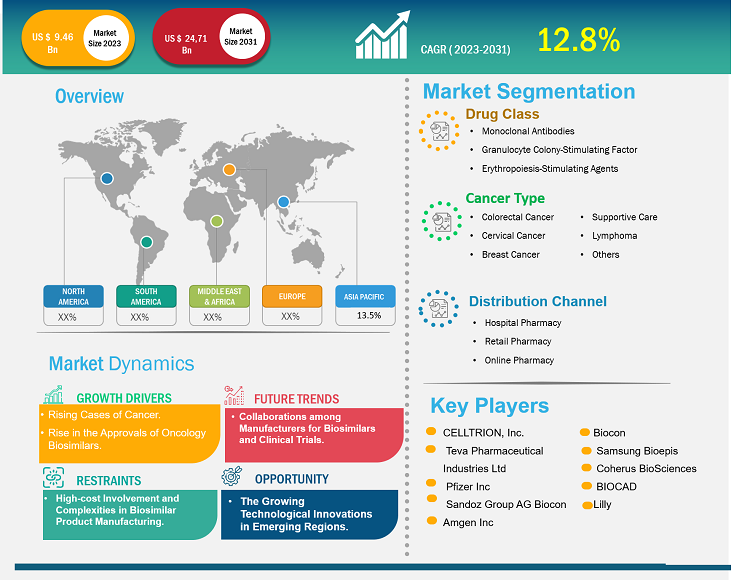

[Research Report] The oncology biosimilars market was valued at US$ 9.46 billion in 2023 and is anticipated to reach US$ 24.71 billion by 2031; it is projected to register a CAGR of 12.8% from 2023 to 2031.

Market Insights and Analyst View:

Biosimilars are biopharmaceutical products that closely resemble existing reference biologic drugs in terms of safety, efficacy, and quality but are not identical. Biosimilars such as monoclonal antibodies and supportive agents, including filgrastim, pegfilgrastim, epoetin α, and epoetin ζ, are available to treat various types of cancers. Factors such as a surge in incidences of cancers, the cost-effectiveness of biosimilar drugs, and a rise in the approvals of oncology biosimilars. Additionally, the collaborations among manufacturers for biosimilars and clinical trials are expected to bring new oncology biosimilars market trends in the coming years. However, high-cost involvement and complexities in biosimilar product manufacturing are among the market deterrent factors.

Oncology Biosimilars Market Size and Share – Market Drivers:

According to the World Health Organization (WHO), in 2022, ~20 million new cancer cases and 9.7 million deaths caused by cancer were reported worldwide. Additionally, the latest estimates from WHO’s Global Cancer Observatory indicated that in 2022, 10 different types of cancer accounted for approximately two-thirds of new cancer cases and deaths worldwide. Among these, lung cancer was the most commonly occurring cancer globally, accounting for 2.5 million new cases and 12.4% of the total new cases. Female breast cancer ranked second with 2.3 million cases and 11.6% of the total new cases, followed by colorectal cancer, accounting for 9.6% of the total new cases. Prostate cancer ranked fourth with 1.5 million cases, and stomach cancer ranked fifth with 970,000 cases. The advent of more affordable oncology biosimilars as a medical armamentarium can reduce the burden on healthcare expenditure and improve access to efficient cancer therapies because of their demonstrated safety and efficacy in real-world scenarios, clinical evidence, and physicochemical quality data. For instance, in an article published by the Multidisciplinary Digital Publishing Institute (MDPI) in July 2023, a comparative and descriptive study was performed to evaluate the safety information of biosimilar monoclonal antibodies (mAbs) used in cancer with that of the corresponding reference medicines and assess the post-marketing pharmacovigilance data. The study concluded that there were no significant variations in the safety profiles of bevacizumab, trastuzumab, and rituximab biosimilars and their originators. The results validated the safety equivalency of biosimilars and supported their use as competitive substitutes for biologic originators. Therefore, the growing burden of cancer and increasing deaths due to it creates the need for affordable treatments, which boosts the oncology biosimilars market growth.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Oncology Biosimilars Market: Strategic Insights

Market Size Value in US$ 9.46 billion in 2023 Market Size Value by US$ 24.71 billion by 2031 Growth rate CAGR of 12.8% from 2023 to 2031 Forecast Period 2023-2031 Base Year 2023

