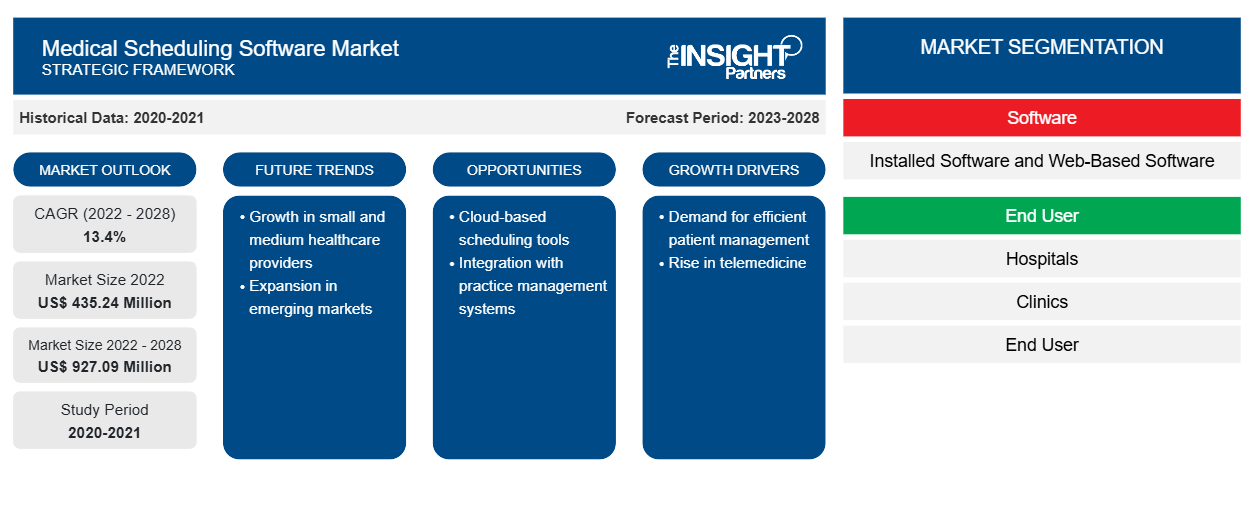

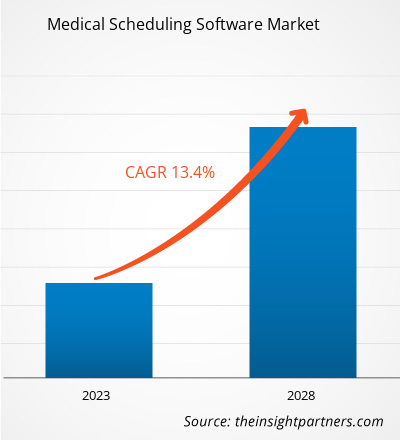

医疗调度软件市场规模预计将从 2022 年的 4.3524 亿美元增至 2028 年的 9.2709 亿美元;预计 2022 年至 2028 年的复合年增长率为 13.4%。

医疗预约软件允许患者在离开医院或诊所时通过在线预约。该诊所采用集成患者门户和预约软件的综合系统。医疗预约软件的常见功能包括患者登记、预约提醒服务、可自定义设置和患者跟踪。该软件经济高效,因此受到越来越多人的青睐。

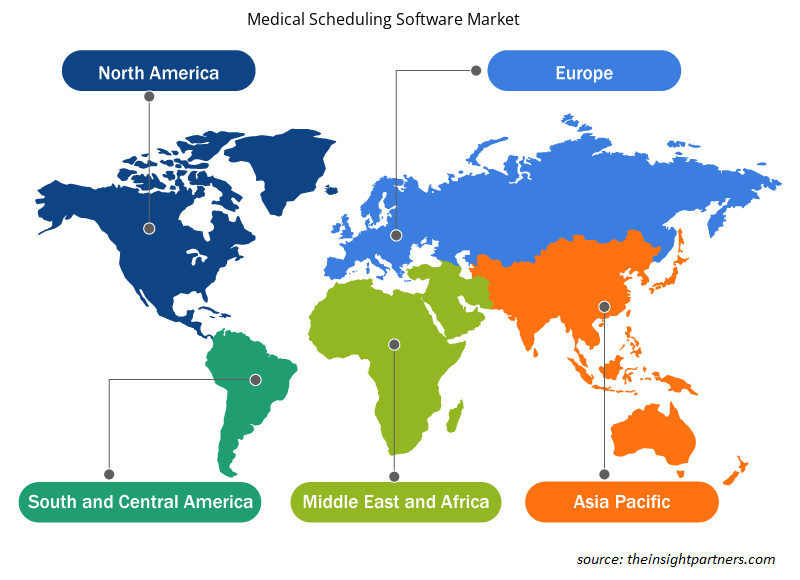

医疗调度软件市场根据软件、最终用户和地理位置进行细分。按地理位置划分,市场大致分为北美、欧洲、亚太地区、中东和非洲以及南美和中美洲。该报告对医疗调度软件市场进行了深入分析,重点关注市场趋势、技术进步和市场动态等参数,并分析了世界主要市场参与者的竞争格局。

