital beds are integrated solutions for supporting and monitoring patient care based on a multidisciplinary design approach. Smart hospital beds support patients that enables the doctors to deliver a thorough checkup and administer treatment and other medical facilities. Along with technological developments, hospital beds are also converted to watch a patient’s resting movement. A smart hospital bed is well-furnished with the most advanced technology for patient care.

The fall prevention segment dominated the US and Europe smart hospital beds market and held the largest market share in 2022.

The smart hospital beds market majorly consists of the players such Hill-Rom Holdings, Incc, Stryker, Arjo, Invacare Corporation, PARAMOUNT BED CO., LTD., GF Health Products, Inc., Malvestio Spa, Span America, Savion Industries, Stiegelmeyer GmbH & Co. KG, and Other Market Participants .

Hill Rom Holdings, Inc. and Stryker are the top two companies that hold huge market shares in the US and Europe smart hospital beds market.

The US and Europe smart hospital beds market is segmented by region into US, Europe region overall and information by separate countries such as the UK, Germany, France, Italy, Spain, and Rest of Europe. The US held the largest market share of the smart hospital beds market in 2022.

1. Introduction

1.1 Scope of the Study

1.2 The Insight Partners Research Report Guidance

1.3 Market Segmentation

1.3.1 Smart Hospital Beds Market – by Patient Weight

1.3.2 Smart Hospital Beds Market – by Offering

1.3.3 Smart Hospital Beds Market – by Application

1.3.4 Smart Hospital Beds Market – by End User

1.3.5 Smart Hospital Beds Market – by Geography

2. Smart Hospital Beds Market – Key Takeaways

3. Research Methodology

3.1 Coverage

3.2 Secondary Research

3.3 Primary Research

4. Smart Hospitals Beds Market – Market Landscape

4.1 Overview

4.2 PEST Analysis

4.2.1 US PEST Analysis

4.2.2 Europe PEST Analysis

4.3 Expert’s Opinion

5. Smart Hospital Beds Market – Key Market Dynamics

5.1 Market Drivers

5.1.1 Increasing Investments in Healthcare Infrastructure and Advantages of Smart Beds

5.1.2 Growing Geriatric Population

5.1.3 Developments in Healthcare Infrastructures and Growth Strategies by Smart Hospital Bed Providers

5.2 Market Restraints

5.2.1 Cybersecurity Risks and Recalls Associated with Smart Hospital Beds

5.3 Market Opportunities

5.3.1 Robotic Hospital Beds

5.4 Future Trends

5.4.1 Digitalization in Healthcare Systems

5.5 Impact Analysis

6. Smart Hospital Beds Market – Regional Analysis

6.1 Smart Hospital Beds Market

6.1.1 Smart Hospital Beds Market Revenue Forecast and Analysis

6.1.2 Smart Hospital Beds Market Revenue Forecast and Analysis, By Region

6.1.3 Market Positioning of Key Players

6.2 Bariatric Hospital Beds Market

6.2.1 Bariatric Hospital Beds Market Revenue Forecast and Analysis

6.2.2 Bariatric Hospital Beds Market Revenue Forecast and Analysis, By Region

6.2.3 US+Europe: Bariatric Hospital Beds Market

6.2.4 US: Bariatric Hospital Beds Market

6.2.5 Europe: Bariatric Hospital Beds Market

6.2.5.1 UK: Bariatric Hospital Beds Market

6.2.5.2 Germany: Bariatric Hospital Beds Market

6.2.5.3 France: Bariatric Hospital Beds Market

6.2.5.4 Italy: Bariatric Hospital Beds Market

6.2.5.5 Spain: Bariatric Hospital Beds Market

6.2.5.6 Rest of Europe Bariatric Hospital Beds Market

6.3 US+Europe Hospital Beds Market

6.3.1 Hospital Beds Market Revenue Forecast and Analysis

6.3.2 Hospital Beds Market Revenue Forecast and Analysis, By Region

6.3.3 US Hospital Beds Market

6.3.4 Europe Hospital Beds Market

6.3.4.1 Germany: Hospital Bed Market

6.3.4.2 UK: Hospital Bed Market

6.3.4.3 France: Hospital Bed Market

6.3.4.4 Italy: Hospital Bed Market

6.3.4.5 Spain: Hospital Bed Market

6.3.4.6 Rest of Europe: Hospital Bed Market

7. Smart Hospital Beds Market – Revenue and Forecast to 2028 – By Patient Weight

7.1 Overview

7.2 Smart Hospital Beds Market Revenue Share, by Patient Weight (2021 and 2028)

7.3 Less than 70 lb

7.3.1 Overview

7.3.2 Less than 70 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

7.4 to 150 lb

7.4.1 Overview

7.4.2 to 150 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

7.5 to 400 lb

7.5.1 Overview

7.5.2 to 400 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

7.6 to 500 lb

7.6.1 Overview

7.6.2 to 500 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

7.7 Greater than 500 lb

7.7.1 Overview

7.7.2 Greater than 500 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

8. Smart Hospital Beds Market – Revenue and Forecast to 2028 – By Offering

8.1 Overview

8.2 Smart Hospital Beds Market Revenue Share, by Offering (2021 and 2028)

8.3 Products and Accessories

8.3.1 Overview