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Oncology Biosimilars Market: Strategic Insights

| Market Size Value in | US$ 9.46 billion in 2023 |

| Market Size Value by | US$ 24.71 billion by 2031 |

| Growth rate | CAGR of 12.8% from 2023 to 2031 |

| Forecast Period | 2023-2031 |

| Base Year | 2023 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Segmentation and Scope:

The “Oncology Biosimilars Market Analysis and Forecast to 2030” is a specialized and in-depth study focusing on the global market dynamics to help identify the key drivers, future market trends, and lucrative market opportunities that would, in turn, aid in identifying major revenue pockets. The report aims to provide an overview of the market with detailed market segmentation on the basis of drug class, cancer type, and distribution channel. The report also includes a comprehensive analysis of the leading market players and their key strategic developments. The scope of the oncology biosimilars market report includes the assessment of the market performance in North America, Europe, Asia Pacific, South & Central America, and the Middle East & Africa.

Segmental Assessment:

The market, based on drug class, is segmented into monoclonal antibodies, granulocyte colony-stimulating factors, and erythropoiesis-stimulating agents (ESAs) . In 2023, the monoclonal antibodies segment held the largest oncology biosimilars market share and is anticipated to register the highest CAGR from 2023 to 2031. Monoclonal antibodies can destroy cancer cells through multiple methods, such as by obstructing ligand-receptor growth and survival pathways. The primary mechanism of action includes antibody-dependent cellular cytotoxicity (ADCC) and complement-mediated cytotoxicity. Rituximab, Trastuzumab, and Bevacizumab were a few biosimilar monoclonal antibodies approved by the European Medicines Agency (EMA) and the Food and Drug Administration (FDA) for cancer treatment until December 2019.

The market, based on cancer type, is categorized as colorectal cancer, cervical cancer, breast cancer, supportive care, lymphoma, and others. The supportive care segment held the largest market share in 2023. Colorectal cancer is projected to register the highest CAGR from 2023 to 2031. According to WHO, cancer is a critical health concern and the primary cause of fatalities globally. With the growing prevalence of cancer, many oncology biosimilar manufacturers are engaged in developing and launching new products in the market. For instance, CT-P16 by Celltrion, 163 HD204 by Prestige Biopharma, CBT124 by Cipla Biotech, and MIL60 by Beijing Mabworks Biotech are potential biosimilars of bevacizumab that are currently undergoing phase 3 studies and being compared on the parameters of safety and efficacy. They are also being evaluated for their ability to treat patients suffering from non-small cell lung cancer.

The market, based on distribution channel, is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. In 2022, the hospital pharmacy segment held the largest market share. Online pharmacy segment is expected to register the highest CAGR from 2023 to 2031. Hospital pharmacies are the primary platform where patients can buy prescription drugs such as biosimilars.

Regional

Analysis:

In terms of revenue, North America accounted for a major oncology biosimilars market share in 2023, followed by Europe. The growing cases of cancer, rising approvals of biosimilars for cancer treatment, and the advanced healthcare infrastructure are the factors anticipated to propel the oncology biosimilars market in North America during the forecast period.

The growing cases of cancer, rising approvals of biosimilars for cancer treatment, and the advanced healthcare infrastructure are the factors anticipated to propel the oncology biosimilars market in North America. Biologics are the most expensive medicines in the US. Biosimilars are expected to be more cost-effective than their reference products. In an article published by PubMed Central in October 2022, a cost comparison was conducted using the average wholesale price (AWP) per unit of biologics and biosimilars based on the drug prices in the US as of June 2021. The analysis stated that biosimilars can offer savings of 15–23% for bevacizumab. Among bevacizumab biosimilars, Zirbes offers significantly higher savings when compared to the originator product, Avastin. Biosimilars for supportive cancer care agents such as Filgrastim biosimilars offer savings ranging from 17.3% to 34% when compared to their reference products, while pegfilgrastim biosimilars offer savings from 33% to 37%. Also, Epogen biosimilar offers savings of 33.5%. According to the Cardinal Health Biosimilars Report published in 2022, the FDA has approved 33 biosimilars in the US, and 21 are commercially available. Out of these, 17 are being used for cancer treatments. As per the same source, biosimilars are expected to reduce US drug expenditure by US$ 133 billion by 2025. Thus, in the US, biosimilars have immense potential for lowering the costs of biologic medicine, making care more accessible to patients, and creating innovations and scientific breakthroughs, thereby driving the oncology biosimilars market in this region.

