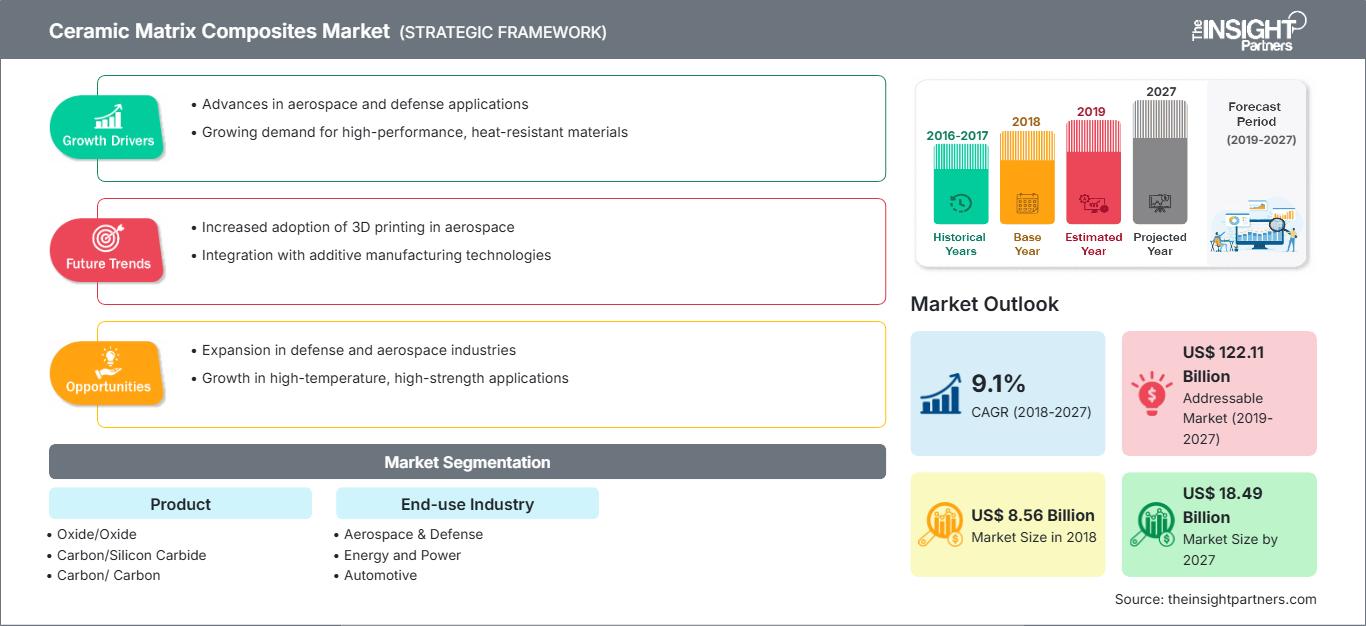

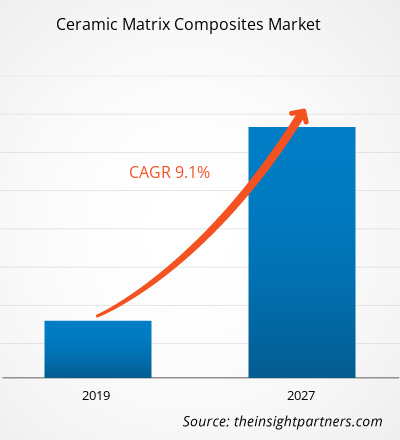

[研究报告] 2018 年陶瓷基复合材料市场规模为 85.6 亿美元,预计在 2019 年至 2027 年预测期内,复合年增长率将达到 9.1%,到 2027 年将达到 184.85 亿美元。

市场分析

陶瓷基复合材料 (CMC) 是指一类将陶瓷纤维或颗粒与陶瓷基体结合在一起以形成高性能复合材料的先进材料。这些复合材料旨在利用增强纤维/颗粒和陶瓷基体的理想特性,以实现与传统陶瓷材料相比更高的机械强度、热稳定性和其他增强特性。陶瓷基复合材料的高耐热性和抗拉强度等机械性能使其成为汽车、国防和航空航天领域的重要组成部分。预计各终端行业应用基础的提升将为陶瓷基复合材料市场的增长提供机遇。

