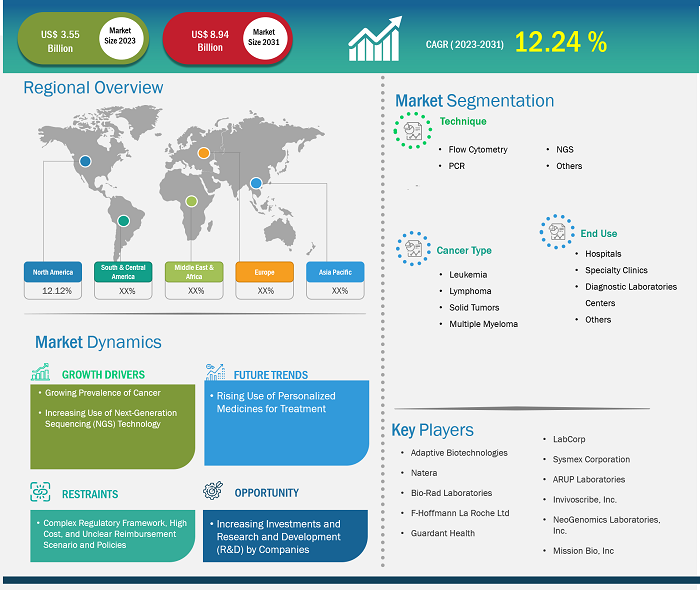

The minimal residue disease testing market size is projected to surge from US$ 3.55 billion in 2023 to US$ 8.94 billion by 2031; the market is estimated to record a CAGR of 12.24% during 2023–2031.

Analyst Perspective:

The report includes growth prospects owing to the current minimal residue disease testing market trends and their foreseeable impact during the forecast period. The increasing global prevalence of various cancers, such as leukemia, lymphoma, and solid tumors, and the demand for minimal residue disease testing products and services. Healthcare providers and researchers recognize the clinical utility of minimal residue disease assessment in monitoring treatment response, predicting relapse, and guiding therapeutic interventions. As minimal residue disease testing continues to evolve and emerge as a critical tool in cancer management, market players focus on innovation, standardization, and accessibility to capitalize on the lucrative opportunities in the minimal residue disease testing market.

Market Overview:

The inclusion of minimal residual disease testing in health coverage plans and the application of this testing approach in solid tumor diagnosis are the factors driving the minimal residual disease testing market. The demand for minimal residual disease testing has also increased with the surge in consumer awareness worldwide. Healthcare providers and researchers recognize this trend and strive to meet patient expectations by integrating minimal residual disease testing into clinical practice. Other key factors driving the minimal residue disease testing market growth include the rising prevalence of cancer and the increasing use of next-generation sequencing technology.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Minimal Residue Disease Testing Market: Strategic Insights

Market Size Value in US$ 3.55 billion in 2023 Market Size Value by US$ 8.94 billion by 2031 Growth rate CAGR of 12.24% from 2023 to 2031 Forecast Period 2023-2031 Base Year 2023

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Minimal Residue Disease Testing Market: Strategic Insights

| Market Size Value in | US$ 3.55 billion in 2023 |

| Market Size Value by | US$ 8.94 billion by 2031 |

| Growth rate | CAGR of 12.24% from 2023 to 2031 |

| Forecast Period | 2023-2031 |

| Base Year | 2023 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Market Driver:

Growing Prevalence of Cancer Propels Market Growth

In 2020, the number of cancer cases reached 19.3 million, and the number of cancer-related deaths reached 9.96 million. As per the International Agency for Research on Cancer, the count of cancer cases is expected to reach 21.9 million by 2025 and 24.6 million by 2030. According to the February 2021 report by the American Society of Clinical Oncology, ~235,760 adults (119,100 men and 116,6600 women) in the US were diagnosed with lung cancer. GLOBOCAN 2020 data that India accounted for 18.3% of the total new cancer cases recorded in the world; moreover, cervical cancer accounts for 9.4% of all cancer cases. According to the American Cancer Society (ACS), nearly 26,560 new cases of stomach cancer were discovered in the US in 2021, 16,160 men and 10,400 women. Statistics released by the National Breast Cancer Foundation in July 2021, ~63% of breast cancer patients were diagnosed with local-stage breast cancer, 27% were diagnosed with regional-stage breast cancer, and 6% were diagnosed with distant (metastatic) disease. In addition, the increasing prevalence of blood cancer worldwide bolsters the demand for better treatment options and accuracy in removing residual cancer cells. As per the statistics published by the American Cancer Society, an estimated 34,920 new cases of multiple myeloma were diagnosed in the US in January 2022. Such an upsurge in the number of cancer cases is likely to compel governments to launch new cancer prevention programs, which is expected to drive the minimal residue disease testing market growth.

