痤疮药物市场分析及预测(按规模、份额、增长、趋势)2030

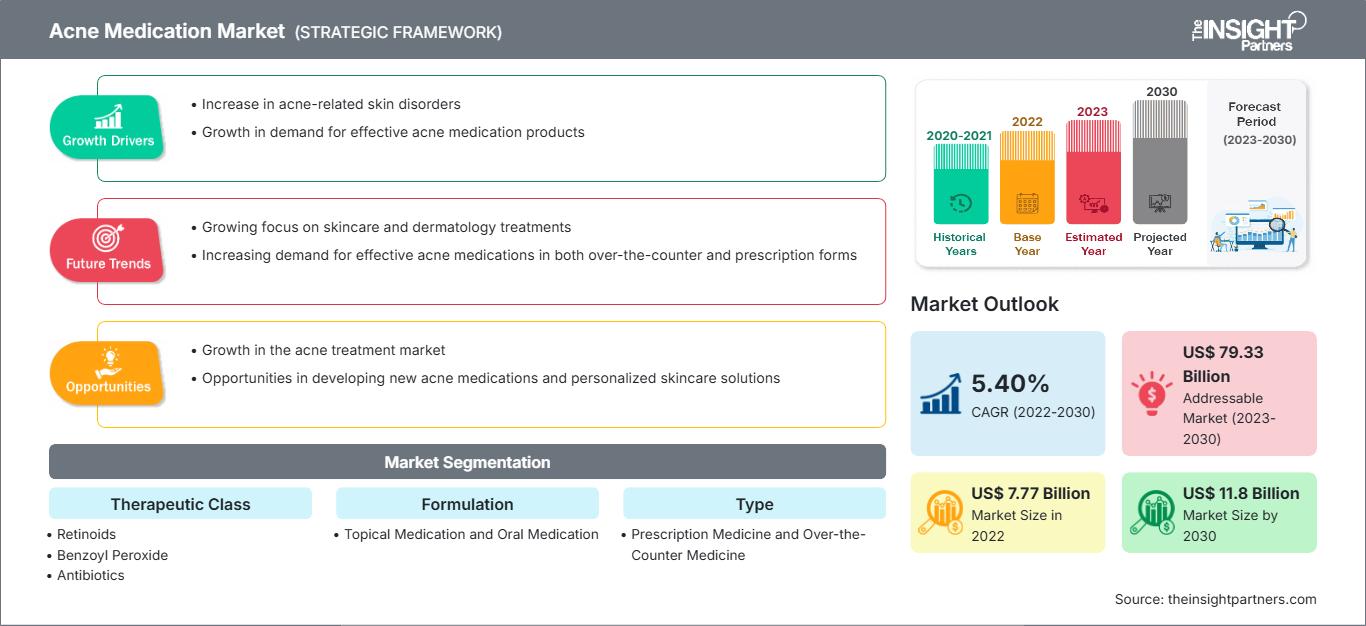

历史数据 : 2020-2021 | 基准年 : 2022 | 预测期 : 2023-2030痤疮药物市场规模和预测(2020-2030 年)、全球和区域份额、趋势和增长机会分析报告范围:按治疗类别(维甲酸、过氧化苯甲酰、抗生素、水杨酸等)、剂型(外用药和口服药)、类型(处方药和非处方药)、痤疮类型(非炎症性痤疮和炎症性痤疮)、分销渠道(药店、零售店和电子商务)和地理位置

- 状态 : 已发布

- 报告代码 : TIPRE00004587

- 类别 : 生命科学

- 页数 : 229

- 可用报告格式 :

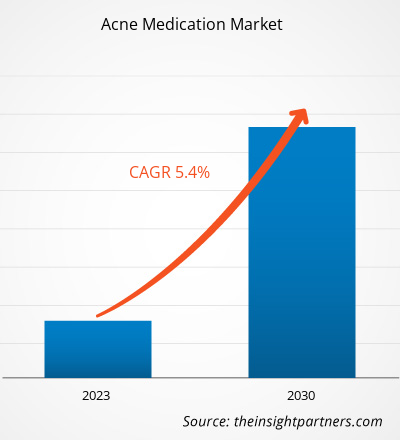

[研究报告] 痤疮药物市场价值预计将从 2022 年的 77.7456 亿美元增长到 2030 年的 118.0229 亿美元。预计该市场在 2022 年至 2030 年期间的复合年增长率将达到 5.40%。