增长动力与挑战

新兴行业对陶瓷基复合材料 (CMC) 的需求不断增长,源于其符合这些行业需求的独特性能。在可再生能源领域,CMC 应用于风力涡轮机和太阳能发电系统,其轻质特性有助于提高能源效率并降低成本。此外,CMC 的高温性能使其适用于聚光太阳能发电厂和地热能系统。在电动汽车行业,CMC 为电池外壳、电机外壳和制动系统等部件提供轻量化和高强度的解决方案,有助于开发更高效、更可持续的电动汽车。CMC 的多功能性使其成为这些新兴行业中极具前景的材料选择,从而推动了陶瓷基复合材料市场的增长。

然而,陶瓷基复合材料 (CMC) 的高成本严重制约了其市场增长。CMC 生产涉及复杂且专业的制造工艺,包括纤维生产、基体制备和复合材料制造,这导致其生产成本高于传统材料。这种成本溢价限制了 CMC 的广泛应用,尤其是在注重成本效益的行业。高成本也给规模较小的制造商或资源有限的公司带来了挑战,因为他们可能难以投资 CMC 生产所需的设备和专业知识。此外,CMC 生产工艺的可扩展性有限,进一步限制了其大规模供应,使潜在用户难以获得和负担得起。因此,CMC 的高成本阻碍了陶瓷基复合材料市场的增长。

自定义此报告以满足您的要求

您将免费获得任何报告的定制,包括本报告的部分内容,或国家级分析、Excel 数据包,以及为初创企业和大学提供超值优惠和折扣

陶瓷基复合材料市场: 战略洞察

- 获取本报告的主要市场趋势。这个免费样本将包括数据分析,从市场趋势到估计和预测。

您将免费获得任何报告的定制,包括本报告的部分内容,或国家级分析、Excel 数据包,以及为初创企业和大学提供超值优惠和折扣

陶瓷基复合材料市场: 战略洞察

- 获取本报告的主要市场趋势。这个免费样本将包括数据分析,从市场趋势到估计和预测。

报告细分和范围

《2027年全球陶瓷基复合材料市场分析》是一项专业且深入的研究,主要关注全球陶瓷基复合材料市场的趋势和增长机遇。本报告旨在概述全球陶瓷基复合材料市场,并按产品、最终用途行业和地域进行详细的市场细分。全球陶瓷基复合材料市场近年来一直保持高速增长,预计在预测期内将继续保持这一趋势。本报告提供了全球陶瓷基复合材料消费量的关键统计数据,以及主要地区和国家的需求。此外,本报告还对影响主要地区和国家陶瓷基复合材料市场表现的各种因素进行了定性评估。本报告还对陶瓷基复合材料市场的主要参与者及其关键战略发展进行了全面分析。本文还包含几项市场动态分析,旨在帮助识别关键驱动因素、市场趋势和利润丰厚的陶瓷基复合材料市场机遇,从而帮助确定主要收入来源。

此外,生态系统分析和波特五力模型分析提供了全球陶瓷基复合材料市场的360度视角,有助于了解整个供应链以及影响市场增长的各种因素。

细分分析

全球陶瓷基复合材料市场根据产品和最终用途行业进行细分。根据产品,陶瓷基复合材料市场细分为氧化物/氧化物、碳化硅/碳化硅、碳/碳化硅和碳/碳。根据最终用途行业,陶瓷基复合材料市场分为航空航天和国防、能源和电力、汽车、工业和其他。

从产品来看,氧化物/氧化物陶瓷基复合材料在2022年占据了相当大的市场份额。氧化物/氧化物陶瓷基复合材料 (CMC) 在推动市场增长方面发挥着重要作用。这些 CMC 具有独特的优势,例如优异的热稳定性、耐高温性和更佳的机械性能。氧化铝 (Al2O3) 和氧化锆 (ZrO2) 等氧化物在这些复合材料中充当陶瓷基体,而氧化铝纤维等氧化物基纤维则增强了结构。氧化物/氧化物 CMC 在航空航天、国防和能源等行业中得到广泛应用,其卓越的热性能和耐用性至关重要。它们用于燃气涡轮发动机的热段、热障涂层以及飞机和太空探索中的高温部件。对能够承受极端温度和恶劣环境的高性能材料的需求日益增长,推动了氧化物/氧化物 CMC 的应用,从而带来了陶瓷基复合材料市场的扩张和增长机会。