Segmental Analysis:

The minimal residue disease testing market analysis has been carried out by considering the following segments: technique, cancer type, and end use.

Based on technique, the minimal residue disease testing market is segmented into flow cytometry, PCR, NGS, and others. The flow cytometry segment held the largest market share in 2023. The PCR segment is estimated to register the highest CAGR of 12.39% during 2023–2031. The PCR method can detect cancer cells based on characteristic genetic abnormalities such as mutations or chromosomal changes. The technique necessarily involves the amplification of tiny DNA or RNA fragments to aid their detectability and countability. This allows identifying genetic abnormalities even by using samples (such as blood cells or bone marrow) containing a scarce number of cancer cells. The high sensitivity of PCR allows it to detect as low as one cancer cell out of 100,000 normal cells. Obtaining test results can take 5–14 days.

The market, based on cancer type, is divided into leukemia, lymphoma, solid tumors, and multiple myeloma. The solid tumors segment held the largest minimal residue disease testing market share in 2023. The market growth for this segment is attributed to ongoing research studies focused on evaluating patients with solid tumors. There are no accepted recommendations for employing MRD testing for the detection of non-hematologic malignancies. The approach involving circulating tumor DNA (ctDNA) as a prognostic biomarker for residual molecular disease diagnosis following solid tumor therapy is rapidly being incorporated into clinical trial design and translational research investigations. This approach is suitable for use in standard clinical care. Although ctDNA detection technologies have evolved rapidly, the low sensitivity of these detection methods reduces their usefulness in the detection of MRD in various clinical applications.

Based on end user, the minimal residue disease testing market is divided into hospitals, specialty clinics, diagnostic laboratories, and others. The hospitals segment held the largest minimal residue disease testing market share in 2022, and the same is anticipated to register the highest CAGR of 12.79% during 2023–2031. Hospitals hold a significant share of the market, which can be primarily attributed to their role in acute care and patient management. Hospital admissions are often necessary for patients suffering severe health conditions, as hospital facilities enable better decision-making capabilities, allowing doctors and healthcare professionals to analyze patients and offer them better treatment options.

Regional Analysis:

The scope of the minimal residue disease testing market report includes North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. The market in North America was valued at US$ 0.93 billion in 2023 and is projected to reach US$ 2.34 billion by 2031; it is expected to register a CAGR of 12.12% during 2023–2031. Significant increase in cancer incidence; the introduction of the latest technologies; and the established proteomics, genomics, and oncology research infrastructure solidify North America's position as a major contributor to the minimal residue disease testing market.

The Asia Pacific minimal residue disease testing market is expected to record the fastest CAGR of 12.68%. The region, especially with countries such as India and China, is home to a sizable pharmaceutical industry. In October 2021, Genetron Health (China) and Jiangsu Fosun (China) began commercializing MRD detection tests in China. They have also promoted Seq-MRD in hematology-focused hospitals and clinics in China in the past. This test offers accuracy, high throughput, cost-effectiveness, consistency, and fast turnaround times. Research is perceived as a primary focus area by major market players to develop novel tests. In addition to the increased focus on research, the surging need for monitoring cancer patients post-treatment continues to drive the minimal residue disease testing market progress in Asia Pacific. Additionally, improvements in healthcare infrastructure and the emerging pharmaceutical sector make Asia Pacific a key hub for the significant growth and development of the market.

Key Player Analysis:

Adaptive Biotechnologies; Natera; Bio-Rad Laboratories; F-Hoffmann La Roche Ltd; Guardant Health; LabCorp; Sysmex Corporation; ARUP Laboratories; Invivoscribe, Inc.; NeoGenomics Laboratories, Inc.; and Mission Bio, Inc are among the key players profiled in the minimal residue disease testing market report.

Minimal Residue Disease Testing Market Report Scope

Recent Developments:

Companies operating in the minimal residue disease testing market adopt mergers and acquisitions as key growth strategies. As per company press releases, a few recent market developments are listed below:

- In April 2023, Quest Diagnostics acquired Haystack Oncology to expand its oncology portfolio with the inclusion of advanced liquid biopsy technology. This addition allowed Quest to improve personalized cancer treatment by providing tools and other products with highly sensitive diagnostic capabilities.