8.3.2 Products and Accessories: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

8.4 Software and Solutions

8.4.1 Overview

8.4.2 Software and Solutions: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

8.5 Services

8.5.1 Overview

8.5.2 Services: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

9. Smart Hospital Beds Market – Revenue and Forecast to 2028 – By Application

9.1 Overview

9.2 Smart Hospital Beds Market Revenue Share, by Application (2021 and 2028)

9.3 Fall Prevention

9.3.1 Overview

9.3.2 Fall Prevention: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

9.4 Pressure Injury Prevention

9.4.1 Overview

9.4.2 Pressure Injury Prevention: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

9.5 Patient Deterioration and Monitoring

9.5.1 Overview

9.5.2 Patient Deterioration and Monitoring: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

9.6 Others

9.6.1 Overview

9.6.2 Others: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10. Smart Hospital Beds Market – Revenue and Forecast to 2028 – By End User

10.1 Overview

10.2 Smart Hospital Beds Market Revenue Share, by End User (2021 and 2028)

10.3 Hospitals

10.3.1 Overview

10.3.2 Hospitals: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10.4 Clinics and Nursing Homes

10.4.1 Overview

10.4.2 Clinics and Nursing Homes: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10.5 Ambulatory Surgical Centers

10.5.1 Overview

10.5.2 Ambulatory Surgical Centers: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10.6 Medical Laboratories

10.6.1 Overview

10.6.2 Medical Laboratories: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10.7 Long Term Care Centers

10.7.1 Overview

10.7.2 Long Term Care Centers: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

10.8 Others

10.8.1 Overview

10.8.2 Others: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11. Smart Hospital Beds Market – Revenue and Forecast to 2028 – Regional Analysis

11.1 US: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.1.1 Overview

11.1.2 US: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.1.3 US: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.1.4 US: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.1.5 US: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.1.6 US: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2 Europe: Smart Hospital Beds Market

11.2.1 Overview

11.2.2 Europe: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.3 Europe: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.4 Europe: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.5 Europe: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.6 Europe: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7 Europe: Smart Hospital Beds Market, by Country, 2022 & 2028 (%)

11.2.7.1 UK: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.1.1 Overview

11.2.7.1.2 UK: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.1.3 UK: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.1.4 UK: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.1.5 UK: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.1.6 UK: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7.2 Germany: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.2.1 Overview

11.2.7.2.2 Germany: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.2.3 Germany: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.2.4 Germany: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.2.5 Germany: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.2.6 Germany: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7.3 France: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.3.1 Overview

11.2.7.3.2 France: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.3.3 France: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.3.4 France: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.3.5 France: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.3.6 France: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7.4 Italy: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.4.1 Overview

11.2.7.4.2 Italy: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.4.3 Italy: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.4.4 Italy: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.4.5 Italy: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.4.6 Italy: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7.5 Spain: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.5.1 Overview

11.2.7.5.2 Spain: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.5.3 Spain: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.5.4 Spain: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.5.5 Spain: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.5.6 Spain: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

