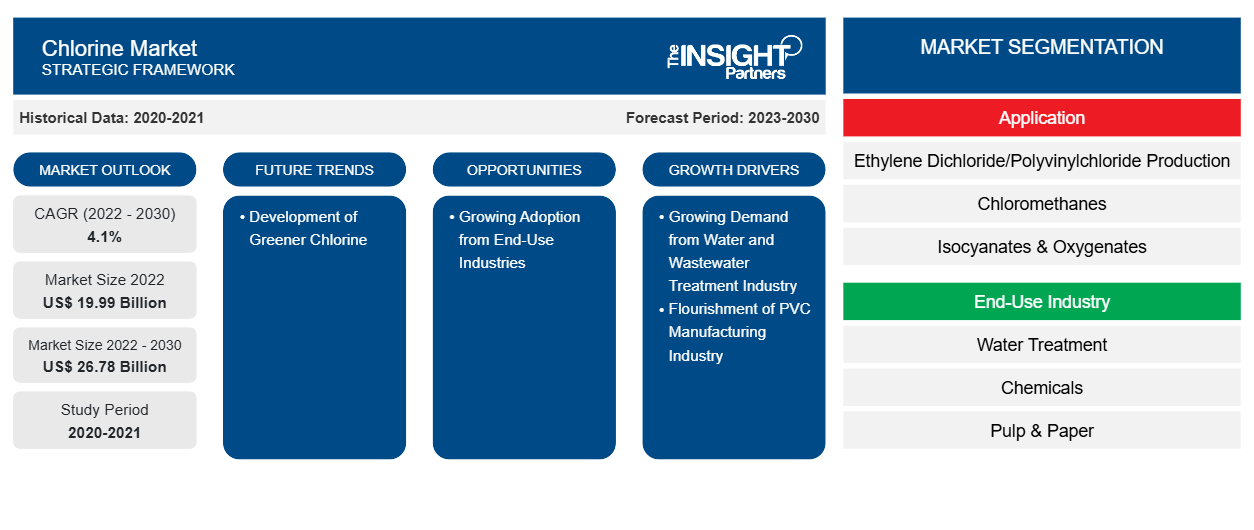

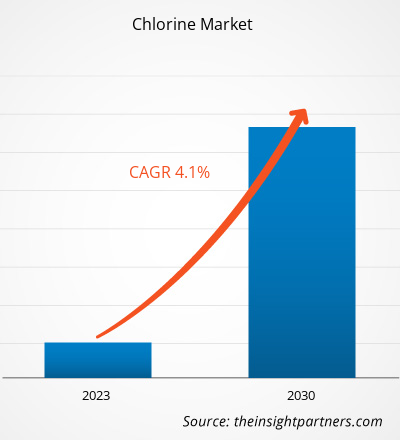

[研究报告] 2022 年氯市场规模价值 199.8892 亿美元,预计到 2030 年将达到 267.7766 亿美元;预计 2022 年至 2030 年的复合年增长率为 4.1%。

市场洞察和分析师观点:

氯是一种用途广泛的化学品,终端用户行业非常广泛,例如水处理、化学品、纸浆和造纸以及塑料。氯是通过使用隔膜电解槽和膜电解槽电解氯化钠溶液而制造的。它是不同行业中各种产品和工艺的必需原材料。氯被广泛用作市政水处理厂的消毒剂,以消灭有害细菌、病毒和其他病原体,确保饮用水的安全和质量。此外,氯是聚氯乙烯 (PVC) 生产的重要组成部分。PVC 用于管道、窗框、地板、包装膜和汽车零部件等应用。制药行业使用氯来合成活性药物成分 (API) 和其他药物化合物。氯用于制造杀虫剂、除草剂和其他农用化学品,以保护农作物并提高农业生产力。它还用于各种化学反应,以生产用于许多工业应用的氯化化合物,例如溶剂、漂白剂和清洁产品。氯在电子制造中用于粘合元件和保护敏感部件。这些因素预计将推动氯市场的增长。

增长动力和挑战:

