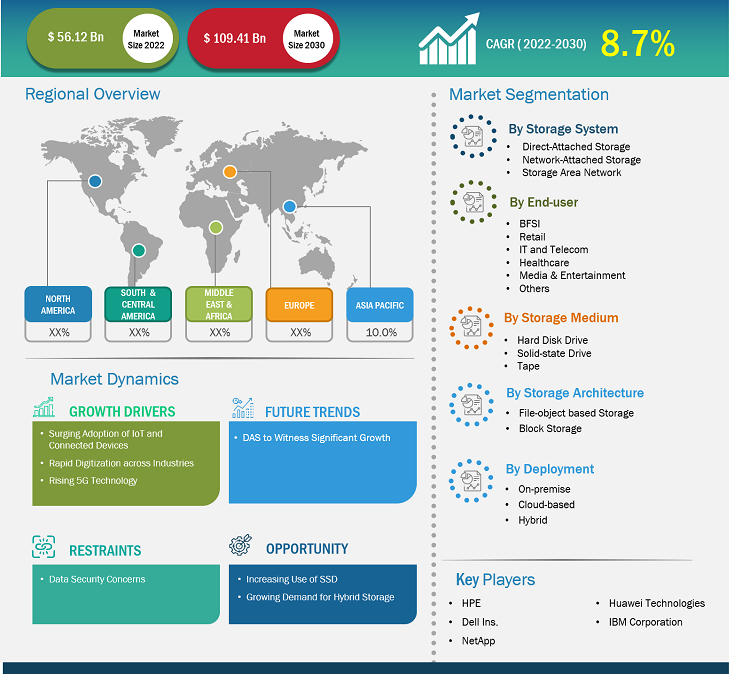

The next-generation data storage market size is projected to reach from US$ 56.12 billion in 2022 to US$ 109.41 billion by 2030; it is estimated to record a CAGR of 8.7% from 2022 to 2030. The increasing resilience of DAS is likely to remain a key trend in the market.

Next Generation Data Storage Market Analysis

The next-generation data storage market in Asia Pacific is experiencing significant growth owing to constant technological advancements, rapid urbanization, and increased investments in research and development by data storage solution providers. One notable development is the launch of the Asia Pacific Data Centre Association (APDCA), which marks the first association of its kind in the region. The APDCA aims to consolidate the shared interests of the data center industry across the Asia Pacific, bringing together data center operators, suppliers, and stakeholders. This association supports advocacies for policies that encourage the sustainable growth of the data center industry. The launch of the APDCA signifies a unified effort to represent the collective interests of the data center industry in Asia Pacific. This association, along with the advancements in technology and the growing market demand, demonstrates the region's commitment to shaping the future of next-generation data storage. The economic development of countries such as Japan and China has also surged the adoption of cutting-edge technologies in enterprises that aim to enhance operational efficiency and maintain competitiveness. Additionally, the presence of a large number of IT industries in the region drives the next-generation data storage market

Next Generation Data Storage Market Overview

5G's significantly faster speeds and lower latency are projected to enable a surge in data generation. The demand for the Internet of Things (IoT) will increase with more smart devices generating real-time data. In addition, with faster downloads and uploads, users will consume and create more data, from 4K/8K video streaming to AR/VR experiences. Also, remote work, cloud applications, and data-driven decision-making will increase enterprise data volumes. This massive data flood necessitates next-gen storage solutions that can handle high volume and velocity with low latency. Efficiently storing and processing real-time data streams requires advanced technologies such as flash storage and in-memory computing.

In November 2023, several companies implemented 5G technologies. For instance, the Port of Tyne, one of the UK's biggest and most important ports, went live with 5G private network connectivity. Together with partners BT and Ericsson, the Port deployed a private network with coverage across the entire estate, making it the UK's first site-wide deployment of 5G standalone connectivity for smart port applications. In addition, in January 2024, Ataya, one of the leaders of unified connectivity for Industry 4.0 and beyond, announced the launch of Chorus, a standalone 5G Access Point (AP) that brings unparalleled simplicity and low-cost benefits to enterprises needing to deploy Private 5G networks rapidly. This will increase the data generation volume. Moreover, partnerships and collaborations between technology giants, telecommunications companies, and storage solution providers will be crucial for driving innovation and delivering integrated solutions. Therefore, 5G technology is acting as a catalyst for the next-generation data storage market, pushing the boundaries of data management and paving the way for faster, more efficient, and scalable storage solutions.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Next Generation Data Storage Market: Strategic Insights

Market Size Value in US$ 56.12 billion in 2022 Market Size Value by US$ 109.41 billion by 2030 Growth rate CAGR of 8.7% from 2022 to 2030 Forecast Period 2022-2030 Base Year 2022

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Next Generation Data Storage Market: Strategic Insights

| Market Size Value in | US$ 56.12 billion in 2022 |

| Market Size Value by | US$ 109.41 billion by 2030 |

| Growth rate | CAGR of 8.7% from 2022 to 2030 |

| Forecast Period | 2022-2030 |

| Base Year | 2022 |

Naveen

Have a question?

