分析师的观点

医疗保健 EDI 市场分析解释了市场驱动因素,例如无缝处理医疗保健索赔和行政交易的需求不断增长,以及越来越多的采用供应链跟踪中的医疗保健 EDI 平台。此外,医疗保健 EDI 的技术进步预计将在 2022 年至 2030 年期间引入市场新趋势。从组件来看,2022年解决方案细分市场将占据更大份额。从交付模式来看,基于网络和基于云的细分市场占据最大份额,占据市场主导地位。从应用来看,理赔管理细分市场占据最大份额,占据市场主导地位。按最终用户细分来看,医疗保健提供商细分市场可能在 2022 年至 2030 年期间占据医疗保健 EDI 市场的相当大份额。

医疗保健中的电子数据交换 (EDI) 是在医疗保健机构、保险公司之间传输数据的安全方式以及使用既定消息格式和标准的患者。

市场洞察

无缝处理医疗保健索赔和管理交易的需求不断增长

EDI 是一种传输医疗保健数据的安全方式。诊所、医院、医疗机构和其他医疗保健公司经常使用 EDI 来传输医疗信息。 ASC X12 版本 5010 就是这样的一个例子。 ASC X12 制定和维护与医疗保健管理交易相关的 EDI 标准。以下是牙科行业中经常采用的一些常用 ASC X12 交易。

牙科行业中常用的 ASC X12 交易

交易类型

说明

ASC X12 270

此交易允许提供商检查患者是否有保险。国家牙科电子数据交换委员会 (NDEDIC) 致力于促进牙科行业内 ASC X12 270/271 的高利用率。

ASC X12 271

此交易是对资格查询的电子回复。消费者的回复显示患者是否有保险,并相应地为患者提供可用的福利。

ASC X12 275

ASC X12 275 是一种电子交易,用于通过发送“ASC X12”来回复保险公司的信息277 向提供商发送的 RFI。ASC X12 275 包含附加数据和/或数字图像(X 射线、牙周图、治疗笔记等)以支持医疗保健声明。该交易并未广泛使用。

其他 ASC X12

其他交易包括 ASC X12 276、ASC X12 277、ASC X12 277CA、ASC X12 277U、ASC X12 RFI、ASC X12 837、ASC X12 835、ASC X12 997、ASC X12 999

来源:The Insight Partners分析

此外,医疗保健 EDI 显着减少了提交和处理索赔所需的时间。例如,EDI 不仅有助于识别要提交的索赔中的潜在错误,还有助于处理和提供有关索赔的实时反馈。索赔提交。例如,EDI 的实用程序使手动流程自动化,消除了纸张、打印、物理存储并节省了成本。此外,与手动流程相比,电子文档的处理速度更快,确保满足客户需求并让客户满意。此外,在医疗保健领域采用 EDI 有助于降低医疗保健成本并使流程顺利进行。 Ramsay Healthcare 采用 GS1 EDI 就是这样一个例子。 Ramsay Healthcare 部署了一整套 GS1 标准,用于识别、捕获和共享支持与供应商互动的信息。因此,采用 GS1 标准套件 Ramsay Healthcare 提高了采购流程的速度和效率,从而有效支持医院的运营并帮助确保持续提供优质医疗保健。由于采用 GS1 标准套件,Ramsay Healthcare 中每份文档的采购到付款处理成本已降低约 95%。因此,医疗保健效率使医疗保健索赔能够通过 EDI 更快地处理,最终推动市场增长。

未来趋势

医疗保健 EDI 的技术进步

医疗保健组织每天处理大量数据,从患者开始实验室结果和处方的记录和声明。根据 Astera Software 于 2023 年发布的报告,美国约 50% 的医院拥有非结构化数据,这对改善整体医疗保健互操作性和互联护理计划造成了重大障碍。因此,技术进步是一种可靠的解决方案,可以帮助医院克服与医院生成的数据相关的挑战。 Pilotfish 于 2020 年推出的“ei Console for X12”就是医疗保健 EDI 技术进步的例子之一。 Pilotfish 是唯一能够验证医疗保健 X12 EDI 数据、转换数据并从任何其他应用程序映射数据的解决方案,通过降低复杂性来提供功能和模块。此外,X12 EDI 的“eiConsole”包括一个 EDI 格式生成器,可为 EDI 事务加载丰富的数据字典,例如字段级文档和友好的源名称。此外,在 eiConsole 中,EDI 格式读取器提供自动价格并读取 X12 交易。

2022 年 9 月,Prodigo Solutions 宣布为利用供应链现代化计划的医疗保健客户发布下一代 EDI 平台“Xchange”并使交易流程自动化。下一代 Xchange 的处理时间明显加快,内存占用较小,可支持贸易伙伴之间传输的 EDI 文档量不断增加。因此,随着医疗保健 EDI 功能的技术进步,医疗保健行业的整体运营效率可能会提高,这将促进 2022-2030 年的市场增长。