11.2.7.6 Rest of Europe: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.6.1 Overview

11.2.7.6.2 Rest of Europe: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

11.2.7.6.3 Rest of Europe: Smart Hospital Beds Market, by Patient Weight, 2019-2028 (US$ Million)

11.2.7.6.4 Rest of Europe: Smart Hospital Beds Market, by Offering, 2019-2028 (US$ Million)

11.2.7.6.5 Rest of Europe: Smart Hospital Beds Market, by Application, 2019-2028 (US$ Million)

11.2.7.6.6 Rest of Europe: Smart Hospital Beds Market, by End User, 2019-2028 (US$ Million)

12. Impact Of COVID-19 Pandemic on Smart Hospital Beds Market

12.1 US: Impact Assessment of COVID-19 Pandemic

12.2 Europe: Impact Assessment of COVID-19 Pandemic

13. Smart Hospital Beds Market–Industry Landscape

13.1 Overview

13.2 Growth Strategies in the Smart Hospital Beds Market

13.3 Inorganic Growth Strategies

13.3.1 Overview

13.4 Organic Growth Strategies

13.4.1 Overview

14. Company Profiles

14.1 Hill-Rom Holdings Inc

14.1.1 Key Facts

14.1.2 Business Description

14.1.3 Products and Services

14.1.4 Financial Overview

14.1.5 SWOT Analysis

14.1.6 Key Developments

14.2 Stryker Corp

14.2.1 Key Facts

14.2.2 Business Description

14.2.3 Products and Services

14.2.4 Financial Overview

14.2.5 SWOT Analysis

14.2.6 Key Developments

14.3 DewertOkin GmbH

14.3.1 Key Facts

14.3.2 Business Description

14.3.3 Products and Services

14.3.4 Financial Overview

14.3.5 SWOT Analysis

14.3.6 Key Developments

14.4 Arjo AB

14.4.1 Key Facts

14.4.2 Business Description

14.4.3 Products and Services

14.4.4 Financial Overview

14.4.5 SWOT Analysis

14.4.6 Key Developments

14.5 Medline Industries Inc

14.5.1 Key Facts

14.5.2 Business Description

14.5.3 Products and Services

14.5.4 Financial Overview

14.5.5 SWOT Analysis

14.5.6 Key Developments

14.6 Invacare Corp

14.6.1 Key Facts

14.6.2 Business Description

14.6.3 Products and Services

14.6.4 Financial Overview

14.6.5 SWOT Analysis

14.6.6 Key Developments

14.7 Paramount Bed Co Ltd

14.7.1 Key Facts

14.7.2 Business Description

14.7.3 Products and Services

14.7.4 Financial Overview

14.7.5 SWOT Analysis

14.7.6 Key Developments

14.8 Zhangjiagang Braun Industry Co Ltd

14.8.1 Key Facts

14.8.2 Business Description

14.8.3 Products and Services

14.8.4 Financial Overview

14.8.5 SWOT Analysis

14.8.6 Key Developments

14.9 GF Health Products Inc

14.9.1 Key Facts

14.9.2 Business Description

14.9.3 Products and Services

14.9.4 Financial Overview

14.9.5 SWOT Analysis

14.9.6 Key Developments

14.10 Enigma Care Ltd

14.10.1 Key Facts

14.10.2 Business Description

14.10.3 Products and Services

14.10.4 Financial Overview

14.10.5 SWOT Analysis

14.10.6 Key Developments

14.11 Malvestio SpA

14.11.1 Key Facts

14.11.2 Business Description

14.11.3 Products and Services

14.11.4 Financial Overview

14.11.5 SWOT Analysis

14.11.6 Key Developments

14.12 Besco Medical Ltd

14.12.1 Key Facts

14.12.2 Business Description

14.12.3 Products and Services

14.12.4 Financial Overview

14.12.5 SWOT Analysis

14.12.6 Key Developments

14.13 Span-America Medical Systems Inc

14.13.1 Key Facts

14.13.2 Business Description

14.13.3 Products and Services

14.13.4 Financial Overview

14.13.5 SWOT Analysis

14.13.6 Key Developments

14.14 Nuprom Health Projects Co

14.14.1 Key Facts

14.14.2 Business Description

14.14.3 Products and Services

14.14.4 Financial Overview

14.14.5 SWOT Analysis

14.14.6 Key Developments

14.15 Savion Industries Ltd

14.15.1 Key Facts

14.15.2 Business Description

14.15.3 Products and Services

14.15.4 Financial Overview

14.15.5 SWOT Analysis

14.15.6 Key Developments

14.16 Stiegelmeyer GmbH & Co. KG

14.16.1 Key Facts

14.16.2 Business Description

14.16.3 Products and Services

14.16.4 Financial Overview

14.16.5 SWOT Analysis

14.16.6 Key Developments

14.17 Favero Health Projects SpA

14.17.1 Key Facts

14.17.2 Business Description

14.17.3 Products and Services

14.17.4 Financial Overview

14.17.5 SWOT Analysis

14.17.6 Key Developments

14.18 Joerns Healthcare LLC

14.18.1 Key Facts

14.18.2 Business Description

14.18.3 Products and Services

14.18.4 Financial Overview

14.18.5 SWOT Analysis

14.18.6 Key Developments

14.19 PROMA REHA Sro

14.19.1 Key Facts

14.19.2 Business Description

14.19.3 Products and Services

14.19.4 Financial Overview

14.19.5 SWOT Analysis

14.19.6 Key Developments

14.20 Volker GmbH

14.20.1 Key Facts

14.20.2 Business Description

14.20.3 Products and Services

14.20.4 Financial Overview

14.20.5 SWOT Analysis

14.20.6 Key Developments

14.21 Hopefull Medical Equipment Co Ltd

14.21.1 Key Facts

14.21.2 Business Description