Naveen will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Next Generation Data Storage Market Drivers and Opportunities

Rapid Digitization Across Industries to Favor Market

Digitization across industries, from healthcare and finance to retail and manufacturing, is creating an explosion in data generation. This includes everything, including sensor data from connected devices and AI-generated insights. Traditional storage solutions struggle with this volume and require constant upgrades or scaling, making next-gen technologies more attractive. Digitized processes and decision-making rely on real-time data access and analysis. Next-gen technologies, including flash storage, NVMe, and software-defined storage, offer significantly faster performance compared to traditional disk drives, enabling smoother operations and faster insights.

Rapidly evolving business needs have further surged the demand for storage solutions that can easily scale up or down as data volumes and access demands fluctuate. Next-gen solutions such as cloud storage and object storage offer on-demand scalability and flexibility, eliminating the need for upfront infrastructure investments and catering to dynamic workloads. Further, new technologies such as AI, IoT, and machine learning generate unstructured and complex data types that require specialized storage solutions. Next-gen technologies such as data lakes and data fabrics offer specialized tools and frameworks for managing and analyzing these diverse data types, unlocking potential value. Thus, rapid digitization is acting as a powerful catalyst for the next-generation data storage market by creating demand for scalable, performant, and secure solutions that can handle the ever-growing volume and complexity of data.

Growing Demand For Hybrid Data Storage

The demands on modern businesses are greater than ever. Companies need to be innovative, flexible, and efficient in order to stay competitive. Hybrid cloud storage, which combines the benefits of public and private cloud environments, including on-premises data centers or edge locations, has emerged as a crucial technology for promoting growth. An architecture framework for hybrid clouds gives businesses the ability to control where data is stored while also efficiently handling spikes in IT demand. It is anticipated that specialized hybrid cloud solutions designed for particular industries or niche requirements will become more popular. These solutions will meet the needs of businesses operating in highly regulated sectors and address their particular compliance requirements while also building greater trust.

Next Generation Data Storage Market Report Segmentation Analysis

Key segments that contributed to the derivation of the next-generation data storage market analysis are storage system, end user, storage medium, storage architecture, and deployment.

- Based on the storage system, the next-generation data storage market is divided into direct attached storage (DAS), network attached storage (NAS), and storage area network (SAN). The network attached storage (NAS) segment will hold a significant market share in 2022.

- By end user, the market is segmented into BFSI, retail, IT and telecom, healthcare, media and entertainment, and others. The BFSI segment held the largest market share in 2022.

- In terms of storage medium, the market is segmented into hard disk drives, solid-state drives, and tape. The hard disk drive segment held the largest market share in 2022.

- In terms of storage architecture, the market is segmented into file-object-based storage and block storage. The file-object-based storage segment held the largest market share in 2022.

- In terms of deployment, the market is segmented into on-premise, cloud-based, and hybrid. The on-premise segment held the largest market share in 2022.

Next Generation Data Storage Market Share Analysis by Geography

The geographic scope of the next-generation data storage market report is mainly divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The next-generation data storage market in Asia Pacific is experiencing significant growth, propelled by various factors. Firstly, there is a remarkable surge in the number of laptop and smartphone users, accompanied by rising disposable income and increasing consumer awareness. As a result, the region is witnessing strong demand for dependable, secure, and cost-effective storage infrastructure. Secondly, the presence of a substantial number of IT industries in countries such as China, Japan, and India plays an essential role in driving market expansion. Additionally, the adoption of technologies such as big data, IoT, and other digital platforms in economies including China, India, Japan, and South Korea amplifies the need for efficient data storage management solutions. The emergence of data hubs and commercial organizations in Asia Pacific also promotes its dominance in the next-generation data storage market.