报告细分和范围

组件-基于见解

根据组件,医疗保健 EDI 市场分为解决方案和服务。 2022 年,解决方案领域占据了更大的市场份额,预计 2022 年至 2030 年市场复合年增长率将达到 14.9%。电子数据交换 (EDI) 解决方案包括可读格式的数据转换、互操作性、IT 工具和数据安全。例如,当前版本的 EDI 解决方案包括标准化消息传递,以实现医疗保健组织内的无缝信息交换。此外,IBM 等顶级公司还提供“IBM WebSphere Data Interchange”解决方案,支持面向服务的架构 (SOA) 和业务流程管理 (BPM) 的实施。此外,“IBM WebSphere Data Interchange”解决方案还有助于创建、部署、执行和管理基于标准的 EDI 格式与内部应用程序数据格式之间的数据转换以及相关的基于标准的处理。 IBM WebSphere Data Interchange 用于多个行业,包括医疗保健行业。上述因素是影响该细分市场增长的因素。

基于交付模式的见解

根据交付模式,医疗保健 EDI 市场分为基于网络和基于云的 EDI 增值网络 (VAN) 、直接/点对点 EDI、移动 EDI 等。基于网络和基于云的细分市场在 2022 年占据最大的市场份额,预计 2022 年至 2030 年复合年增长率最高,为 15.2%。基于网络的 EDI 通过互联网浏览器进行 EDI,并以网络格式复制纸质文档。该表单包含用户需要填写信息的字段。添加相关信息后,它会自动转换为 EDI 消息,并通过安全互联网协议(例如安全文件传输协议 (FTPS) 和安全超文本传输协议 (HTTPS) 或 AS2)发送。 Web EDI 是中小型企业可以采用的最简单的技术形式,通过浏览器创建、接收、周转和管理电子文档。

同样,基于云的 EDI 解决方案提供了丰厚的优势,例如灵活性和可扩展性。可扩展性、成本效益和云计算优势。例如,由于提高了公司运营的敏捷性和 IT 灵活性,GE Healthcare 等大型医疗保健公司正在将重点从传统的数据交换平台转向基于云的 EDI。此外,云 EDI 软件提供了技术和业务流程改进的组合,旨在满足组织的需求。从数据转换功能到简化自动化,云 EDI 使企业能够应对任何集成挑战,而无需部署和管理软件和硬件。

基于应用程序的见解

在应用程序方面,医疗保健 EDI 市场分为理赔管理和医疗保健供应链。理赔管理细分市场将在 2022 年占据更大的市场份额,预计 2022 年至 2030 年复合年增长率将达到 14.6%。

EDI 是整个医疗保健行业常规使用的标准,允许付款人和医疗保健专业人员发送更快地接收索赔相关信息,避免延误并减少管理费用。 EDI 对医疗保健索赔管理的好处如下:

在供应商、清算所和付款人级别自动检查电子索赔是否符合 HIPAA 和付款人特定要求。此类电子索赔减少了索赔被拒绝的数量,并且通过 EDI 生成的相同水平的自动化数据无法在纸质索赔上执行。EDI 减少了呼叫时间,获取有关会员的信息,并通过经过验证的授权处理索赔相关的付款。例如, XactAnalysis 不断监控数据以识别错误、跟踪进度、基准性能,以减少索赔成本和错误,并提高医疗保健索赔结算的精确速度。此外,XactAnalysis 还提供实时质量保证和审核工具、批量作业导入、估算审核、显示绩效记分卡、作业网络等。

基于最终用户的见解

亚太地区医疗保健电子数据交换( EDI)市场按最终用户划分为医疗保健提供者、医疗保健付款人、医疗和制药行业以及药房。医疗保健提供商细分市场在 2022 年占据最大的市场份额,预计 2022 年至 2030 年复合年增长率最高,达到 14.7%。医疗保健提供商需要一套广泛的工具来推动临床、财务和运营的成功。 “Oracle Health”就是这样一个例子,它致力于简化临床和运营工作流程,以提高门诊诊所和门诊手术中心 (ASC) 的生产力和结果。以下案例研究很好地理解了这一点:明尼苏达州儿童医院与 Oracle Health 合作,最大限度地提高效率并支持优质护理。此外,明尼苏达州儿童医院能够利用 Cerner 的新 ED LaunchPoint 产品简化现成护理服务或紧急护理。该产品提供了当前患者就诊和操作的直接可见性,以及只需单击一下即可查看患者摘要视图。此外,为了支持所有患者就诊类型的移动性,Cerner 在明尼苏达州儿童医院的初级护理中推出了“PowerChart Touch”。例如,“PowerChart Touch”支持提供商在智能手机或平板电脑上的移动性,允许提供商查看图表、拍照以方便数据/报告传输,并使用内置听写软件进行记录。提供商为医疗保健组织高效、平稳运作而推出的此类创新产品促进了整体市场增长。

