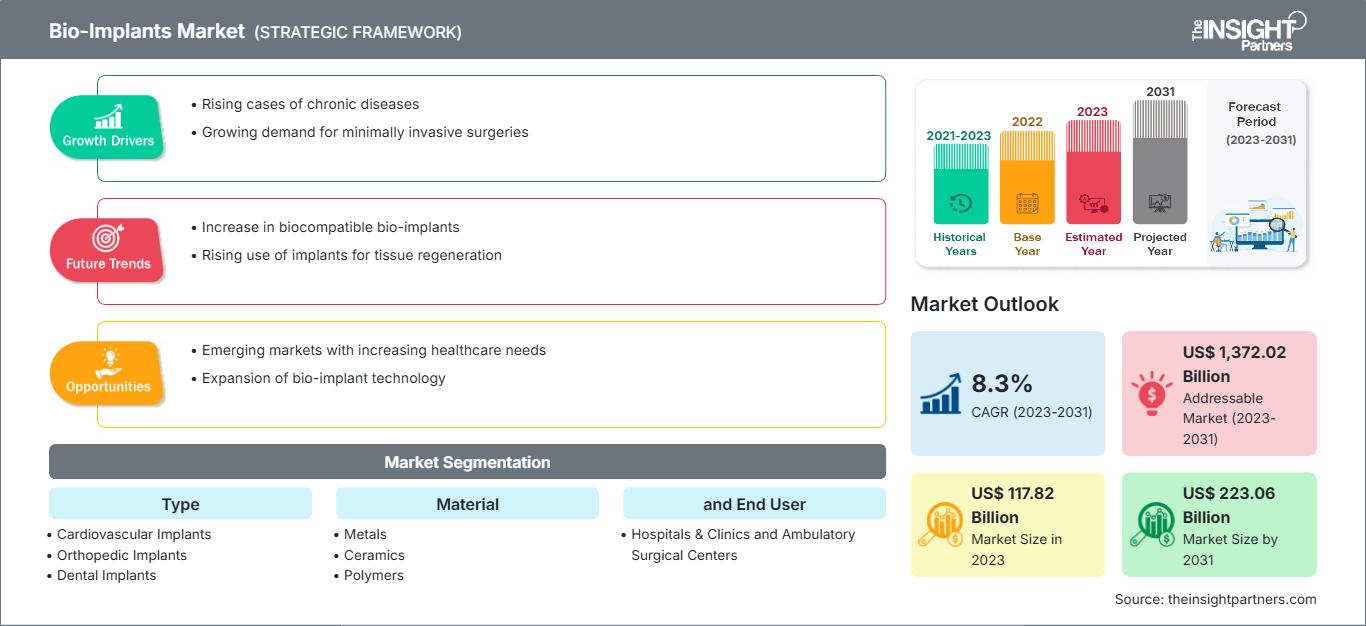

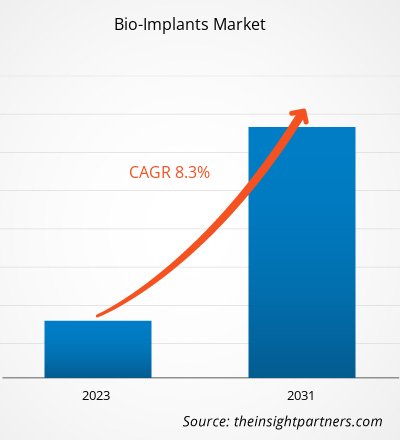

预计到2031年,生物植入物市场规模将达到2.79亿美元。预计2025年至2031年期间,该市场将以7.3%的复合年增长率增长。

分析师观点:

该报告分析了当前生物植入物市场趋势及驱动因素,并展望了其增长前景。推动生物植入物市场规模增长的主要因素包括慢性病病例的增加(尤其是在老年人群中)以及可支配收入的提高。发达国家和发展中国家的医疗基础设施预计将进一步改善,从而显著推动生物植入物市场的发展。

全球范围内,人们对美容植入物的有效性和技术进步的认知度不断提高。由于牙科疾病病例的增加,生物植入物市场在全球范围内持续增长。同时,心血管和骨科疾病发病率的上升也带动了对骨科植入物和心脏起搏器的需求增长。北美地区生物植入物市场的整体销售额预计将持续增长,这得益于该地区完善的医疗基础设施、人们对美容植入物的认知度不断提高,以及该地区生物植入物市场的主要参与者。此外,欧洲是全球第二大生物植入物市场,这主要得益于医疗保健技术的快速发展、对非侵入性生物植入物需求的增长以及老年人口的激增。然而,生物植入手术成本的不断上涨以及生物植入物产品的合理利用不足,阻碍了生物植入物市场的增长。

市场概况:

推动生物植入物市场增长的关键因素包括老年人群骨质疏松症病例的增加、微创手术需求的增长以及生活方式疾病病例的增多。此外,医疗保健领域的技术发展预计将在未来几年对生物植入物市场预测产生重大影响。尽管医疗保健行业近年来取得了显著的技术进步,但严重疾病发病率的上升阻碍了生物植入物市场的发展。