Next Generation Data Storage Market Report Scope

Next Generation Data Storage Market News and Recent Developments

The next-generation data storage market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the developments in the next-generation data storage market are listed below:

- DDN, the global leader in artificial intelligence (AI) and multi-cloud data management solutions, announced the launch of DDN Infinia. This next-generation software-defined storage platform leverages two decades of DDN engineering in file systems, data orchestration, and AI-based optimization, all coming together to usher in the era of accelerated computing and generative AI. (Source: DDN, Press Release, November 2023)

- Hitachi, Ltd. announced the transformation of its existing data storage portfolio with the introduction of Hitachi Virtual Storage Platform One, a single hybrid cloud data platform. Having a common data plane across structured and unstructured data in block, file, and object storage allows businesses to run different types of applications anywhere—on-premises and in the public cloud—without any complexities. (Source: Hitachi, Ltd, Press Release, October 2023)

Next Generation Data Storage Market Report Coverage and Deliverables

The “Next Generation Data Storage Market Size and Forecast (2020–2030)” report provides a detailed analysis of the market covering below areas:

- Next-generation data storage market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Next-generation data storage market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Detailed PEST/Porter’s Five Forces and SWOT analysis

- Next-generation data storage market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the next-generation data storage market

- Detailed company profiles

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Storage System, End-User, Storage Medium, Storage Architecture, and Deployment

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

North America is expected to dominate the next-generation data storage market with the highest market share in 2022.

The next-generation data storage market size is projected to reach US$ 109.41 billion by 2030.

The global next-generation data storage market is expected to grow at a CAGR of 8.7% during the forecast period 2022 - 2030.

The leading players operating in the next-generation data storage market are Dell Technologies Inc, Hewlett Packard Enterprise Co, NetApp Inc, Hitachi Ltd, International Business Machines Corp, Pure Storage Inc, DataDirect Networks Inc, Fujitsu Ltd, NETGEAR, and Huawei Technologies Co Ltd.

The increasing resilience of DAS is anticipated to play a significant role in the global next-generation data storage market in the coming years.

Increasing adoption of IoT & connected devices, rapid digitization across industries, and rising 5G technology are the major factors driving the next-generation data storage market.

1. Introduction

1.1 The Insight Partners Research Report Guidance

1.2 Market segmentation

2. Executive Summary

2.1 Key Insights

2.2 Market Attractiveness

3. Research Methodology

3.1 Coverage

3.2 Secondary Research

3.3 Primary Research

4. Next-Generation Data Storage Market Landscape

4.1 Overview

4.2 PEST Analysis

4.3 Ecosystem Analysis

4.3.1 System Providers:

4.3.2 System Integrators

4.3.3 End-Users:

4.3.4 List of Vendors in the Value Chain

5. Next-Generation Data Storage Market – Key Market Dynamics

5.1 Next-Generation Data Storage Market – Key Market Dynamics

5.2 Market Drivers

5.2.1 Surging Adoption of IoT and Connected Devices:

5.2.2 Rapid Digitization across Industries

5.2.3 Rising 5G Technology

5.3 Market Restraints

5.3.1 Data Security Concerns

5.4 Market Opportunities

5.4.1 ncreasing Use of SSD

5.4.2 Growing Demand for Hybrid Storage

5.5 Future Trends

5.5.1 DAS to Witness Significant Growth

5.6 Impact of Drivers and Restraints:

6. Next-Generation Data Storage Market – Global Market Analysis

6.1 Next-Generation Data Storage Market Revenue (US$ Million), 2022–2030

6.2 Next-Generation Data Storage Market Forecast Analysis

7. Next-Generation Data Storage Market Analysis – by Storage System

7.1 Direct Attached Storage (DAS)

7.1.1 Overview

7.1.2 Direct Attached Storage (DAS): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

7.2 Network Attached Storage (NAS)

7.2.1 Overview

7.2.2 Network Attached Storage (NAS): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

7.3 Storage Area Network (SAN)

7.3.1 Overview

7.3.2 Storage Area Network (SAN): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8. Next-Generation Data Storage Market Analysis – by End-user