随着抗生素耐药性细菌的增多和水传播疾病的出现,强大的水消毒方法变得至关重要。除了在去除病原体方面发挥主要作用外,氯还用于水处理以控制藻类和藻类毒素的生长、去除铁和锰以及解决其他水质问题。由于全球人口增长导致用水量增加,以及对确保安全和清洁饮用水消费的需求不断增加,水和废水行业对氯的需求不断增加,推动了氯市场的增长。此外,PVC 薄膜和片材广泛用于包装应用,特别是食品和药品。随着对包装商品的需求不断增加以及对卫生和产品安全的日益关注,对 PVC 基包装材料的需求猛增,进一步促进了 PVC 行业对氯的需求。在电气领域,PVC 电缆和电线因其优异的电气性能和阻燃特性而被广泛用于电气绝缘。随着全球对电力和电力基础设施的需求不断增长,对 PVC 基电气材料的需求不断增长,从而推动了氯的需求。因此,由于 PVC 仍然是建筑、汽车、包装和电气应用中的首选材料,聚合过程中对氯的需求仍然强劲。因此,水处理、PVC 制造和其他终端使用行业不断增长的需求正在推动氯市场的增长。

各行各业和应用对氯的大量生产、处理和处置对人类健康和环境构成潜在风险。世界各国政府已经认识到这些风险,并实施了严格的法规,以确保安全和负责任地使用氯。因此,对氯使用的担忧和控制氯使用的法规不断增加对氯市场的增长产生了负面影响。

定制此报告以满足您的需求

您可以免费定制任何报告,包括本报告的部分内容、国家级分析、Excel 数据包,以及为初创企业和大学提供优惠和折扣

氯市场:

- 获取此报告的关键市场趋势。这个免费样品将包括数据分析,从市场趋势到估计和预测。

报告细分和范围:

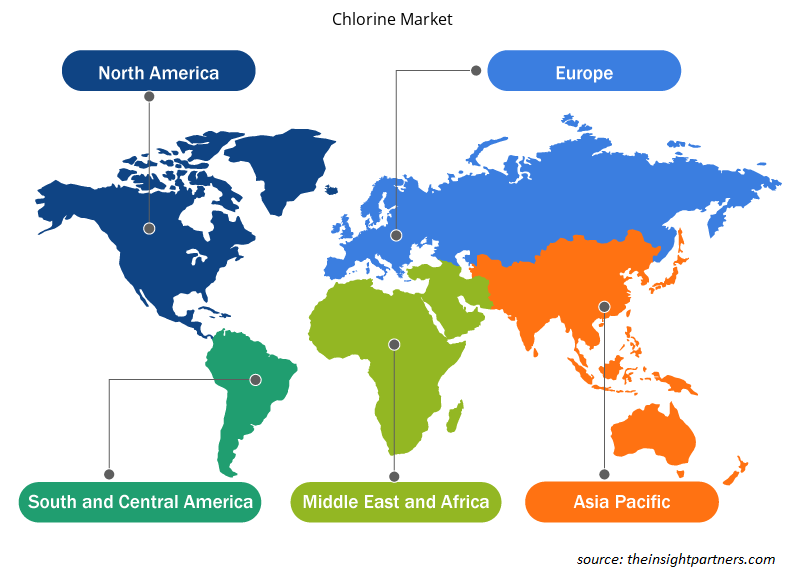

全球氯市场根据应用、最终用途行业和地理区域进行细分。根据应用,氯市场细分为二氯乙烷/聚氯乙烯生产、氯甲烷、异氰酸酯和含氧化合物、溶剂和其他。就最终用途行业而言,氯市场细分为水处理、化学品、纸浆和造纸、塑料、制药和其他。根据地理区域,氯市场细分为北美(美国、加拿大和墨西哥)、欧洲(德国、法国、意大利、英国、俄罗斯和欧洲其他地区)、亚太地区(澳大利亚、中国、日本、印度、韩国和亚太其他地区)、中东和非洲(南非、沙特阿拉伯、阿联酋和中东和非洲其他地区)以及南美洲和中美洲(巴西、阿根廷和南美洲和中美洲其他地区)。

节段分析:

根据应用,氯市场细分为二氯乙烷/聚氯乙烯生产、氯甲烷、异氰酸酯和含氧化合物、溶剂等。异氰酸酯和含氧化合物领域预计将在 2022 年至 2030 年间实现显着增长。异氰酸酯广泛用于生产聚氨酯,聚氨酯是一种用于泡沫、粘合剂、密封剂、涂料和弹性体的多功能材料。这些聚氨酯材料可用于家具、床垫、汽车零件、绝缘材料和鞋类等产品。虽然氯不出现在聚氨酯分子中,但它用于制造中间体异氰酸酯。