市场洞察

医疗服务提供商越来越多地采用以患者为中心的方法

以患者为中心的方法是医疗保健系统中的一种理念,它可以在患者及其家属和医疗保健从业者之间建立合作关系,使决策与患者的需求、偏好和愿望保持一致。它还包括为患者提供做出某些决定和参与护理所需的特定教育和支持。

定制此报告以满足您的需求

您可以免费定制任何报告,包括本报告的部分内容、国家级分析、Excel 数据包,以及为初创企业和大学提供优惠和折扣

医疗调度软件市场:

- 获取此报告的关键市场趋势。这个免费样品将包括数据分析,从市场趋势到估计和预测。

增加与所有利益相关者(医疗服务提供者、患者和其他人员)的互动,从而降低总体费用。提高患者对其健康、福祉和医疗保健选择的知识和理解,从而改善护理并降低患病率。这种知识的提高还可以改善出院后的护理、医院就诊、减少再入院和二次咨询。通过与患者一起参与决策并与他们合作,医疗服务提供者可以就患者的健康做出更合适的决定。随着越来越多的医院在护理质量和成本方面争夺患者,竞争优势增强。患者生活质量的提高会提高医生和患者的满意度。

近年来,以患者为中心的方法在医疗保健行业占据主导地位。技术创新和软件开发对这场医疗保健行业革命至关重要。这些技术发展支持医疗和管理服务,极大地增强和简化了医疗保健流程、通信和工作流程。以患者为中心的医疗保健提高了患者的满意度,为医疗保健提供者和实践带来了好处。因此,医疗保健提供者越来越多地采用以患者为中心的方法,推动了医疗调度软件市场的增长。

增加对物联网的了解

2011 年至 2020 年期间,连接到互联网的设备数量比以往任何时候都多,而且这种趋势在未来几十年也仍将持续稳定。物联网 (IoT) 的出现推动了旨在改善人口健康的各种健康实践的发展。最近的几项研究已经检验了物联网在医疗保健领域的许多服务和应用,包括电子健康、移动医疗 (mHealth)、环境辅助生活、语义设备、可穿戴设备和智能手机以及社区医疗保健。这些服务具有广泛的信息量,可用于单一疾病和集群疾病管理的各种目的,包括允许医疗保健专业人员远程跟踪和监控患者进展、改善慢性病的自我管理、协助及早发现异常、加快症状识别和临床诊断。此外,基于物联网的应用程序有可能更好地利用医疗资源,同时提供高质量、低成本的医疗服务。

进一步的人工智能 (AI) 提高了即时医疗信息的可用性;例如,聊天机器人(也称为 AI 医生)可以提供生活方式和医疗建议。Woebot、Your. Md、Babylon 和 HealthTap 是其他知名 AI 机器人的例子,它们根据患者输入的详细信息/症状向患者提供即时建议。

医疗保健行业物联网创新的机会不断涌现和发展。医疗机构面临着特殊的挑战,物联网供应商正在开发新方法来应对这些挑战。

移动医疗技术的接受度不断提高

移动技术的进步,加上日益增长的健康问题,推动了全球移动医疗服务 (MHS) 的增长。移动和无线技术有可能改变医疗保健的提供方式。移动技术和应用的快速发展、将移动医疗融入现有电子医疗服务的新机会的增加以及移动蜂窝网络覆盖范围的不断扩大,是支持移动医疗解决方案普及的主要因素。根据国际电信联盟 (ITU) 的估计,2020 年无线用户超过 50 亿,其中 70% 以上生活在中低收入国家。根据 GSM 协会的数据,商业无线传输已覆盖全球约 85% 的人口,远远超出了电网的覆盖范围。无线通信的普及不仅有助于提高护理质量和患者的健康,而且每年还可以通过帮助解决处方药质量低劣的问题来节省大量不必要的医疗费用。移动医疗的应用在未来几年可能会扩大。随着糖尿病在美国越来越普遍,移动医疗应用在糖尿病护理和预防方面的潜力将成为移动医疗应用开发商最重要的领域之一。例如,英国国家医疗服务体系 (NHS) 推出了测试平台计划,让 1 型或 2 型糖尿病患者尝试使用健康技术,让他们可以待在家里自行管理病情。这有助于患者减少住院产生的额外费用。此外,除了互联网连通性改善之外,互联网成本的降低(尤其是在发展中国家)也是推动移动医疗应用普及的主要因素。