8.1 BFSI

8.1.1 Overview

8.1.2 BFSI: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8.2 Retail

8.2.1 Overview

8.2.2 Retail: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8.3 IT and telecom

8.3.1 Overview

8.3.2 IT and telecom: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8.4 Healthcare

8.4.1 Overview

8.4.2 Healthcare: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8.5 Media and Entertainment

8.5.1 Overview

8.5.2 Media and Entertainment: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

8.6 Others

8.6.1 Overview

8.6.2 Others: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

9. Next-Generation Data Storage Market Analysis – by Storage Medium

9.1 Hard Disk Drive

9.1.1 Overview

9.1.2 Hard Disk Drive: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

9.2 Solid-State Drive

9.2.1 Overview

9.2.2 Solid-State Drive: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

9.3 Tape

9.3.1 Overview

9.3.2 Tape: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

10. Next-Generation Data Storage Market Analysis – by Storage Architecture

10.1 File-Object based Storage

10.1.1 Overview

10.1.2 File-Object based Storage: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

10.2 Block Storage

10.2.1 Overview

10.2.2 Block Storage: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

11. Next-Generation Data Storage Market Analysis – by Deployment

11.1 On-premise

11.1.1 Overview

11.1.2 On-premise: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

11.2 Cloud-based

11.2.1 Overview

11.2.2 Cloud-based: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

11.3 Hybrid

11.3.1 Overview

11.3.2 Hybrid: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12. Next-Generation Data Storage Market – Geographical Analysis

12.1 Overview

12.2 North America

12.2.1 North America Next-Generation Data Storage Market Overview

12.2.2 North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.2.3 North America: Next-Generation Data Storage Market Breakdown, by Storage System

12.2.3.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage System

12.2.4 North America: Next-Generation Data Storage Market Breakdown, by End-user

12.2.4.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by End-user

12.2.5 North America: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.2.5.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Medium

12.2.6 North America: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.2.6.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Architecture

12.2.7 North America: Next-Generation Data Storage Market Breakdown, by Deployment

12.2.7.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Deployment

12.2.8 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.2.8.1 North America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.2.8.2 United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.2.8.2.1 United States: Next-Generation Data Storage Market Breakdown, by Storage System

12.2.8.2.2 United States: Next-Generation Data Storage Market Breakdown, by End-user

12.2.8.2.3 United States: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.2.8.2.4 United States: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.2.8.2.5 United States: Next-Generation Data Storage Market Breakdown, by Deployment

12.2.8.3 Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.2.8.3.1 Canada: Next-Generation Data Storage Market Breakdown, by Storage System

12.2.8.3.2 Canada: Next-Generation Data Storage Market Breakdown, by End-user

12.2.8.3.3 Canada: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.2.8.3.4 Canada: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.2.8.3.5 Canada: Next-Generation Data Storage Market Breakdown, by Deployment

12.2.8.4 Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.2.8.4.1 Mexico: Next-Generation Data Storage Market Breakdown, by Storage System

12.2.8.4.2 Mexico: Next-Generation Data Storage Market Breakdown, by End-user

12.2.8.4.3 Mexico: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.2.8.4.4 Mexico: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.2.8.4.5 Mexico: Next-Generation Data Storage Market Breakdown, by Deployment

12.3 Europe

12.3.1 Europe Next-Generation Data Storage Market Overview

12.3.2 Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.3 Europe: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.3.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage System

12.3.4 Europe: Next-Generation Data Storage Market Breakdown, by End-user

12.3.4.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by End-user

12.3.5 Europe: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.5.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Medium

12.3.6 Europe: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.6.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Architecture

12.3.7 Europe: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.7.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Deployment

12.3.8 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.3.8.1 Europe: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.3.8.2 Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.2.1 Germany: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.2.2 Germany: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.2.3 Germany: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.2.4 Germany: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.2.5 Germany: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.8.3 United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.3.1 United Kingdom: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.3.2 United Kingdom: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.3.3 United Kingdom: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.3.4 United Kingdom: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.3.5 United Kingdom: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.8.4 France: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.4.1 France: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.4.2 France: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.4.3 France: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.4.4 France: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.4.5 France: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.8.5 Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.5.1 Italy: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.5.2 Italy: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.5.3 Italy: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.5.4 Italy: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.5.5 Italy: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.8.6 Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.6.1 Russian Federation: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.6.2 Russian Federation: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.6.3 Russian Federation: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.6.4 Russian Federation: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.6.5 Russian Federation: Next-Generation Data Storage Market Breakdown, by Deployment

12.3.8.7 Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.3.8.7.1 Rest of Europe: Next-Generation Data Storage Market Breakdown, by Storage System

12.3.8.7.2 Rest of Europe: Next-Generation Data Storage Market Breakdown, by End-user

12.3.8.7.3 Rest of Europe: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.3.8.7.4 Rest of Europe: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.3.8.7.5 Rest of Europe: Next-Generation Data Storage Market Breakdown, by Deployment