14.21.3 Products and Services

14.21.4 Financial Overview

14.21.5 SWOT Analysis

14.21.6 Key Developments

14.22 LINET spol sro

14.22.1 Key Facts

14.22.2 Business Description

14.22.3 Products and Services

14.22.4 Financial Overview

14.22.5 SWOT Analysis

14.22.6 Key Developments

14.23 Wissner-Bosserhoff GmbH

14.23.1 Key Facts

14.23.2 Business Description

14.23.3 Products and Services

14.23.4 Financial Overview

14.23.5 SWOT Analysis

14.23.6 Key Developments

14.24 Umano Medical Inc

14.24.1 Key Facts

14.24.2 Business Description

14.24.3 Products and Services

14.24.4 Financial Overview

14.24.5 SWOT Analysis

14.24.6 Key Developments

14.25 Guangdong Pigeon Medical Apparatus Co Ltd

14.25.1 Key Facts

14.25.2 Business Description

14.25.3 Products and Services

14.25.4 Financial Overview

14.25.5 SWOT Analysis

14.25.6 Key Developments

14.26 Transfer Master Products Inc

14.26.1 Key Facts

14.26.2 Business Description

14.26.3 Products and Services

14.26.4 Financial Overview

14.26.5 SWOT Analysis

14.26.6 Key Developments

14.27 Famed Zywiec Sp zoo

14.27.1 Key Facts

14.27.2 Business Description

14.27.3 Products and Services

14.27.4 Financial Overview

14.27.5 SWOT Analysis

14.27.6 Key Developments

14.28 Haelvoet NV

14.28.1 Key Facts

14.28.2 Business Description

14.28.3 Products and Services

14.28.4 Financial Overview

14.28.5 SWOT Analysis

14.28.6 Key Developments

14.29 Jiangsu Saikang Medical Equipment Co Ltd

14.29.1 Key Facts

14.29.2 Business Description

14.29.3 Products and Services

14.29.4 Financial Overview

14.29.5 SWOT Analysis

14.29.6 Key Developments

14.30 Noa Medical Industries Inc

14.30.1 Key Facts

14.30.2 Business Description

14.30.3 Products and Services

14.30.4 Financial Overview

14.30.5 SWOT Analysis

14.30.6 Key Developments

14.31 Medstrom Ltd

14.31.1 Key Facts

14.31.2 Business Description

14.31.3 Products and Services

14.31.4 Financial Overview

14.31.5 SWOT Analysis

14.31.6 Key Developments

14.32 Midmark India Pvt Ltd

14.32.1 Key Facts

14.32.2 Business Description

14.32.3 Products and Services

14.32.4 Financial Overview

14.32.5 SWOT Analysis

14.32.6 Key Developments

14.33 JD Healthcare Group Pty Ltd

14.33.1 Key Facts

14.33.2 Business Description

14.33.3 Products and Services

14.33.4 Financial Overview

14.33.5 SWOT Analysis

14.33.6 Key Developments

14.34 Antano Group SRL

14.34.1 Key Facts

14.34.2 Business Description

14.34.3 Products and Services

14.34.4 Financial Overview

14.34.5 SWOT Analysis

14.34.6 Key Developments

14.35 MESPA

14.35.1 Key Facts

14.35.2 Business Description

14.35.3 Products and Services

14.35.4 Financial Overview

14.35.5 SWOT Analysis

14.35.6 Key Developments

14.36 Merits Health Products Co Ltd

14.36.1 Key Facts

14.36.2 Business Description

14.36.3 Products and Services

14.36.4 Financial Overview

14.36.5 SWOT Analysis

14.36.6 Key Developments

14.37 Magnatek Enterprises Pvt Ltd

14.37.1 Key Facts

14.37.2 Business Description

14.37.3 Products and Services

14.37.4 Financial Overview

14.37.5 SWOT Analysis

14.37.6 Key Developments

14.38 Benmor Medical Ltd

14.38.1 Key Facts

14.38.2 Business Description

14.38.3 Products and Services

14.38.4 Financial Overview

14.38.5 SWOT Analysis

14.38.6 Key Developments

14.39 Malsch GmbH

14.39.1 Key Facts

14.39.2 Business Description

14.39.3 Products and Services

14.39.4 Financial Overview

14.39.5 SWOT Analysis

14.39.6 Key Developments

14.40 Thuasne SAS

14.40.1 Key Facts

14.40.2 Business Description

14.40.3 Products and Services

14.40.4 Financial Overview

14.40.5 SWOT Analysis

14.40.6 Key Developments

14.41 Drive Devilbiss Healthcare Ltd

14.41.1 Key Facts

14.41.2 Business Description

14.41.3 Products and Services

14.41.4 Financial Overview

14.41.5 SWOT Analysis

14.41.6 Key Developments

14.42 Medi-Plinth Equipment Ltd

14.42.1 Key Facts

14.42.2 Business Description

14.42.3 Products and Services

14.42.4 Financial Overview

14.42.5 SWOT Analysis

14.42.6 Key Developments

15. Appendix

15.1 About The Insight Partners

15.2 Glossary of Terms

LIST OF TABLES