含氧化合物是一大类含有氧原子的有机化合物,通常以羟基的形式存在。一些常见的含氧化合物类型是醇(例如乙醇和甲醇)、醚(例如甲基叔丁基醚)和酮(例如丙酮)。含氧化合物在各个行业中作为溶剂、燃料添加剂和化学中间体具有多种应用。例如,乙醇被用作生物燃料添加剂,以减少排放并提高燃料性能。氯在涉及氯化中间体的化学过程中起着至关重要的作用。甲烷的氯化可以产生氯甲烷,氯甲烷经过一系列化学反应生成甲醇。所有这些因素都在推动氯市场中异氰酸酯和含氧化合物部分的增长。

区域分析:

根据地理位置,氯市场分为五个主要区域——北美、欧洲、亚太、南美和中美以及中东和非洲。全球氯市场以亚太地区为主,2022 年该地区的市场规模约为 95 亿美元。该地区已成为全球制造业中心,行业涵盖化学品、纺织、塑料和电子产品。氯是各种工业过程中的关键化学品,例如化学品、溶剂和药品中间体的生产。该地区为满足国内和国际需求而不断增加的制造业活动预计将推动对氯这种重要原材料的需求。因此,随着该地区的发展和工业化,对氯及其衍生物的需求预计将保持强劲,预计将推动亚太地区 2023 年至 2030 年的氯市场增长。预计欧洲在 2023 年至 2030 年的复合年增长率将超过 4%。该地区依赖氯及其衍生物进行各种应用,对这种用途广泛的化学品的需求稳定而持续。欧洲废水处理行业对氯的需求正在增长,原因有几个,这些原因凸显了氯作为关键水消毒剂的重要性。随着欧洲国家努力改善水质、保护公众健康和满足严格的环境法规,氯已成为废水处理的可靠有效解决方案。所有这些因素都在推动欧洲氯市场的增长。北美预计也将出现显着增长,到 2030 年将达到 55 亿美元以上。

行业发展和未来机遇:

以下列出了氯市场主要参与者采取的各种举措:

- 2022 年 12 月,INEOS Enterprises 完成了从 Bigshire Mexico S. de RL de CV 收购 ASHTA Chemicals 的交易,该交易包括一座 100ktpa 氢氧化钾 (KOH)/65 kte 氯气工厂。

- 根据提交给德克萨斯州审计长办公室的文件,2022年4月,西方石油公司化学部门OxyVinyls宣布,计划在其位于德克萨斯州拉波特的氯碱工厂投资 11 亿美元进行扩建和现代化改造项目。

COVID-19 影响:

COVID-19 疫情对各国几乎所有行业都产生了不利影响。北美、欧洲、亚太地区 (APAC)、南美和中美以及中东和非洲 (MEA) 的封锁、旅行限制和企业关闭阻碍了包括化学和材料行业在内的多个行业的增长。氯气公司制造部门的关闭扰乱了全球供应链、制造活动和交付计划。各公司报告称,2020 年产品交付延迟,产品销售下滑。大多数工业制造设施在疫情期间关闭,减少了氯气的消耗。此外,COVID-19 疫情导致氯气价格波动。然而,在供应限制得到解决后,各行业恢复了运营,从而导致氯气市场复苏。此外,工业和住宅部门对氯气的需求不断增长,大大促进了氯气市场的增长。

氯市场区域洞察

Insight Partners 的分析师已详细解释了预测期内影响氯市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的氯市场细分和地理位置。

- 获取氯市场的区域具体数据

氯市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2022 年市场规模 | 199.9 亿美元 |

| 2030 年市场规模 | 267.8亿美元 |

| 全球复合年增长率(2022 - 2030 年) | 4.1% |

| 史料 | 2020-2021 |

| 预测期 | 2023-2030 |

| 涵盖的领域 | 按应用

|

| 覆盖地区和国家 | 北美

|

| 市场领导者和主要公司简介 |

|

市场参与者密度:了解其对商业动态的影响

氯市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求又源于消费者偏好的不断变化、技术进步以及对产品优势的认识不断提高等因素。随着需求的增加,企业正在扩大其产品范围,进行创新以满足消费者的需求,并利用新兴趋势,从而进一步推动市场增长。