12.4 Asia Pacific

12.4.1 Asia Pacific Next-Generation Data Storage Market Overview

12.4.2 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.3 Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.3.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage System

12.4.4 Asia Pacific: Next-Generation Data Storage Market Breakdown, by End-user

12.4.4.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by End-user

12.4.5 Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.5.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Medium

12.4.6 Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.6.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Architecture

12.4.7 Asia Pacific: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.7.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Deployment

12.4.8 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.4.8.1 Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.4.8.2 China: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.2.1 China: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.2.2 China: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.2.3 China: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.2.4 China: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.2.5 China: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.8.3 Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.3.1 Japan: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.3.2 Japan: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.3.3 Japan: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.3.4 Japan: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.3.5 Japan: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.8.4 South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.4.1 South Korea: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.4.2 South Korea: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.4.3 South Korea: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.4.4 South Korea: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.4.5 South Korea: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.8.5 India: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.5.1 India: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.5.2 India: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.5.3 India: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.5.4 India: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.5.5 India: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.8.6 Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.6.1 Australia: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.6.2 Australia: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.6.3 Australia: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.6.4 Australia: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.6.5 Australia: Next-Generation Data Storage Market Breakdown, by Deployment

12.4.8.7 Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.4.8.7.1 Rest of APAC: Next-Generation Data Storage Market Breakdown, by Storage System

12.4.8.7.2 Rest of APAC: Next-Generation Data Storage Market Breakdown, by End-user

12.4.8.7.3 Rest of APAC: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.4.8.7.4 Rest of APAC: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.4.8.7.5 Rest of APAC: Next-Generation Data Storage Market Breakdown, by Deployment

12.5 Middle East and Africa

12.5.1 Middle East and Africa Next-Generation Data Storage Market Overview

12.5.2 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.5.3 Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage System

12.5.3.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage System

12.5.4 Middle East and Africa: Next-Generation Data Storage Market Breakdown, by End-user

12.5.4.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by End-user

12.5.5 Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.5.5.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Medium

12.5.6 Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.5.6.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Architecture

12.5.7 Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Deployment

12.5.7.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Deployment

12.5.8 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.5.8.1 Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.5.8.2 South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.5.8.2.1 South Africa: Next-Generation Data Storage Market Breakdown, by Storage System

12.5.8.2.2 South Africa: Next-Generation Data Storage Market Breakdown, by End-user

12.5.8.2.3 South Africa: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.5.8.2.4 South Africa: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.5.8.2.5 South Africa: Next-Generation Data Storage Market Breakdown, by Deployment

12.5.8.3 Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.5.8.3.1 Saudi Arabia: Next-Generation Data Storage Market Breakdown, by Storage System

12.5.8.3.2 Saudi Arabia: Next-Generation Data Storage Market Breakdown, by End-user

12.5.8.3.3 Saudi Arabia: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.5.8.3.4 Saudi Arabia: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.5.8.3.5 Saudi Arabia: Next-Generation Data Storage Market Breakdown, by Deployment

12.5.8.4 United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.5.8.4.1 United Arab Emirates: Next-Generation Data Storage Market Breakdown, by Storage System

12.5.8.4.2 United Arab Emirates: Next-Generation Data Storage Market Breakdown, by End-user

12.5.8.4.3 United Arab Emirates: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.5.8.4.4 United Arab Emirates: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.5.8.4.5 United Arab Emirates: Next-Generation Data Storage Market Breakdown, by Deployment

12.5.8.5 Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.5.8.5.1 Rest of Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage System

12.5.8.5.2 Rest of Middle East and Africa: Next-Generation Data Storage Market Breakdown, by End-user

12.5.8.5.3 Rest of Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.5.8.5.4 Rest of Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.5.8.5.5 Rest of Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Deployment

12.6 South and Central America

12.6.1 South and Central America Next-Generation Data Storage Market Overview

12.6.2 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.6.3 South and Central America: Next-Generation Data Storage Market Breakdown, by Storage System

12.6.3.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage System

12.6.4 South and Central America: Next-Generation Data Storage Market Breakdown, by End-user

12.6.4.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by End-user

12.6.5 South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.6.5.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Medium

12.6.6 South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.6.6.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Storage Architecture

12.6.7 South and Central America: Next-Generation Data Storage Market Breakdown, by Deployment

12.6.7.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Deployment

12.6.8 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.6.8.1 South and Central America: Next-Generation Data Storage Market – Revenue and Forecast Analysis – by Country