市场洞察和分析师观点:

本报告中提供的痤疮药物市场预测可以帮助该市场的利益相关者规划其增长战略。痤疮是一种常见的皮肤病,其特征是皮肤上出现粉刺(黑头和白头)、丘疹、脓疱、结节和囊肿。它通常发生在面部、颈部、胸部、背部和肩部。它主要是由油脂分泌过多、毛囊堵塞、细菌和炎症等因素引起的。痤疮的严重程度各不相同,从轻微的偶尔爆发到严重的持续性症状,可能导致疤痕和心理困扰。目前有各种药物和疗法可以有效控制痤疮。然而,痤疮药物的副作用阻碍了市场的增长。此外,痤疮药物市场趋势包括对有机和天然疗法的需求激增。

增长动力和制约因素:

严重痤疮通常以疼痛性囊肿、结节和持续性炎症为特征,是严重的挑战,会严重影响人们的生活质量。根据2022年全球疾病发展报告 (GBD) 的研究,痤疮的患病率为9.4%,在全球最常见的疾病中排名第八。寻常痤疮影响着超过85%的12至25岁年龄段的年轻人。如此高的发病率导致对有效治疗中度至重度痤疮的药物的需求激增。随着人们寻求减轻严重痤疮带来的身心负担的方法,对先进、更有效的处方药和非处方药的需求也相应增加。这种趋势促使制药公司专注于开发创新配方,包括外用维甲酸、口服抗生素、激素疗法和先进的外用疗法,以满足严重痤疮患者的复杂需求。《皮肤病学药物杂志》(JDD)估计,痤疮治疗每年给美国经济造成的直接成本超过 10 亿美元,其中非处方痤疮药物占该成本的近 10%。JDD 还估计,未来几年用于痤疮治疗的支出将达到数十亿美元。因此,严重痤疮患病率的上升以及相关经济成本的飙升,进一步扩大了痤疮药物市场的规模。

另一方面,许多传统和全身性痤疮治疗,包括口服抗生素、维甲酸和激素疗法,都与一系列潜在的不良反应相关,例如皮肤干燥、刺激、光敏性、胃肠道不适,以及在极少数情况下更严重的全身性副作用。这些潜在的不良反应引起了患者和医疗保健提供者的担忧,导致他们不愿采用某些痤疮药物,尤其是长期使用。副作用也导致治疗依从性不足,因为患者可能会因为无法忍受或不良的副作用而选择停用或避免使用某些药物。因此,消费者倾向于优先考虑疗效并最大程度减少不良反应的先进配方和治疗方式,这引发了对新型、更耐受、耐受性更好的痤疮药物的持续需求。因此,痤疮药物的副作用限制了痤疮药物市场的增长。

自定义此报告以满足您的要求

您将免费获得任何报告的定制,包括本报告的部分内容,或国家级分析、Excel 数据包,以及为初创企业和大学提供超值优惠和折扣

痤疮药物市场: 战略洞察

-

获取本报告的主要市场趋势。这个免费样本将包括数据分析,从市场趋势到估计和预测。

趋势:

随着人们越来越意识到传统护肤品中使用的合成成分和化学物质的潜在危害,全球对被认为更安全、更温和、更环保的天然和有机替代品的需求日益增长。消费者越来越寻求不含刺激性化学物质、人工香料和潜在刺激性物质的产品,选择利用植物成分、植物提取物、精油和其他以护肤功效而闻名的天然化合物的配方。为了顺应这一趋势,许多护肤品牌和制造商正在开发各种天然和有机痤疮治疗产品,以满足注重健康的消费者的需求。这些产品通常含有茶树油、金缕梅、芦荟、绿茶提取物和水杨酸等天然来源的成分,在不影响疗效的情况下,提供更全面、更可持续的痤疮治疗方法。 2022年7月,有机护肤品牌MÁDARA推出了两款全新天然日常护肤产品——一款平衡微生物组的保湿霜和一款不干燥的洁面乳。该公司声称,这些产品融合了科学与自然,并经过特别配制,可为不同肤色、易长痘痘的人群提供温和呵护。两款产品均采用天然、有机和纯素成分——北方杜松干细胞、发酵多糖、地衣和马黛茶提取物——专门针对瑕疵,保护肌肤免受伤害。成人和青少年均可使用。因此,预计未来几年对天然和有机痤疮治疗方案的日益偏好将继续塑造痤疮药物市场的未来。