根据您的需求定制此报告

获取免费定制服务生物植入物市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

市场驱动因素:生活方式疾病负担加重推动市场增长

糖尿病、心血管疾病和骨关节炎等生活方式疾病在全球范围内日益普遍,是导致发病率和死亡率的主要原因。支架和支架等生物植入物可以治疗这些疾病,并正成为传统永久性植入物的理想替代方案。根据美国心脏协会2021年发表的一篇文章,美国每年约有4万名儿童接受先天性心脏病手术。英国心脏基金会2022年发布的《2022年1月英国概况介绍》指出,约有760万人患有心脏和循环系统疾病,其中近400万男性和360万女性在2021年患有心脏病和循环系统疾病。因此,心血管疾病患病率的不断上升导致对早期诊断和治疗的需求日益增长,预计这将推动介入心脏病学手术以及心血管生物植入物的需求。此外,口腔健康问题的急剧增加预计也将增加对生物植入物的需求。例如,根据世界卫生组织(世卫组织)2021年全球疾病负担研究,口腔疾病预计将影响全球约一半的人口。约有35.8亿人受到龋齿和其他牙科问题的影响。生物植入物

此外,生物植入物有助于管理和控制特定药物的输送,例如在肌肉骨骼疾病中。根据2021年1月发表在《骨科手术》杂志上的一篇文章,北京社区中年人群腰椎滑脱症的总体患病率为17.26%(男性为15.98%,女性为18.80%)。60岁及以上的女性更容易患腰椎滑脱症。据世界卫生组织统计,肌肉骨骼损伤和疾病十分普遍,影响着全球17.1亿人,是全球致残的主要原因。根据发表在《柳叶刀风湿病学》杂志上的一项新研究,预计到2050年,将有超过10亿人患有关节、肌肉、骨骼、韧带、肌腱和脊柱疾病,而2020年这一数字约为5亿。由于人口老龄化加剧,患有肌肉骨骼疾病及相关功能障碍的人数正在迅速增加。患者中肌肉骨骼疾病的日益增多导致对植入手术和住院治疗的需求增加,从而推动了生物植入物市场的发展。

细分市场分析:

生物植入物市场分析是通过考虑以下几个方面进行的:类型、材料和最终用户。

根据类型,生物植入物市场可分为心血管植入物、骨科植入物、牙科植入物、眼科植入物和其他植入物。2023年,心血管植入物市场份额最大。该细分市场的增长主要得益于新型心脏植入产品研发活动的快速发展。例如,2022年2月,医疗技术公司雅培宣布,作为其AVEIR DR i2i关键性临床试验的一部分,全球首例患者成功植入了无导线双腔起搏器系统。雅培的这款实验性双腔无导线起搏器的植入,是无导线起搏器技术领域的一个重要里程碑;它是全球首例进入关键性试验的此类产品。

根据材料的不同,生物植入物市场可分为金属、陶瓷和聚合物三大类。2023年,速释胶囊占据了最大的市场份额,预计在预测期内仍将保持最高的复合年增长率。这些金属材料因其卓越的机械强度、耐腐蚀性和生物相容性,是植入应用的理想选择。钛因其优异的耐久性、轻量化设计和与人体组织的相容性,成为骨科、牙科和心血管植入物中极为流行的材料。金属材料因其延展性、导电性和惰性,在心脏电极和神经探针等特殊植入应用中备受青睐。慢性疾病发病率的上升以及材料科学和制造技术的进步,推动了生物植入物对生物材料金属的需求。这巩固了生物材料金属作为生物植入物市场中最受欢迎的材料类别的地位。

根据最终用户,生物植入物市场可分为医院和诊所以及门诊手术中心两大板块。2023年,医院和诊所板块占据了生物植入物市场更大的份额,预计在2023年至2031年期间,其复合年增长率(CAGR)将更高。医院和诊所通常拥有庞大的患者群体,其中包括需要特殊植入物治疗的患者,这得益于其完善的医疗体系和多学科的患者护理模式。医院通常与研究中心和医疗器械制造商合作,以促进获取尖端植入物突破性技术。医院和诊所是生物植入物市场的重要参与者,因为它们提供必要的植入物相关服务,并对生物植入物相关的产品和流程产生显著需求。因此,随着人们对药物需求的不断增长,医院和诊所数量的增加预计将在预测期内推动该板块市场的增长。

区域分析:

生物植入物市场报告涵盖北美、欧洲、亚太、中东和非洲以及南美和中美洲。2023年北美市场规模为505.1亿美元,预计到2031年将达到966.9亿美元,2023年至2031年间的复合年增长率预计为8.5%。北美市场分为美国、加拿大和墨西哥三个部分。北美市场的增长归因于慢性病患病率的上升和医疗基础设施的改善。2022年7月,美国疾病控制与预防中心(CDC)更新的数据显示,冠状动脉疾病是最常见的心脏病类型之一,美国约有2010万20岁及以上的成年人患有此病。此外,根据CDC的数据,每40秒就有一人发生心脏病发作,即近80.5万人。预计在预测期内,慢性病数量的增加将推高对生物植入物的整体需求。