下面提到了各种其他下一代健康应用程序:

- Mobile MIM 应用程序是 Apple App Store 中的第一款医疗应用程序。它用于查看、注册、融合和显示 SPECT、PET、CT、MRI、X 射线和超声波检查的医学图像,以用于诊断目的。Mobile MIM 通过提供无线和便携式医学图像访问,增强了医生对图片的访问,并允许他们与同行进行咨询。

- WellDoc Inc. 开发了 BlueStar 糖尿病应用程序,该应用程序通过记录血糖数据来工作;它还提供实时指导。WellDoc 的系统拥有超过 20,000 条自动指导信息,可分析数据并提供量身定制的指导,帮助患者管理药物和治疗。

新的 Welch Allyn iExaminer 应用程序将 PanOptic 检眼镜转变为移动数字成像设备,让用户可以观察眼睛。这些产品的发明是为了简化视网膜脱离和青光眼等疾病的检测。适配器允许 PanOptic 检眼镜的光学访问 iPhone 相机的视轴,使其能够捕捉眼底和视网膜神经的高分辨率图像。

医疗调度软件市场 - 最终用户洞察

根据最终用户,全球医疗调度软件市场分为医院、诊所和其他。医院部门在 2021 年占据了最大的市场份额,预计在预测期内将以最高的复合年增长率增长。患者主要喜欢在医院寻求心脏病科、儿科、肺科、精神病科和内科等各种医学专科的治疗。医院是患者进行诊断、治疗和其他医疗保健服务的主要场所。许多患者因外科手术而入院,而一些患者则因诊断而入院。大多数住院患者已经患有各种传染病和慢性病。医院是人民的主要医疗保健中心,这可能会推动该部门的医疗调度软件市场增长。

此外,心血管疾病、癌症和慢性病等慢性疾病的发病率不断上升,也刺激了对用于管理医院患者就诊的医疗调度软件的需求。根据世界卫生组织的数据,心血管疾病 (CVD) 是全球死亡的主要原因,每年导致 1790 万人死亡。此外,根据世界卫生组织的数据,癌症是全球常见的死亡原因之一,预计到 2030 年新发病例数将大幅增加。每年约有 40 万名儿童患上癌症。因此,全球癌症发病率的上升、医院数量的增加以及各种心血管疾病手术的增加,增加了对有效管理患者流量的技术的需求,预计这将在预测期内推动医疗调度软件市场对医院部门的需求。

产品发布和并购是全球医疗调度软件市场参与者广泛采用的策略。以下列出了一些近期的关键产品开发:

- 2022 年 2 月,Daw Systems, Inc. 宣布其荣获 2021 年 Surescripts 白大褂最高精度奖。Daw Systems, Inc. 的核心产品 ScriptSure Cloud ERX v2.0 整合了 Surescripts 网络的广泛功能,使医疗专业人员能够以电子方式将处方发送到药房。

- 2022 年 9 月,Upland Software 和 HP Inc. 计划将 Upland 的 Document Workflow Cloud 解决方案引入 HP Workpath,这是他们持续努力实现纸质和数字之间信息流现代化的一部分。新产品预计将于 2020 年底发布,是一个完整的端到端统一的基于云的工作流平台,用于文档捕获、图像处理和数据提取。

COVID-19 疫情导致全球供应链和需求链中断,导致封锁初期医疗行业的销售额下降。然而,由于社交距离和医院紧急预约等限制,医疗调度软件市场在疫情期间出现了增长。由于医疗机构对更好的管理系统的需求不断增长,以及向基于互联网的平台的转变日益增加,COVID-19 疫情对医疗调度软件市场产生了积极影响。由于需求不断增长,预计医疗 IT 市场将在后 COVID-19 时代健康发展。

医疗排程软件市场 - 细分

根据软件,市场分为基于网络的软件和安装的软件。根据最终用户,市场分为医院、诊所和最终用户。根据地理位置,市场分为北美(美国、加拿大、墨西哥)、欧洲(法国、德国、英国、意大利、西班牙和欧洲其他地区)、亚太地区(中国、日本、印度、澳大利亚、韩国和亚太其他地区)、中东和非洲(沙特阿拉伯、南非、阿联酋和中东和非洲其他地区)、南美洲和中美洲(巴西、阿根廷和南美洲和中美洲其他地区)