- In April 2023, Integrated DNA Technologies launched the Archer FUSIONPlex Core Solid Tumor Panel. This breakthrough testing solution has been improved and refined to cover a broader range of single nucleotide variants (SNVs) and indel (i.e., insertion, deletion, or insertion and deletion of nucleotides) capabilities or aid cancer research.

- In December 2022, Adaptive Biotechnologies launched clonoSEQ for assessing minimal residual disease using circulating tumor DNA (ctDNA) in patients that have diffuse large B-cell lymphoma (DLBCL).

- In October 2022, Adaptive Biotechnologies and Epic Systems Corporation partnered for the integration of the clonoSEQ assay into Epic's comprehensive electronic medical record (EMR) system. The clonoSEQ assay was monitored and approved by the US Food and Drug Administration (FDA) to detect minimal residual disease associated with multiple myeloma (MM), chronic lymphocytic leukemia (CLL), and B-cell acute lymphoblastic leukemia (ALL).

- In August 2022, Roche launched its first Digital LightCycler System, which is designed to accurately quantify trace quantities of specific RNA and DNA.

- In February 2022, Personalis collaborated with Moores Cancer Center to support clinical diagnostic testing in patients with advanced solid tumors and hematologic malignancies. The collaboration focused on conducting studies for the detection of highly sensitive minimal residual disease and cancer recurrence using a newly introduced liquid biopsy assay.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Technique, Cancer Type, End Use, and Geography

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

The global minimal residual disease testing market, based on technique is divided into flow cytometry, PCR, NGS, and others. The flow cytometry segment held the largest market share in 2023, and the PCR segment is likely to register the highest CAGR of 12.39% during 2023–2031. Based on cancer type, the market is segmented into leukemia, lymphoma, solid tumors, and multiple myeloma. The solid tumors segment held the largest market share in 2023, and the same segment is estimated to grow at the fastest CAGR during 2023–2031. The lymphoma segment held the second largest market share in 2023. Based on end user, the market is segmented into hospitals, specialty clinics, diagnostic laboratories, and others. The hospitals segment held the largest minimal residue disease testing market share in 2022, and the same is anticipated to register the highest CAGR of 12.79% during 2023–2031.

The minimal residual disease testing market is expected to be valued at US$ 8.94 billion in 2031.

The minimal residual disease testing market was valued at US$ 3.55 billion in 2023.

The minimal residual disease testing market majorly consists of the players such as Adaptive Biotechnologies; Natera; Bio-Rad Laboratories; F-Hoffmann La Roche Ltd; Guardant Health; LabCorp; Sysmex Corporation; ARUP Laboratories; Invivoscribe, Inc.; NeoGenomics Laboratories, Inc.; and Mission Bio, Inc.

The factors driving the growth of the minimal residual disease testing market include the surging prevalence of cancer and the increasing use of next-generation sequencing technology.

Patients achieving complete hematologic remission after blood cancer treatment may foster residual cancer cells in the bone marrow or peripheral blood. These cells can result in relapse, as they persist at levels so low that they cannot be detected by conventional cytomorphology. Similar is the case with several other cancer conditions, including solid tumors and multiple myeloma. Minimal residual disease testing is employed to detect and quantify cancer cells existing in small numbers in a patient's body. This testing is performed by using sensitive technologies such as polymerase chain reaction (PCR), next-generation sequencing (NGS), and flow cytometry to identify measurable residual disease at the molecular level. Minimal residual disease testing is clinically important because it helps monitor response to treatment, predicts risk of relapse, guides personalized therapies, and serves as an endpoint in clinical trials.