报告细分和范围:

痤疮药物市场分析通过考虑以下细分进行:治疗类别、配方、类型、痤疮类型和分销渠道。根据治疗类别,市场细分为类维生素 A、过氧化苯甲酰、抗生素、水杨酸等。就配方而言,市场分为外用药和口服药。痤疮药物市场按用途分为处方药和非处方药。根据痤疮类型,痤疮药物市场分为非炎症性痤疮和炎症性痤疮。根据分销渠道,市场分为药店、零售店和电子商务。就地域而言,痤疮药物市场分为北美(美国、加拿大和墨西哥)、欧洲(德国、法国、意大利、英国、俄罗斯和欧洲其他地区)、亚太地区(澳大利亚、中国、日本、印度、韩国和亚太其他地区)、中东和非洲(南非、沙特阿拉伯、阿联酋和中东和非洲其他地区)以及南美洲和中美洲(巴西、阿根廷和南美洲其他地区)。

分部分析:

根据治疗类别,类维生素 A 药物在 2022 年占据了痤疮药物市场的最大份额。预计同一细分市场在 2022 年至 2030 年期间将在市场上实现显著的复合年增长率。类维生素 A 只能凭医生处方购买,其主要成分是维生素 A;它们的作用机制与视黄醇相似,但在治疗痤疮方面比后者效力更强、效果更好。类视黄酸可作为口服胶囊和外用药物。维甲酸、阿达帕林和异维甲酸是众所周知的类视黄酸;异维甲酸的口服制剂有时被称为罗可维甲酸。类视黄酸的常用剂量为每公斤患者体重 0.1-1%(外用)和 0.5-1 毫克(口服)。

根据剂型,痤疮药物市场分为外用药和口服药。2022 年,外用药在痤疮药物市场中占有较大份额。预计同一领域在 2022 年至 2030 年期间的市场复合年增长率将显著提高。外用制剂在痤疮的管理和治疗中起着至关重要的作用,可将活性成分直接输送到受影响的皮肤区域。各种类型的外用痤疮药物包括凝胶、乳霜、乳液、泡沫和溶液,每种产品都针对特定的痤疮问题和肤质量身定制。这些配方通常含有维甲酸、过氧化苯甲酰、水杨酸和抗生素等成分,每种成分在对抗痤疮爆发方面发挥着不同的作用。

根据类型,市场分为处方药和非处方药。处方药在2022年占据了更大的痤疮药物市场份额。皮肤科医生或医疗保健提供者通常会在全面评估患者的痤疮类型、严重程度以及对既往治疗的反应后开具处方。处方痤疮药物涵盖多种选择,包括外用药物、口服药物、联合疗法以及针对特定痤疮问题的定制配方。处方药旨在为中度至重度痤疮患者提供有针对性的强效解决方案。

痤疮药物市场按分销渠道细分为零售店、药房和药店,以及其他基于模式的渠道。 2022年,药房和药店占据了最大的市场份额。药房和药店凭借其便捷性、私密性和价格实惠(与私人医生相比)的优势,成为医疗服务、物资和知识的重要来源。近年来,药房和药店因其能够帮助管理各种疾病和病症,从而增进健康的能力,在许多国家获得了认可。药房和药店通常拥有知识渊博的员工,能够指导顾客根据个人肤质和问题选择合适的痤疮药物。

区域分析:

痤疮药物市场报告的地理范围涵盖北美、欧洲、亚太地区、中东和非洲以及南美洲和中美洲。2022年,北美占据了全球痤疮药物市场的最大份额。

痤疮是一种由碎屑、油脂、皮脂和死皮细胞堵塞毛囊引起的皮肤病。根据美国皮肤病学会的数据,痤疮是美国最常见的皮肤疾病,每年有多达5000万美国人饱受痤疮的困扰,使其成为美国最常见的皮肤病。由于美国人痤疮发病率的上升以及随之而来的各种创新痤疮药物的上市,美国的痤疮药物市场预计将持续增长。此外,人们对个人护理、皮肤健康和外观的日益关注也刺激了对痤疮药物的需求。技术进步和研究推动了创新型痤疮治疗产品的开发,这些产品疗效更佳,副作用更小,这进一步促进了美国痤疮药物市场的增长,因为美国民众更愿意投资于能够达到预期效果的高质量产品。