Oncology Biosimilars Market Report Scope

Industry Developments and Future Opportunities:

The oncology biosimilars market forecast can help stakeholders in this marketplace plan their growth strategies. As per the company press release, below are a few key developments and initiatives taken by key players operating in the oncology biosimilars market:

- In November 2022, Organon launched a biosimilar of Avastin, AYBINTIO, in Canada. The treatment is available for patients in Canada who are affected by certain aggressive forms of cancer, including metastatic colorectal cancer (mCRC); metastatic lung cancer; platinum-sensitive and resistant recurrent epithelial ovarian, including fallopian tube and primary peritoneal cancer; and glioblastoma. This launch aims to expand the company's biosimilar portfolio.

- In May 2022, Biocon Biologics and Viatris launched Abemy, a biosimilar to Roche’s Avastin (Bevacizumab). Biocon Biologics Ltd., a subsidiary of Biocon Ltd., and Vietris’ Inc. announced the availability of this oncology biosimilar in Canada. bevy, co-developed by Biocon Biologics and Vietri’s, has been approved by Health Canada for four types of cancers.

- In April 2020, Pfizer received approval from the European Commission (EC) for RUXIENCE, which is a monoclonal antibody (mob) and biosimilar to Mather (rituximab). This approval was for treating certain cancers, such as non-Hodgkin’s lymphoma (NHL), chronic lymphocytic leukemia (CLL), and autoimmune conditions.

- In January 2020, Chorus Biosciences entered into a license agreement with Innocents Biologics Co., Ltd. for the development and commercialization of bevacizumab (Avastin) biosimilar of any dosage form and presentation in the US and Canada.

Competitive Landscape and Key Companies:

CELLTRION, Inc.; Teva Pharmaceutical Industries Ltd; Pfizer Inc; Sandoz Group AG; Biocon; Amgen Inc; Samsung Bioepis; Coherus BioSciences; BIOCAD; and Lilly are among the top players profiled in the oncology biosimilars market report. These companies focus on presenting new hi-tech products, technological advancements in existing products, and geographic expansions to meet the growing consumer demand worldwide.

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Drug Class, Cancer Type, and Distribution Channel

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

Biosimilars are biopharmaceutical products that closely resemble existing reference biologic drugs in terms of safety, efficacy, and quality but are not identical. Biosimilars such as monoclonal antibodies and supportive agents, including filgrastim, pegfilgrastim, epoetin α, and epoetin ζ, are available to treat various types of cancers.

The oncology biosimilars majorly consists of the players, including CELLTRION, Inc.; Teva Pharmaceutical Industries Ltd; Pfizer Inc; Sandoz Group AG; Biocon; Amgen Inc; Samsung Bioepis; Coherus BioSciences; BIOCAD; and Lilly.

Key factors driving the oncology biosimilars growth are the surging in incidences of cancers, the cost-effectiveness of biosimilar drugs, and a rise in the approvals of oncology biosimilars.

The oncology biosimilars market is segmented into monoclonal antibodies, granulocyte colony-stimulating factor, and erythropoiesis-stimulating agents.

The oncology biosimilars is expected to be valued at US$ 24.71 billion in 2031.

The oncology biosimilars was valued at US$ 9.46 billion in 2023.