1. Introduction

1.1 Scope of the Study

1.2 Market Definition, Assumptions and Limitations

1.3 Market Segmentation

2. Executive Summary

2.1 Key Insights

2.2 Market Attractiveness Analysis

3. Research Methodology

4. Minimal Residue Disease Testing Market Landscape

4.1 Overview

4.2 PEST Analysis

4.3 Ecosystem Analysis

4.3.1 List of Vendors in the Value Chain

5. Minimal Residue Disease Testing Market - Key Market Dynamics

5.1 Key Market Drivers

5.2 Key Market Restraints

5.3 Key Market Opportunities

5.4 Future Trends

5.5 Impact Analysis of Drivers and Restraints

6. Minimal Residue Disease Testing Market - Global Market Analysis

6.1 Minimal Residue Disease Testing - Global Market Overview

6.2 Minimal Residue Disease Testing - Global Market and Forecast to 2031

7. Minimal Residue Disease Testing Market – Revenue Analysis (USD Million) – By Technique, 2021-2031

7.1 Overview

7.2 Flow Cytometry

7.3 Polymerase Chain Reaction (PCR)

7.4 Next Generation Sequencing (NGS)

7.5 Others

8. Minimal Residue Disease Testing Market – Revenue Analysis (USD Million) – By Cancer Type, 2021-2031

8.1 Overview

8.2 Leukemia

8.2.1 Myeloid Leukemia

8.2.2 Lymphoid Leukemia

8.3 Lymphoma

8.3.1 Hodgkin's Lymphoma

8.3.2 Non- Hodgkin's Lymphoma

8.4 Solid Tumors

8.5 Multiple Myeloma

9. Minimal Residue Disease Testing Market – Revenue Analysis (USD Million) – By End User, 2021-2031

9.1 Overview

9.2 Hospitals

9.3 Specialty Clinics

9.4 Diagnostic Laboratories

9.5 Others

10. Minimal Residue Disease Testing Market - Revenue Analysis (USD Million), 2021-2031 – Geographical Analysis

10.1 North America

10.1.1 North America Minimal Residue Disease Testing Market Overview

10.1.2 North America Minimal Residue Disease Testing Market Revenue and Forecasts to 2031

10.1.3 North America Minimal Residue Disease Testing Market Revenue and Forecasts and Analysis - By Technique

10.1.4 North America Minimal Residue Disease Testing Market Revenue and Forecasts and Analysis - By Cancer Type

10.1.5 North America Minimal Residue Disease Testing Market Revenue and Forecasts and Analysis - By End User

10.1.6 North America Minimal Residue Disease Testing Market Revenue and Forecasts and Analysis - By Countries

10.1.6.1 United States Minimal Residue Disease Testing Market

10.1.6.1.1 United States Minimal Residue Disease Testing Market, by Technique

10.1.6.1.2 United States Minimal Residue Disease Testing Market, by Cancer Type

10.1.6.1.3 United States Minimal Residue Disease Testing Market, by End User

10.1.6.2 Canada Minimal Residue Disease Testing Market

10.1.6.2.1 Canada Minimal Residue Disease Testing Market, by Technique

10.1.6.2.2 Canada Minimal Residue Disease Testing Market, by Cancer Type

10.1.6.2.3 Canada Minimal Residue Disease Testing Market, by End User

10.1.6.3 Mexico Minimal Residue Disease Testing Market

10.1.6.3.1 Mexico Minimal Residue Disease Testing Market, by Technique

10.1.6.3.2 Mexico Minimal Residue Disease Testing Market, by Cancer Type

10.1.6.3.3 Mexico Minimal Residue Disease Testing Market, by End User

Note - Similar analysis would be provided for below mentioned regions/countries

10.2 Europe

10.2.1 Germany

10.2.2 France

10.2.3 Italy

10.2.4 Spain

10.2.5 United Kingdom

10.2.6 Rest of Europe

10.3 Asia-Pacific

10.3.1 Australia

10.3.2 China

10.3.3 India

10.3.4 Japan

10.3.5 South Korea

10.3.6 Rest of Asia Pacific

10.4 Middle East and Africa

10.4.1 South Africa

10.4.2 Saudi Arabia

10.4.3 U.A.E

10.4.4 Rest of Middle East and Africa

10.5 South and Central America

10.5.1 Brazil

10.5.2 Argentina

10.5.3 Chile

11. Industry Landscape

11.1 Mergers and Acquisitions

11.2 Agreements, Collaborations, Joint Ventures

11.3 New Product Launches

11.4 Expansions and Other Strategic Developments

12. Competitive Landscape

12.1 Heat Map Analysis by Key Players

12.2 Company Positioning and Concentration

13. Minimal Residue Disease Testing Market - Key Company Profiles

13.1 Adaptive Biotechnologies

13.1.1 Key Facts

13.1.2 Business Description

13.1.3 Products and Services

13.1.4 Financial Overview

13.1.5 SWOT Analysis

13.1.6 Key Developments

Note - Similar information would be provided for below list of companies

13.2 NeoGenomics Laboratories, Inc.

13.3 ARUP Laboratories

13.4 Bio-Rad Laboratories

13.5 F Hoffmann La Roche Ltd

13.6 Guardant Health Inc

13.7 Invivoscribe Inc

13.8 Laboratory Corporation of America Holdings

13.9 Sysmex Corporation

13.10 Natera

13.11 Mission Bio, Inc.

14. Appendix

14.1 Glossary

14.2 About The Insight Partners

14.3 Market Intelligence Cloud

The List of Companies - Minimal Residual Disease Testing Market

- Adaptive Biotechnologies

- Natera

- Bio-Rad Laboratories

- F-Hoffmann La Roche Ltd

- Guardant Health

- LabCorp

- Sysmex Corporation

- ARUP Laboratories

- Invivoscribe, Inc.