医疗调度软件市场区域洞察

Insight Partners 的分析师已详尽解释了预测期内影响医疗排程软件市场的区域趋势和因素。本节还讨论了北美、欧洲、亚太地区、中东和非洲以及南美和中美洲的医疗排程软件市场细分和地理位置。

- 获取医疗调度软件市场的区域特定数据

医疗调度软件市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2022 年市场规模 | 4.3524亿美元 |

| 2028 年市场规模 | 9.2709亿美元 |

| 全球复合年增长率(2022 - 2028) | 13.4% |

| 史料 | 2020-2021 |

| 预测期 | 2023-2028 |

| 涵盖的领域 | 按软件

|

| 覆盖地区和国家 | 北美

|

| 市场领导者和主要公司简介 |

|

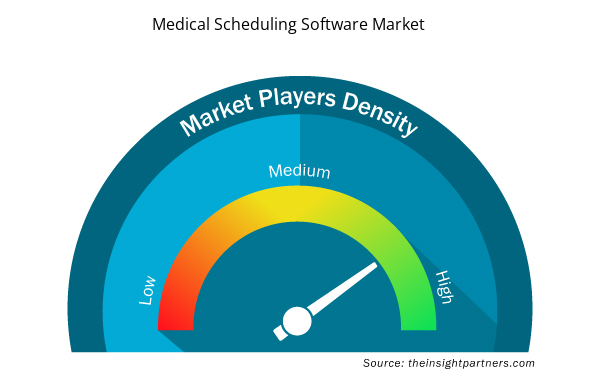

医疗调度软件市场参与者密度:了解其对业务动态的影响

医疗排程软件市场正在快速增长,这得益于终端用户需求的不断增长,而这些需求又源于消费者偏好的不断变化、技术进步以及对产品优势的认识不断提高等因素。随着需求的增加,企业正在扩大其产品范围,进行创新以满足消费者的需求,并利用新兴趋势,从而进一步推动市场增长。

市场参与者密度是指在特定市场或行业内运营的企业或公司的分布情况。它表明相对于给定市场空间的规模或总市场价值,有多少竞争对手(市场参与者)存在于该市场空间中。

在医疗调度软件市场运营的主要公司有:

- 时间交易

- AdvanceMD 公司

- 优卡利网络公司

- 语音通讯公司

- WellSky、Daw Systems, Inc.

免责声明:上面列出的公司没有按照任何特定顺序排列。

- 获取医疗调度软件市场顶级关键参与者概述

医疗调度软件市场 - 公司简介

- TimeTrade,AdvanceMD,Inc.

- 优卡利网络公司

- 语音通讯公司

- 威斯凯

- Daw 系统公司

- ByteBloc 软件

- 工作路径

- 三角洲健康技术公司

- 国土安全部全球

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST 和 SWOT 分析

- 市场规模价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

常见问题

Based on end user, the global medical scheduling software market is divided into hospitals, clinics, and others. The hospitals segment held the largest share of the market in 2021 and is expected to grow at the highest CAGR during the forecast period.

TimeTrade, AdvanceMD, Inc., Yocale Network Corporation, Voicent Communications Inc., WellSky, Daw Systems, Inc., ByteBloc Software, Workpath, Delta Health Technologies, Inc., and DHS Worldwide among others are among the leading companies operating in the medical scheduling software market.

Based on software segment, the web-based segment took the forefront leaders in the worldwide market by accounting largest share in 2022 and is expected to continue to do so till the forecast period.

Medical scheduling software allows patients to schedule their appointments through online when they are away from the hospitals or clinics. The practice employs the comprehensive system with an integrated patient portal and scheduling software. Common features of a medical scheduling software include, patient registration, appointment reminder services, customizable settings, and patient tracking. The economic and efficient handling of the software has led to increased preference of the software.

Rising adoption of patient-centric approach by healthcare providers, surge in use of smart devices for monitoring health, and shortage of nursing staff and doctors are among the key forces driving the overall market growth.

Trends and growth analysis reports related to Technology, Media and Telecommunications : READ MORE..

The List of Companies - Medical Scheduling Software Market

- TimeTrade

- AdvanceMD, Inc.

- Yocale Network Corporation

- Voicent Communications Inc.

- WellSky, Daw Systems, Inc.

- ByteBloc Software

- Workpath

- Delta Health Technologies, Inc.

- DHS Worldwide

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

获取此报告的免费样本

获取此报告的免费样本