区域分析

本报告详细概述了全球陶瓷基复合材料市场,涵盖五大主要区域,即北美、欧洲、亚太地区 (APAC)、中东和非洲 (MEA) 以及南美和中美。北美地区占据陶瓷基复合材料市场主导地位,2022 年市场收入超过 45 亿美元。北美在航空航天、国防和能源等广泛使用陶瓷基复合材料 (CMC) 的关键行业中占有重要地位。这些行业对具有优异性能(包括轻质、高强度和热稳定性)的先进材料有着很高的需求,而 CMC 恰好可以提供这些性能。预计到 2028 年,欧洲陶瓷基复合材料市场收入将超过 73 亿美元。CMC 行业在欧洲经济中占据重要地位,促进了增长、创新和就业。CMC 与国防、航空航天、能源和电力、电气和电子等多个工业领域密切相关。亚太地区陶瓷基复合材料市场预计将以超过10%的复合年增长率显著增长。该地区各国的人口和城镇化进程都在快速增长,这为陶瓷基复合材料市场的主要参与者提供了充足的机遇。

行业发展与未来机遇

合作、收购和新产品发布是全球陶瓷基复合材料市场参与者的主要战略。

- 2019年,西格里碳素公司(SGL Carbon)与Elbe Flugzeugwerke公司续签了合同,将为空客A350客舱地板面板供应浸渍碳纤维纺织品,合同有效期至2020年底。

- 2023年4月,西格里碳素公司宣布与Lancer Systems公司建立新的合作伙伴关系,共同开发用于热防护系统的陶瓷基复合材料。

- 2023年1月,劳斯莱斯与英国谢菲尔德大学签署谅解备忘录,合作开发新型陶瓷基复合材料。

陶瓷基复合材料市场区域洞察

The Insight Partners 的分析师已详尽阐述了预测期内影响陶瓷基复合材料市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的陶瓷基复合材料市场细分和地域分布。

陶瓷基复合材料市场报告范围

| 报告属性 | 细节 |

|---|---|

| 市场规模 2018 | US$ 8.56 Billion |

| 市场规模 2027 | US$ 18.49 Billion |

| 全球复合年增长率 (2018 - 2027) | 9.1% |

| 历史数据 | 2016-2017 |

| 预测期 | 2019-2027 |

| 涵盖的领域 |

By 产品

|

| 覆盖地区和国家 | 北美

|

| 市场领导者和主要公司简介 |

|

陶瓷基复合材料市场参与者的密度:了解其对业务动态的影响

陶瓷基复合材料市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求的驱动因素包括消费者偏好的演变、技术进步以及对产品优势的认知度的提升。随着需求的增长,企业正在扩展产品线,不断创新以满足消费者需求,并抓住新兴趋势,从而进一步推动市场增长。

- 获取 陶瓷基复合材料市场 主要参与者概述

新冠疫情的影响

新冠疫情对陶瓷基复合材料 (CMC) 市场造成了重大冲击,导致市场中断并阻碍了市场增长。疫情引发了广泛的经济不确定性、供应链中断以及各行各业的工业活动减少。许多 CMC 的终端用户行业,例如航空航天、汽车和能源,都面临重大挫折,包括生产停顿、项目延期和投资减少。旅行和贸易限制也影响了全球市场对 CMC 的需求。此外,企业面临的财务困境以及对成本削减措施的关注导致资本支出减少,并对采用 CMC 等先进材料持谨慎态度。尽管随着经济重启和工业活动的恢复,市场预计将逐步复苏,但新冠疫情无疑在短期内阻碍了 CMC 市场的增长轨迹。

竞争格局和主要公司

陶瓷基复合材料市场的一些主要参与者包括 COI Ceramics, Inc.;通用电气公司;Lancer Systems;SGL Carbon;劳斯莱斯公司;CoorsTek, Inc.;Applied Thin Films Inc.;Ultramet;CFCCARBON CO, LTD;以及 Matech 等。

Habi 是一位经验丰富的市场研究分析师,拥有 8 年专注于化学品和材料领域的经验,并在食品饮料和消费品行业拥有丰富的专业知识。他是维什瓦卡玛理工学院 (VIT) 的化学工程师,在工业和特种化学品、油漆和涂料、纸张和包装、润滑剂以及消费品领域拥有深厚的知识。

Habi 的核心能力包括市场规模和预测、竞争对标分析、趋势分析、客户互动、报告撰写和团队协调,这使他能够提供切实可行的见解并支持战略决策。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

近期报告

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 陶瓷基复合材料市场

获取免费样品 - 陶瓷基复合材料市场