Table 1. US+Europe Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 2. US+Europe Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 3. US Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 4. US Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 5. Europe Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 6. Europe Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 7. UK Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 8. UK Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 9. Germany Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 10. Germany Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 11. France Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 12. France Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 13. Italy Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 14. Italy Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 15. Spain Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 16. Spain Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 17. Rest of Europe Bariatric Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 18. Rest of Europe Bariatric Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 19. US Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 20. US Hospital Bed Market, by Usage– Revenue and Forecast to 2028 (US$ Million)

Table 21. US Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 22. US Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 23. Europe: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 24. Europe: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 25. Europe: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 26. Europe: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 27. Germany: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 28. Germany: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 29. Germany: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 30. Germany: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 31. UK: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 32. UK: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 33. UK: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 34. UK: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 35. France: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 36. France: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 37. France: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 38. France: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 39. Italy: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 40. Italy: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 41. Italy: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 42. Italy: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 43. Spain: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 44. Spain: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 45. Spain: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 46. Spain: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 47. Rest of Europe: Hospital Bed Market, by Type – Revenue and Forecast to 2028 (US$ Million)

Table 48. Rest of Europe: Hospital Bed Market, by Usage – Revenue and Forecast to 2028 (US$ Million)

Table 49. Rest of Europe: Hospital Bed Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 50. Rest of Europe: Hospital Bed Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 51. US Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 52. US Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 53. US Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 54. US Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 55. Europe Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 56. Europe Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 57. Europe Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 58. Europe Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 59. UK Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 60. UK Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 61. UK Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 62. UK Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 63. Germany Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 64. Germany Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 65. Germany Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 66. Germany Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 67. France Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 68. France Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 69. France Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 70. France Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 71. Italy Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 72. Italy Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 73. Italy Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 74. Italy Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 75. Spain Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 76. Spain Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 77. Spain Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 78. Spain Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 79. Rest of Europe Smart Hospital Beds Market, by Patient Weight – Revenue and Forecast to 2028 (US$ Million)