12.6.8.2 Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.6.8.2.1 Brazil: Next-Generation Data Storage Market Breakdown, by Storage System

12.6.8.2.2 Brazil: Next-Generation Data Storage Market Breakdown, by End-user

12.6.8.2.3 Brazil: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.6.8.2.4 Brazil: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.6.8.2.5 Brazil: Next-Generation Data Storage Market Breakdown, by Deployment

12.6.8.3 Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.6.8.3.1 Argentina: Next-Generation Data Storage Market Breakdown, by Storage System

12.6.8.3.2 Argentina: Next-Generation Data Storage Market Breakdown, by End-user

12.6.8.3.3 Argentina: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.6.8.3.4 Argentina: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.6.8.3.5 Argentina: Next-Generation Data Storage Market Breakdown, by Deployment

12.6.8.4 Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

12.6.8.4.1 Rest of South and Central America: Next-Generation Data Storage Market Breakdown, by Storage System

12.6.8.4.2 Rest of South and Central America: Next-Generation Data Storage Market Breakdown, by End-user

12.6.8.4.3 Rest of South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Medium

12.6.8.4.4 Rest of South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Architecture

12.6.8.4.5 Rest of South and Central America: Next-Generation Data Storage Market Breakdown, by Deployment

13. Competitive Landscape

13.1 Heat Map Analysis By Key Players

13.2 Company Positioning & Concentration

14. Industry Landscape

14.1 Overview

14.2 Market Initiative

14.3 New Product Development

15. Company Profiles

15.1 Dell Technologies Inc

15.1.1 Key Facts

15.1.2 Business Description

15.1.3 Products and Services

15.1.4 Financial Overview

15.1.5 SWOT Analysis

15.1.6 Key Developments

15.2 Hewlett Packard Enterprise Co

15.2.1 Key Facts

15.2.2 Business Description

15.2.3 Products and Services

15.2.4 Financial Overview

15.2.5 SWOT Analysis

15.2.6 Key Developments

15.3 NetApp Inc

15.3.1 Key Facts

15.3.2 Business Description

15.3.3 Products and Services

15.3.4 Financial Overview

15.3.5 SWOT Analysis

15.3.6 Key Developments

15.4 Hitachi Ltd

15.4.1 Key Facts

15.4.2 Business Description

15.4.3 Products and Services

15.4.4 Financial Overview

15.4.5 SWOT Analysis

15.4.6 Key Developments

15.5 International Business Machines Corp

15.5.1 Key Facts

15.5.2 Business Description

15.5.3 Products and Services

15.5.4 Financial Overview

15.5.5 SWOT Analysis

15.5.6 Key Developments

15.6 Pure Storage Inc

15.6.1 Key Facts

15.6.2 Business Description

15.6.3 Products and Services

15.6.4 Financial Overview

15.6.5 SWOT Analysis

15.6.6 Key Developments

15.7 DataDirect Networks Inc

15.7.1 Key Facts

15.7.2 Business Description

15.7.3 Products and Services

15.7.4 Financial Overview

15.7.5 SWOT Analysis

15.7.6 Key Developments

15.8 Fujitsu Ltd

15.8.1 Key Facts

15.8.2 Business Description

15.8.3 Products and Services

15.8.4 Financial Overview

15.8.5 SWOT Analysis

15.8.6 Key Developments

15.9 NETGEAR

15.9.1 Key Facts

15.9.2 Business Description

15.9.3 Products and Services

15.9.4 Financial Overview

15.9.5 SWOT Analysis

15.9.6 Key Developments

15.10 Huawei Technologies Co Ltd

15.10.1 Key Facts

15.10.2 Business Description

15.10.3 Products and Services

15.10.4 Financial Overview

15.10.5 SWOT Analysis

15.10.6 Key Developments

16. Appendix

16.1 About The Insight Partners

List of Tables

Table 1. Next-Generation Data Storage Market segmentation

Table 2. List of Vendors

Table 3. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Table 4. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million) – by Storage System

Table 5. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million) – by End-user

Table 6. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million) – by Storage Medium

Table 7. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million) – by Storage Architecture

Table 8. Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million) – by Deployment

Table 9. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 10. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 11. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 12. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 13. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 14. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Country

Table 15. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 16. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 17. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 18. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 19. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 20. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 21. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 22. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 23. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 24. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 25. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 26. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 27. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 28. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 29. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 30. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 31. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 32. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 33. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 34. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 35. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Country