1. Introduction

1.1 Scope of the Study

1.2 Market Definition, Assumptions and Limitations

1.3 Market Segmentation

2. Executive Summary

2.1 Key Insights

2.2 Market Attractiveness Analysis

3. Research Methodology

4. Oncology Biosimilars Market Landscape

4.1 Overview

4.2 PEST Analysis

4.3 Ecosystem Analysis

4.3.1 List of Vendors in the Value Chain

5. Oncology Biosimilars Market - Key Market Dynamics

5.1 Key Market Drivers

5.2 Key Market Restraints

5.3 Key Market Opportunities

5.4 Future Trends

5.5 Impact Analysis of Drivers and Restraints

6. Oncology Biosimilars Market - Global Market Analysis

6.1 Oncology Biosimilars - Global Market Overview

6.2 Oncology Biosimilars - Global Market and Forecast to 2031

7. Oncology Biosimilars Market – Revenue Analysis (USD Million) – By Drug Class, 2021-2031

7.1 Overview

7.2 Monoclonal Antibodies

7.3 Erythropoiesis-Stimulating Agents

7.4 Granulocyte Colony-Stimulating Factor (G-CSF)

8. Oncology Biosimilars Market – Revenue Analysis (USD Million) – By Cancer Type, 2021-2031

8.1 Overview

8.2 Colorectal Cancer

8.3 Cervical Cancer

8.4 Breast Cancer

8.5 Supportive Care

8.6 Lymphoma

8.7 Others

9. Oncology Biosimilars Market – Revenue Analysis (USD Million) – By Distribution Channel , 2021-2031

9.1 Overview

9.2 Hospital Pharmacy

9.3 Retail Pharmacy

9.4 Online Pharmacy

10. Oncology Biosimilars Market - Revenue Analysis (USD Million), 2021-2031 – Geographical Analysis

10.1 North America

10.1.1 North America Oncology Biosimilars Market Overview

10.1.2 North America Oncology Biosimilars Market Revenue and Forecasts to 2031

10.1.3 North America Oncology Biosimilars Market Revenue and Forecasts and Analysis - By Drug Class

10.1.4 North America Oncology Biosimilars Market Revenue and Forecasts and Analysis - By Cancer Type

10.1.5 North America Oncology Biosimilars Market Revenue and Forecasts and Analysis - By Distribution Channel

10.1.6 North America Oncology Biosimilars Market Revenue and Forecasts and Analysis - By Countries

10.1.6.1 United States Oncology Biosimilars Market

10.1.6.1.1 United States Oncology Biosimilars Market, by Drug Class

10.1.6.1.2 United States Oncology Biosimilars Market, by Cancer Type

10.1.6.1.3 United States Oncology Biosimilars Market, by Distribution Channel

10.1.6.2 Canada Oncology Biosimilars Market

10.1.6.2.1 Canada Oncology Biosimilars Market, by Drug Class

10.1.6.2.2 Canada Oncology Biosimilars Market, by Cancer Type

10.1.6.2.3 Canada Oncology Biosimilars Market, by Distribution Channel

10.1.6.3 Mexico Oncology Biosimilars Market

10.1.6.3.1 Mexico Oncology Biosimilars Market, by Drug Class

10.1.6.3.2 Mexico Oncology Biosimilars Market, by Cancer Type

10.1.6.3.3 Mexico Oncology Biosimilars Market, by Distribution Channel

Note - Similar analysis would be provided for below mentioned regions/countries

10.2 Europe

10.2.1 Germany

10.2.2 France

10.2.3 Italy

10.2.4 Spain

10.2.5 United Kingdom

10.2.6 Rest of Europe

10.3 Asia-Pacific

10.3.1 Australia

10.3.2 China

10.3.3 India

10.3.4 Japan

10.3.5 South Korea

10.3.6 Rest of Asia-Pacific

10.4 Middle East and Africa

10.4.1 South Africa

10.4.2 Saudi Arabia

10.4.3 U.A.E

10.4.4 Rest of Middle East and Africa

10.5 South and Central America

10.5.1 Brazil

10.5.2 Argentina

10.5.3 Rest of South and Central America

11. Industry Landscape

11.1 Mergers and Acquisitions

11.2 Agreements, Collaborations, Joint Ventures

11.3 New Product Launches

11.4 Expansions and Other Strategic Developments

12. Competitive Landscape

12.1 Heat Map Analysis by Key Players

12.2 Company Positioning and Concentration

13. Oncology Biosimilars Market - Key Company Profiles

13.1 Biocon

13.1.1 Key Facts

13.1.2 Business Description

13.1.3 Products and Services

13.1.4 Financial Overview

13.1.5 SWOT Analysis

13.1.6 Key Developments

Note - Similar information would be provided for below list of companies

13.2 Celltrion Inc

13.3 Samsung Bioepis

13.4 Amgen Inc

13.5 Coherus BioSciences

13.6 Pfizer Inc

13.7 Sandoz International GmbH (A Novartis Division)

13.8 Teva Pharmaceutical Industries Ltd.