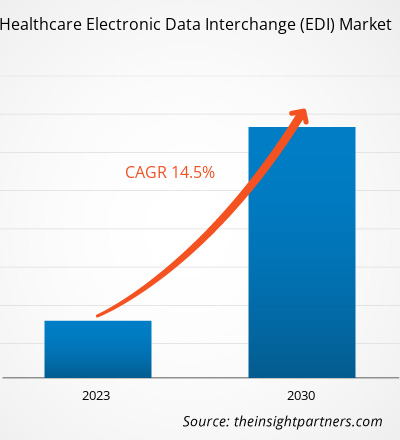

医疗保健 EDI 市场,按组成部分 – 2022 年和 2030 年

区域分析

亚太医疗保健EDI 市场分为中国、印度、日本、韩国、澳大利亚和亚太地区其他地区。中国占据医疗保健 EDI 市场的最大份额。根据美国国立卫生研究院(NIH)的报告,中国已经意识到采用电子数据交换(EDI)的好处。例如,医疗保健领域的数据治理系统寻求平衡和共享健康数据。此外,监管需求也很重要,因为会产生大量健康数据。为此,中国卫生部计划于2023年10月实施重大工程“中国金健康医疗网工程”,建立卫星传输的全国医疗卫生通信网络。该项目将推出金健康卡,这是一种内置芯片的智能卡,可以保存患者的财务和医疗信息,帮助患者从不同地理位置的医院获得适当的医疗服务。在同一项目下,医院已开始使用 EDI 与其他医院、医疗资源供应商、保险公司和银行进行通信。

EDI 服务首先在北京医院开展,以推广 EDI 在中国医疗机构的使用。北京被选为实施EDI的研究地点,因为它是中国的首都,也是工业化程度最高的城市之一。此外,北京的许多组织都拥有发达的IT基础设施。因此,北京的医院更多地得到政府和各行业组织的帮助,在医院实施EDI。 EDI涌入中国医院使三级及以下医院发生了显着变化。例如,门诊挂号费由中国的医疗政策决定,三级及以下医院的挂号费差异约为100%。 0.2 美元。由于差异如此之小,许多患者愿意花更多钱去服务更好的中国三级医院。因此,中国一级、二级医院门诊就诊人数较少,三级医院排队等候时间较长。由于三级医院排队等候时间较长,更有可能采用IT基础设施来保持竞争力。然而,对于低级别医院来说,吸引病人是一个关键问题,他们更愿意投资于营销而不是IT。因此,EDI的实施对于三级和低级别医院来说都具有IT和营销方面的优势。因此,EDI 提供的这些显着功能有助于中国的医疗保健系统占据市场主导地位。

- Historical Analysis (2 Years), Base Year, Forecast (7 Years) with CAGR

- PEST and SWOT Analysis

- Market Size Value / Volume - Global, Regional, Country

- Industry and Competitive Landscape

- Excel Dataset

- Airport Runway FOD Detection Systems Market

- Collagen Peptides Market

- Toothpaste Market

- Intraoperative Neuromonitoring Market

- Sexual Wellness Market

- Foot Orthotic Insoles Market

- Legal Case Management Software Market

- Maritime Analytics Market

- Hydrogen Storage Alloys Market

- Space Situational Awareness (SSA) Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

Frequently Asked Questions

The healthcare EDI market majorly consists of the players such Siemens Healthineers AG, GE HealthCare Technologies Inc, Wipro Ltd, athenahealth Inc, PNORS Technology Group Pty Ltd, International Business Machines Corp, Cognizant Technology Solutions Corp, Veradigm Inc, Oracle Corp, McKesson Corp, and Optum Inc.

The healthcare providers segment dominated the healthcare EDI market and held the largest market share in 2022.

Electronic data interchange (EDI) in healthcare is a secure way of transmitting data between healthcare institutions, insurers, and patients using established message formats and standards.

The CAGR value of the healthcare EDI market during the forecasted period of 2020-2030 is 14.5%.

The solution segment held the largest share of the market in the healthcare EDI market and held the largest market share in 2022.

Siemens Healthineers and GE HealthCare Technologies Inc are the top two companies that hold huge market shares in the healthcare EDI market.

Trends and growth analysis reports related to Technology, Media and Telecommunications : READ MORE..

The List of Companies - Asia Pacific Healthcare EDI Market

- Siemens Healthineers AG

- GE HealthCare Technologies Inc

- Wipro Ltd

- athenahealth Inc

- PNORS Technology Group Pty Ltd

- International Business Machines Corp

- Cognizant Technology Solutions Corp

- Veradigm Inc

- Oracle Corp

- McKesson Corp

- Optum Inc

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Get Free Sample For

Get Free Sample For