Table 36. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 37. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 38. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 39. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 40. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 41. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 42. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 43. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 44. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 45. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 46. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 47. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 48. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 49. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 50. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 51. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 52. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 53. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 54. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 55. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 56. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 57. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 58. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 59. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 60. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 61. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 62. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 63. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 64. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 65. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 66. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 67. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 68. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 69. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 70. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 71. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Country

Table 72. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 73. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 74. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 75. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 76. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 77. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 78. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 79. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 80. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 81. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 82. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 83. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 84. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 85. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 86. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 87. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 88. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 89. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 90. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 91. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 92. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 93. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 94. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 95. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 96. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 97. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 98. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 99. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 100. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 101. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 102. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 103. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 104. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 105. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 106. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 107. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Country

Table 108. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 109. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 110. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 111. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 112. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 113. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 114. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 115. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 116. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 117. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 118. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 119. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 120. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 121. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 122. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 123. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 124. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 125. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 126. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 127. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 128. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 129. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 130. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 131. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 132. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 133. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Country

Table 134. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 135. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 136. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 137. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 138. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 139. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 140. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 141. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 142. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 143. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 144. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage System

Table 145. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by End-user

Table 146. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Medium

Table 147. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Storage Architecture

Table 148. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million) – by Deployment

Table 149.Heat Map Analysis By Key Players

List of Figures

Figure 1. Next-Generation Data Storage Market segmentation, by Geography

Figure 2. PEST Analysis

Figure 3. Ecosystem Analysis

Figure 4. Impact Analysis of Drivers and Restraints

Figure 5. Next-Generation Data Storage Market Revenue (US$ Million), 2022–2030

Figure 6. Next-Generation Data Storage Market Share (%) – by Storage System (2022 and 2030)

Figure 7. Direct Attached Storage (DAS): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 8. Network Attached Storage (NAS): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 9. Storage Area Network (SAN): Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 10. Next-Generation Data Storage Market Share (%) – by End-user (2022 and 2030)

Figure 11. BFSI: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 12. Retail: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 13. IT and telecom: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 14. Healthcare: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 15. Media and Entertainment: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 16. Others: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 17. Next-Generation Data Storage Market Share (%) – by Storage Medium (2022 and 2030)

Figure 18. Hard Disk Drive: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 19. Solid-State Drive: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 20. Tape: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 21. Next-Generation Data Storage Market Share (%) – by Storage Architecture (2022 and 2030)

Figure 22. File-Object based Storage: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 23. Block Storage: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 24. Next-Generation Data Storage Market Share (%) – by Deployment (2022 and 2030)

Figure 25. On-premise: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 26. Cloud-based: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 27. Hybrid: Next-Generation Data Storage Market – Revenue and Forecast to 2030 (US$ Million)

Figure 28. Next-Generation Data Storage Market Breakdown by Region, 2022 and 2030 (%)

Figure 29. North America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 30. North America: Next-Generation Data Storage Market Breakdown, by Storage System (2022 and 2030)

Figure 31. North America: Next-Generation Data Storage Market Breakdown, by End-user (2022 and 2030)

Figure 32. North America: Next-Generation Data Storage Market Breakdown, by Storage Medium (2022 and 2030)

Figure 33. North America: Next-Generation Data Storage Market Breakdown, by Storage Architecture (2022 and 2030)

Figure 34. North America: Next-Generation Data Storage Market Breakdown, by Deployment (2022 and 2030)

Figure 35. North America: Next-Generation Data Storage Market Breakdown, by Key Countries, 2022 and 2030 (%)

Figure 36. United States: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 37. Canada: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 38. Mexico: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 39. Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 40. Europe: Next-Generation Data Storage Market Breakdown, by Storage System (2022 and 2030)

Figure 41. Europe: Next-Generation Data Storage Market Breakdown, by End-user (2022 and 2030)

Figure 42. Europe: Next-Generation Data Storage Market Breakdown, by Storage Medium (2022 and 2030)

Figure 43. Europe: Next-Generation Data Storage Market Breakdown, by Storage Architecture (2022 and 2030)

Figure 44. Europe: Next-Generation Data Storage Market Breakdown, by Deployment (2022 and 2030)

Figure 45. Europe: Next-Generation Data Storage Market Breakdown, by Key Countries, 2022 and 2030 (%)