- NeoGenomics Laboratories, Inc.

- Mission Bio, Inc.

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Minimal Residue Disease Testing Market

Apr 2024

Pediatric Cardiology Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Transcatheter Heart Valves, Occlusion Devices, Catheters, Stents, Introducer Sheaths, and Others), Disease Indication (Congenital Heart Disease, Acquired Heart Disease, Arrhythmias, Cardiomyopathies, and Others), Surgical Procedure (Interventional Procedures, Heart Rhythm Management Procedures, and Others), End User (Hospitals, Specialty Clinics, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Apr 2024

Pharmaceutical Membrane Filters Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technology (Microfiltration, Ultrafiltration, Reverse Osmosis and Nanofiltration), Design (Hollow Fiber, Spiral Wound, Tubular System and Plate and Frame), Material (Polyethersulfone (PES), Polysulfone (PS), Cellulose-Based Membranes, Polytetrafluoroethylene (PTFE), Polyvinyl Chloride (PVC), Polyacrylonitrile (PAN) and Others), End User (Pharmaceutical and Biotech Industries and CROs and CDMOs), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South & Central America)

Apr 2024

ECG Devices Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Resting ECG and Stress ECG), Lead Type (12-Lead ECG, 3–6 Lead ECG, and Single Lead), Technology [Portable (Wired) ECG System and Wireless ECG System], End User (Hospital and Clinics, Ambulatory Surgical Centers, Cardiac Centers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Apr 2024

Surgical Laser Fiber Units Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (CO2 Laser, Diode Laser, Erbium Laser, Nd:YAG Laser, Holmium Laser, Alexandrite Laser, and Others), Material (Silica-Based Fibers, Quartz Fibers, Polymer-Based Fibers, Multimode Fibers, and Others), Power (Low-Power Lasers, Medium-Power Lasers, and High-Power Lasers), Application (Urology, Dermatology, Gynecology, Cardiology, Neurology, Ophthalmology, Respiratory, Dentistry and Others), Wavelength (9,301 nm and above, 2,941–9,300 nm, and 1,441–2,940 nm, 821–1,440 nm, 710–820 nm, and below 710 nm), End User (Hospitals, Specialty Clinics, Physician Office, and Others), and Geography

Apr 2024

Therapeutic Vaccines Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Cancer Vaccines, Infectious Disease Vaccines, and Others), Technology (Allogenic Vaccines and Autologous Vaccines), End User (Hospitals, Clinics, and Others), and Geography

Apr 2024

Medical Cables Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Disposable Medical Cables, Reusable Medical Cables, and Custom Medical Cables), Applications [Diagnostics (Ultrasound Cables, Endoscopy Cables, Patient Interface Cables, and Others), Motorized Equipment, Patient Monitoring (ECG Cables, SpO2 Cables, NiBP Cables, EEG Cables, and Others), Surgical and Life Support (Fiber Optics, Modular Local Area Network, and Others), and Others], End User (Hospital and Clinics, Diagnostic Laboratories and Imaging Centers, Ambulatory Surgical Centers, and Others), and Geography

Apr 2024

Laser-Assisted ENT Surgeries Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (C02 Laser, Nd:YAG Laser, Diode Laser, Blue Laser, KTP Laser, Argon Laser, and Other Laser Types), Surgery Type [Laser Laryngeal Surgery, Laser Endoscopic Sinus Surgery (LESS), Laser-Assisted Uvulopalatoplasty (LAUP), Laser-Assisted Stapedotomy, Laser-Assisted Tonsillectomy and Adenoidectomy, Laser Turbinates Reduction, Transoral Laser Microsurgery (TLM), Nasal Surgery, and Other Surgery Types], End User (Hospitals and Specialty Clinics, Physician Offices, and Other End Users), and Geography (North America, Europe, Asia Pacific, South and Central America, and Middle East and Africa)

Apr 2024

Mobile Cleanroom Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Softwall and Hardwall), End User (Microelectronics Industry, Pharmaceuticals and Biotechnology Industry, Medical Device Manufacturers, and Others), and Geography

Get Free Sample For

Get Free Sample For