市场参与者密度是指在特定市场或行业内运营的企业或公司的分布情况。它表明在给定市场空间中,相对于其规模或总市场价值,有多少竞争对手(市场参与者)存在。

在氯市场运营的主要公司有:

- 印度阿迪亚贝拉化工有限公司

- 巴斯夫

- 埃克罗斯公司

- 韩华解决方案公司

- 英力士集团控股公司

免责声明:上面列出的公司没有按照任何特定顺序排列。

- 了解氯市场主要参与者概况

竞争格局和重点公司:

Aditya Birla Chemicals India Ltd、BASF SE、Ercros SA、Hanwha Solutions Corp、INEOS Group Holdings SA、Occidental Petroleum Corp、Olin Corp、Tata Chemicals Ltd、Vynova Belgium NV 和住友化学有限公司是全球氯气市场的参与者。全球氯气市场参与者专注于提供高质量的产品以满足客户需求。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST 和 SWOT 分析

- 市场规模价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

常见问题

Chlorine is widely used as a disinfectant in municipal water treatment plants to kill harmful bacteria, viruses, and other pathogens, ensuring the safety and quality of drinking water. In addition, chlorine is an important component of polyvinyl chloride (PVC) production. PVC is used in applications such as pipes, window frames, flooring, packaging films, and automotive components. The pharmaceutical industry uses chlorine to synthesize active pharmaceutical ingredients (APIs) and other pharmaceutical compounds. Chlorine is used to manufacture pesticides, herbicides, and other agrochemicals to protect crops and improve agricultural productivity. Growing demand from these end-used industries is driving the demand for chlorine from 2022 to 2030.

The plastics segment held the largest share of the global chlorine market in 2022. The production of PVC involves the polymerization of vinyl chloride monomers, and chlorine is a key raw material in this chemical process. The construction and infrastructure development is growing substantially. PVC pipes, fittings, and profiles are extensively used in construction due to their durability, cost-effectiveness, and versatility. As urbanization continues to accelerate in many parts of the world, the demand for PVC-based construction materials rises in tandem, leading to a higher need for chlorine to meet the polymerization requirements.

Pharmaceutical segment is estimated to register the fastest CAGR in the global chlorine market over the forecast period. Chlorine and chlorine-based compounds play an important role in the pharmaceutical industry, contributing to the synthesis of various medications and pharmaceutical products. Chlorine-containing compounds serve as essential intermediates and reagents in the synthesis of pharmaceutical compounds, enabling the production of a wide range of drugs. Chlorine synthesizes many active pharmaceutical ingredients (APIs), primarily biologically active components in medications. Growing demand for pharmaceuticals is expected to drive the demand for the chlorine from 2022 to 2030.

In 2022, Asia Pacific held the largest share of the global chlorine market. The region has become a global manufacturing hub, with industries spanning chemicals, textiles, plastics, and electronics. Chlorine is a crucial chemical in various industrial processes, such as the production of chemicals, solvents, and intermediates for pharmaceuticals. The rising manufacturing activities across the region to meet domestic and international demands are anticipated to fuel the demand for chlorine, an essential raw material. All these factors led to the dominance of the Asia Pacific region in 2022.

A few players operating in the global chlorine market include Aditya Birla Chemicals India Ltd, BASF SE, Ercros SA, Hanwha Solutions Corp, INEOS Group Holdings SA, Occidental Petroleum Corp, Olin Corp, Tata Chemicals Ltd, Vynova Belgium NV, Sumitomo Chemical Co Ltd.

The isocyanates & oxygenates segment held the largest share in the global chlorine market in 2022. Isocyanates are extensively used in the production of polyurethane, a versatile material used in foams, adhesives, sealants, coatings, and elastomers. These polyurethane materials find applications in items like furniture, mattresses, automotive parts, insulation, and footwear. Thus, growing demand from the application sectors led to the dominance of the isocyanates & oxygenates segment in 2022.

Trends and growth analysis reports related to Chemicals and Materials : READ MORE..

The List of Companies - Chlorine Market

- Aditya Birla Chemicals India Ltd

- BASF SE

- Ercros SA

- Hanwha Solutions Corp

- INEOS Group Holdings SA

- Occidental Petroleum Corp

- Olin Corp

- Tata Chemicals Ltd

- Vynova Belgium NV

- Sumitomo Chemical Co Ltd

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

获取此报告的免费样本

获取此报告的免费样本