Figure 46. Germany: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 47. United Kingdom: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 48. France: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 49. Italy: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 50. Russian Federation: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 51. Rest of Europe: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 52. Asia Pacific: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 53. Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage System (2022 and 2030)

Figure 54. Asia Pacific: Next-Generation Data Storage Market Breakdown, by End-user (2022 and 2030)

Figure 55. Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage Medium (2022 and 2030)

Figure 56. Asia Pacific: Next-Generation Data Storage Market Breakdown, by Storage Architecture (2022 and 2030)

Figure 57. Asia Pacific: Next-Generation Data Storage Market Breakdown, by Deployment (2022 and 2030)

Figure 58. Asia Pacific: Next-Generation Data Storage Market Breakdown, by Key Countries, 2022 and 2030 (%)

Figure 59. China: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 60. Japan: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 61. South Korea: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 62. India: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 63. Australia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 64. Rest of APAC: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 65. Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 66. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage System (2022 and 2030)

Figure 67. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by End-user (2022 and 2030)

Figure 68. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Medium (2022 and 2030)

Figure 69. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Storage Architecture (2022 and 2030)

Figure 70. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Deployment (2022 and 2030)

Figure 71. Middle East and Africa: Next-Generation Data Storage Market Breakdown, by Key Countries, 2022 and 2030 (%)

Figure 72. South Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 73. Saudi Arabia: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 74. United Arab Emirates: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 75. Rest of Middle East and Africa: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 76. South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 77. South and Central America: Next-Generation Data Storage Market Breakdown, by Storage System (2022 and 2030)

Figure 78. South and Central America: Next-Generation Data Storage Market Breakdown, by End-user (2022 and 2030)

Figure 79. South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Medium (2022 and 2030)

Figure 80. South and Central America: Next-Generation Data Storage Market Breakdown, by Storage Architecture (2022 and 2030)

Figure 81. South and Central America: Next-Generation Data Storage Market Breakdown, by Deployment (2022 and 2030)

Figure 82. South and Central America: Next-Generation Data Storage Market Breakdown, by Key Countries, 2022 and 2030 (%)

Figure 83. Brazil: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 84. Argentina: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 85. Rest of South and Central America: Next-Generation Data Storage Market – Revenue and Forecast to 2030(US$ Million)

Figure 86. Company Positioning & Concentration

The List of Companies - Next-Generation Data Storage Market

- Dell Technologies Inc

- Hewlett Packard Enterprise Co

- NetApp Inc

- Hitachi Ltd

- International Business Machines Corp

- Pure Storage Inc

- DataDirect Networks Inc

- Fujitsu Ltd

- NETGEAR

- Huawei Technologies Co Ltd

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Next Generation Data Storage Market

Mar 2024

Remote Access Solution Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type [Secure Remote Access-VPN, Identity and Access Management (IAM) Solutions, Multi-Factor Authentication, Single Sign-On (SSO), Endpoint Security, and Others], Mode of Deployment (Cloud and On-Premise), End-Use Industry (IT and Telecommunications, BFSI, Healthcare, Government, Manufacturing, and Others), and Geography

Mar 2024

Hall Effect Teslameter Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Analog Hall Effect Teslameters and Digital Hall Effect Teslameters), End Users (Automotive, Industrial, Healthcare, Aerospace, Laboratory, and Others), and Geography

Mar 2024

Automotive Board to Board Connector Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Pin Headers, Sockets, Floating Connector, and Card Edge Connector), Pin Headers (Stacked Headers and Shrouded Headers), Application (Powertrain Control Systems, Infotainment and Navigation Systems, Advanced Driver Assistance Systems (ADAS), Electric Vehicles (EV) and Hybrid Vehicle Systems, Lighting Control Systems, Autonomous Vehicles, and Others), Pitch (Less Than 1 mm, 1–2 mm, and More Than 2 mm), Number of Pin (2–12 Pin, 13–30 Pin, 31–50 Pin, 51–100 Pin, and 100+ Pin), and Geography

Mar 2024

Radiation Hardened Motor Controller and Motor Drive Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Motor Controller and Motor Drive), Motor Drive (AC Drive, DC Drive, and BLDC), Application (Space Exploration, Military and Defense, Nuclear Power Plants, and Others), and Geography

Mar 2024

Pluggable Optics for Data Center Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Component (Switches, Routers, and Servers), Data Rate (100–400 Gb/s, 400–800 Gb/s, and 800 Gb/s and above), and Geography

Mar 2024

Doors and Windows Automation Market