13.9 Lilly

13.10 BIOCAD

14. Appendix

14.1 Glossary

14.2 About The Insight Partners

14.3 Market Intelligence Cloud

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Oncology Biosimilars Market

Mar 2024

Pediatric Cardiology Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Transcatheter Heart Valves, Occlusion Devices, Catheters, Stents, Introducer Sheaths, and Others), Disease Indication (Congenital Heart Disease, Acquired Heart Disease, Arrhythmias, Cardiomyopathies, and Others), Surgical Procedure (Interventional Procedures, Heart Rhythm Management Procedures, and Others), End User (Hospitals, Specialty Clinics, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2024

Pharmaceutical Membrane Filters Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technology (Microfiltration, Ultrafiltration, Reverse Osmosis and Nanofiltration), Design (Hollow Fiber, Spiral Wound, Tubular System and Plate and Frame), Material (Polyethersulfone (PES), Polysulfone (PS), Cellulose-Based Membranes, Polytetrafluoroethylene (PTFE), Polyvinyl Chloride (PVC), Polyacrylonitrile (PAN) and Others), End User (Pharmaceutical and Biotech Industries and CROs and CDMOs), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South & Central America)

Mar 2024

ECG Devices Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Resting ECG and Stress ECG), Lead Type (12-Lead ECG, 3–6 Lead ECG, and Single Lead), Technology [Portable (Wired) ECG System and Wireless ECG System], End User (Hospital and Clinics, Ambulatory Surgical Centers, Cardiac Centers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Mar 2024

Surgical Laser Fiber Units Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (CO2 Laser, Diode Laser, Erbium Laser, Nd:YAG Laser, Holmium Laser, Alexandrite Laser, and Others), Material (Silica-Based Fibers, Quartz Fibers, Polymer-Based Fibers, Multimode Fibers, and Others), Power (Low-Power Lasers, Medium-Power Lasers, and High-Power Lasers), Application (Urology, Dermatology, Gynecology, Cardiology, Neurology, Ophthalmology, Respiratory, Dentistry and Others), Wavelength (9,301 nm and above, 2,941–9,300 nm, and 1,441–2,940 nm, 821–1,440 nm, 710–820 nm, and below 710 nm), End User (Hospitals, Specialty Clinics, Physician Office, and Others), and Geography

Mar 2024

Therapeutic Vaccines Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Cancer Vaccines, Infectious Disease Vaccines, and Others), Technology (Allogenic Vaccines and Autologous Vaccines), End User (Hospitals, Clinics, and Others), and Geography

Mar 2024

Medical Cables Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Disposable Medical Cables, Reusable Medical Cables, and Custom Medical Cables), Applications [Diagnostics (Ultrasound Cables, Endoscopy Cables, Patient Interface Cables, and Others), Motorized Equipment, Patient Monitoring (ECG Cables, SpO2 Cables, NiBP Cables, EEG Cables, and Others), Surgical and Life Support (Fiber Optics, Modular Local Area Network, and Others), and Others], End User (Hospital and Clinics, Diagnostic Laboratories and Imaging Centers, Ambulatory Surgical Centers, and Others), and Geography

Mar 2024

Laser-Assisted ENT Surgeries Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (C02 Laser, Nd:YAG Laser, Diode Laser, Blue Laser, KTP Laser, Argon Laser, and Other Laser Types), Surgery Type [Laser Laryngeal Surgery, Laser Endoscopic Sinus Surgery (LESS), Laser-Assisted Uvulopalatoplasty (LAUP), Laser-Assisted Stapedotomy, Laser-Assisted Tonsillectomy and Adenoidectomy, Laser Turbinates Reduction, Transoral Laser Microsurgery (TLM), Nasal Surgery, and Other Surgery Types], End User (Hospitals and Specialty Clinics, Physician Offices, and Other End Users), and Geography (North America, Europe, Asia Pacific, South and Central America, and Middle East and Africa)

Mar 2024

Mobile Cleanroom Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Softwall and Hardwall), End User (Microelectronics Industry, Pharmaceuticals and Biotechnology Industry, Medical Device Manufacturers, and Others), and Geography

Get Free Sample For

Get Free Sample For