Table 80. Rest of Europe Smart Hospital Beds Market, by Offering – Revenue and Forecast to 2028 (US$ Million)

Table 81. Rest of Europe Smart Hospital Beds Market, by Application – Revenue and Forecast to 2028 (US$ Million)

Table 82. Rest of Europe Smart Hospital Beds Market, by End User – Revenue and Forecast to 2028 (US$ Million)

Table 83. Recent Inorganic Growth Strategies in The Smart Hospital Beds Market

Table 84. Recent Organic Growth Strategies in The Smart Hospital Beds Market

Table 85. Glossary of Terms

LIST OF FIGURES

Figure 1. Smart Hospital Beds Market Segmentation

Figure 2. Smart Hospital Beds by Region

Figure 3. Smart Hospital Beds Market Overview

Figure 4. to 500 lb Segment Held Largest Share of Patient Weight Segment in Smart Hospital Beds Market

Figure 5. Smart Hospital Beds Market, by Geography (US$ Million)

Figure 6. Smart Hospital Beds Market – Leading Country Markets (US$ Million)

Figure 7. Smart Hospital Beds Market – Industry Landscape

Figure 8. US: PEST Analysis

Figure 9. Europe: PEST Analysis

Figure 10. Experts’ Opinion

Figure 11. Smart Hospital Beds Market Impact Analysis of Drivers and Restraints

Figure 12. Smart Hospital Beds Market – Revenue Forecast and Analysis – 2020–2028

Figure 13. Smart Hospital Beds Market, by Geography – Forecast and Analysis (2022–2028)

Figure 14. Market Positioning of Key Players

Figure 15. Bariatric Hospital Beds Market – Revenue Forecast and Analysis – 2020–2028

Figure 16. Hospital Beds Market – Revenue Forecast and Analysis – 2020–2028

Figure 17. Smart Hospital Beds Market Revenue Share, by Patient Weight (2021 and 2028)

Figure 18. Less than 70 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 19. to 150 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 20. to 400 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 21. to 500 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 22. Greater than 500 lb: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 23. Smart Hospital Beds Market Revenue Share, by Offering (2021 and 2028)

Figure 24. Products and Accessories: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 25. Software and Solutions: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 26. Services: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 27. Smart Hospital Beds Market Revenue Share, by Application (2021 and 2028)

Figure 28. Products and Accessories: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 29. Pressure Injury Prevention: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 30. Patient Deterioration and Monitoring: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 31. Others: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 32. Smart Hospital Beds Market Revenue Share, by End User (2021 and 2028)

Figure 33. Hospitals: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 34. Clinics and Nursing Homes: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 35. Ambulatory Surgical Centers: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 36. Medical Laboratories: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 37. Long Term Care Centers: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 38. Others: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 39. US: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 40. Europe: Smart Hospital Beds Market, by Key Country – Revenue (2021) (US$ Million)

Figure 41. Europe Smart Hospital Beds Market Revenue and Forecast to 2028 (US$ Million)

Figure 42. Europe: Smart Hospital Beds Market, by Country, 2022 & 2028 (%)

Figure 43. UK: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 44. Germany: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 45. France: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 46. Italy: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 47. Spain: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 48. Rest of Europe: Smart Hospital Beds Market – Revenue and Forecast to 2028 (US$ Million)

Figure 49. Impact of the COVID-19 Pandemic on the US Market

Figure 50. Impact of COVID-19 Pandemic on European Country Markets

Figure 51. Growth Strategies in the Smart Hospital Beds Market

The List of Companies - US and Europe Smart Hospital Beds Market

- Hill-Rom Holdings, Inc.

- Stryker

- Arjo

- Invacare Corporation

- PARAMOUNT BED CO., LTD.

- GF Health Products, Inc.

- Malvestio Spa

- Span America

- Savion Industries

- Stiegelmeyer GmbH & Co. KG

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For