预计在2022年至2030年期间,亚太地区痤疮药物市场的复合年增长率将最高。中国是该地区最大的痤疮药物市场。中国痤疮药物市场的发展受到多种因素的推动。值得注意的是,人工智能远程医疗的广泛应用彻底改变了皮肤病护理,提高了治疗的可及性,并提供了更佳的个性化治疗。AIDERMA 是中国首个全方位的皮肤病人工智能辅助诊断和治疗平台。咨询、教育以及诊疗支持是 AIDERMA 的主要服务内容。AIDERMA 提供 90 多种常见皮肤病的辅助诊断和治疗。AIDERMA 声称这是一种简单易行的程序,可提供诊断和潜在的治疗方案。超过 7,000 名临床医生已注册 AIDDA,这款应用程序允许中国医生诊断牛皮癣、湿疹和特应性皮炎。

痤疮药物

痤疮药物市场区域洞察The Insight Partners 的分析师已详尽阐述了预测期内影响痤疮药物市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的痤疮药物市场细分和地域分布。

痤疮药物市场报告范围

| 报告属性 | 细节 |

|---|---|

| 市场规模 2022 | US$ 7.77 Billion |

| 市场规模 2030 | US$ 11.8 Billion |

| 全球复合年增长率 (2022 - 2030) | 5.40% |

| 历史数据 | 2020-2021 |

| 预测期 | 2023-2030 |

| 涵盖的领域 |

By 治疗类

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

痤疮药物市场参与者密度:了解其对业务动态的影响

痤疮药物市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求的驱动因素包括消费者偏好的演变、技术进步以及对产品益处的认知度的提升。随着需求的增长,企业正在扩展产品线,不断创新以满足消费者需求,并抓住新兴趋势,从而进一步推动市场增长。

- 获取 痤疮药物市场 主要参与者概述

行业发展和未来机遇:

根据公司新闻稿,全球痤疮药物市场知名参与者的不同举措如下:

- 2023 年 9 月,Cosmo Pharmaceuticals NV(爱尔兰)和 Glenmark Pharmaceuticals(孟买)的子公司 Glenmark Specialty SA 宣布签署分销和许可协议,以在南非和欧洲分销 Winlevi(1% clascoterone 乳膏)。协议规定,Glenmark 将获得在 15 个欧盟国家(萨宾、保加利亚、捷克共和国、丹麦、芬兰、法国、匈牙利、冰岛、荷兰、挪威、波兰、葡萄牙、罗马尼亚、斯洛伐克和瑞典)以及南非和英国通过 Cosmo 子公司 Cassiopea 销售 Winlevi 的独家权利。

- 2023 年 10 月,Crown Laboratories 的子公司 Crown Therapeutics 在其经皮肤科医生认可且屡获殊荣的 PanOxyl 系列中增加了两款新的 PanOxyl 产品——含 2% 水杨酸的 PanOxyl 净化去角质霜和 0.1% 的 PanOxyl 阿达帕林凝胶。2023 年 9 月,Sun Pharmaceutical Industries Limited 的全资子公司 Sun Pharma Canada Inc. 宣布 WINLEVI(clascoterone 乳膏,1% w/w)可在加拿大上市。对于12岁及以上的患者,WINLEVI是第一个也是唯一一个推荐用于局部治疗寻常痤疮(即痤疮)的雄激素受体抑制剂。

竞争格局和主要公司:

Teva Pharmaceutical Industries Ltd、Mayne Pharma Group Ltd、Almirall SA、Johnson & Johnson、Sun Pharmaceutical Industries Ltd、Bausch Health Companies Inc、Centro Internacional de Cosmiatria SA de CV、Galderma SA、Pfizer Inc.、GSK Plc、Viatris Inc、Somar Sapi De CV、Carnot Technologies 和 Italmex SA 是痤疮药物市场报告中介绍的几家主要公司。这些公司专注于开发和采用新技术、改进现有产品以及扩大其地理覆盖范围,以满足全球日益增长的消费者需求。

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 痤疮药物市场

获取免费样品 - 痤疮药物市场