根据美国医疗保险和医疗补助服务中心(CMS)的数据,预计到2028年,美国医疗保健支出将达到6.2万亿美元,2019年至2028年的年均增长率(AAR)为5.4%。由于预计医疗保健支出将增长1.1个百分点,医疗保健支出占经济的比重预计将在2028年增长19.7%,高于2019年至2028年期间的年均GDP增速。因此,不断增长的医疗保健支出预计将为市场参与者在预测期内开发生物植入物创造机遇。

2023年,欧洲占据全球第二大生物植入物市场份额。该地区市场增长主要归功于医疗保健技术的进步、对非手术生物植入物需求的增加以及老年人口的增长。欧洲市场增长还得益于政府对医疗保健的投入和支持、骨科疾病发病率的上升以及医疗保健领域研发活动的增加。此外,该地区心血管疾病发病率的上升导致心血管手术数量的增加,这也推动了该地区生物植入物市场的发展。

预计2023年至2031年间,亚太地区将在全球生物植入物市场中实现最高的复合年增长率。该地区市场增长主要归因于老年人口的增长、可支配收入的增加、医疗保健投资的增加以及市场参与者的扩张,以及交通事故增多导致的脊髓损伤病例的增加。亚太地区正经历着显著的增长,尤其是在中国和印度等新兴市场。医疗基础设施的扩建和为提供高效的患者服务而增加的投资,推动了该地区生物植入物市场的发展。例如,根据日本庆应义塾大学2019年发布的一份报告,日本约有10万名患者因脊髓损伤而瘫痪。然而,iPS技术的获批有望在不久的将来帮助这些患者,这有望在未来几年为生物植入物市场带来新的机遇。根据联合国亚洲经济社会委员会和太平洋社会发展部的数据,2016年亚洲60岁以上人口占总人口的12.4%以上,预计到2050年底,这一数字将达到13亿。

生物植入物

生物植入物市场区域洞察

The Insight Partners 的分析师对预测期内生物植入物市场的区域趋势和影响因素进行了详尽的阐述。本节还探讨了北美、欧洲、亚太、中东和非洲以及南美和中美洲等地区的生物植入物市场细分和地域分布。

生物植入物市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2024年市场规模 | XX百万美元 |

| 到2031年市场规模 | 2.79亿美元 |

| 全球复合年增长率(2025-2031年) | 7.3% |

| 史料 | 2021-2023 |

| 预测期 | 2025-2031 |

| 涵盖部分 |

按类型

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

生物植入物市场参与者密度:了解其对业务动态的影响

生物植入物市场正快速增长,这主要得益于终端用户需求的不断增长,而终端用户需求的增长又源于消费者偏好的转变、技术的进步以及消费者对产品益处的认知度不断提高。随着需求的增长,企业不断拓展产品和服务,持续创新以满足消费者需求,并把握新兴趋势,这些都进一步推动了市场增长。

- 获取生物植入物市场主要参与者概览

关键球员分析:

LifeNet Health;Smith & Nephew;Arthrex, Inc.;Clinic Lemanic;Alpha Bio Tec;MiMedx Group;Medtronic;St Jude Medical(雅培);Stryker Cooperation;DePuy Synthes;Biomet(Zimmer);Exactech, Inc.;Cochlear Ltd;以及 Straumann AG 等公司是生物植入物市场报告中重点介绍的主要参与者。

最新进展:

在市场上运营的公司会采取并购等方式。根据公司新闻稿,以下是近期一些重要的发展动态:

- 2023年2月,医疗器械开发商CurvaFix公司宣布推出其直径更小的7.5毫米CurvaFix IM植入物,该产品旨在修复弯曲骨骼的骨折。CurvaFix IM植入物旨在简化手术流程,为小骨提供牢固稳定的固定,并适用于骨骼畸形患者。

- 2022 年 6 月,ZimVie 在美国推出了获得美国食品药品监督管理局批准的 T3 专业工程种植体和 Encode Emergence 愈合基台。

- 2021年6月,医疗器械公司Intelligent Implants Ltd.的骨科植入物技术SmartFuse获得美国FDA的突破性专利批准。SmartFuse平台旨在远程刺激、控制和监测骨骼生长,从而为临床决策提供实时支持。该产品适用于首次接受腰椎融合术的患者。

- 2021 年 2 月,美敦力推出了 TYRX 可吸收抗菌鞘,这是一种可吸收的一次性抗菌鞘,旨在稳定心脏植入式电子设备或植入式神经刺激器。

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 生物植入物市场

获取免费样品 - 生物植入物市场