肿瘤生物仿制药市场战略、顶级参与者、增长机会、2031 年分析和预测

历史数据 : 2021-2023 | 基准年 : 2024 | 预测期 : 2025-2031肿瘤生物类似药市场规模及预测(2021-2031 年)、全球及区域份额、趋势及增长机会分析报告涵盖范围:按药物类别(单克隆抗体、粒细胞集落刺激因子和促红细胞生成剂)、癌症类型(结直肠癌、宫颈癌、乳腺癌、支持治疗、淋巴瘤及其他)和分销渠道(医院药房、零售药房和在线药房)划分。

- 状态 : 数据发布

- 报告代码 : TIPRE00002766

- 类别 : 生命科学

- 页数 : 150

- 可用报告格式 :

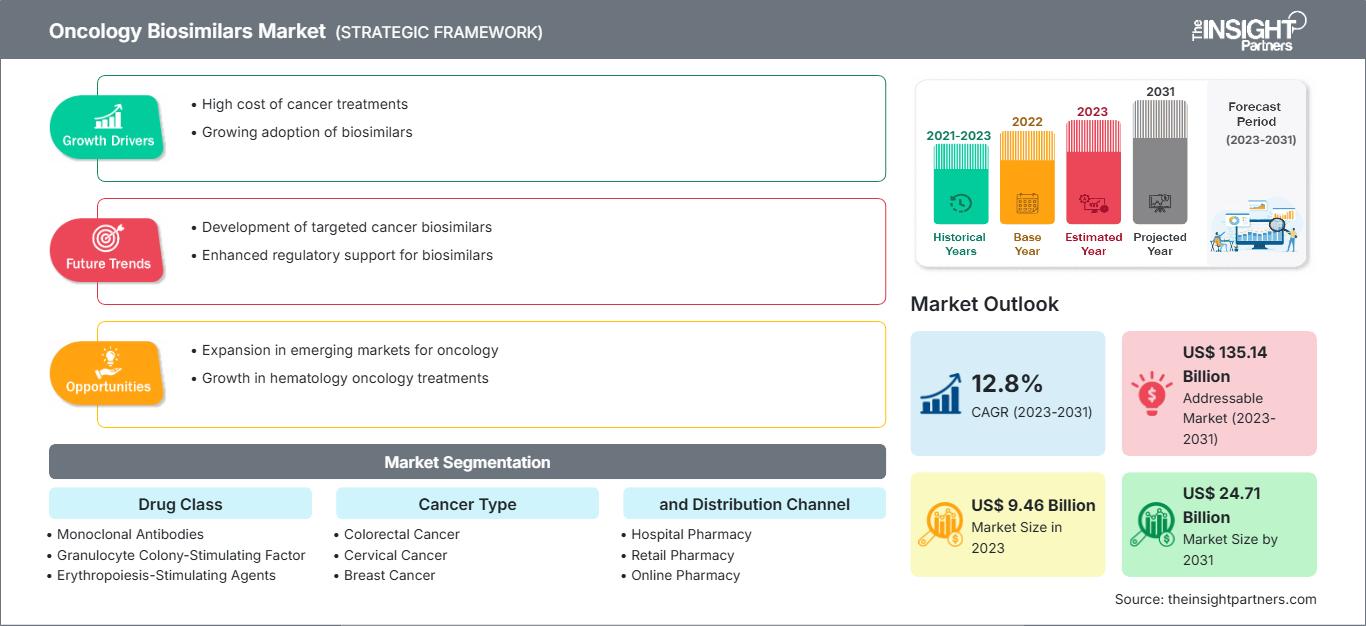

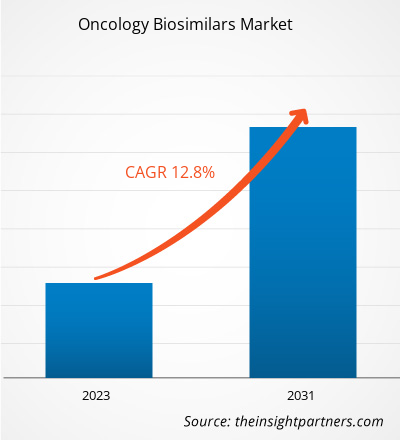

预计到 2031 年,肿瘤生物类似药市场规模将达到 266.18 亿美元。预计该市场在 2025 年至 2031 年期间的复合年增长率将达到 16.3%。

市场洞察与分析师观点:

生物类似药是指在安全性、有效性和质量方面与现有参考生物药高度相似但并非完全相同的生物制药产品。生物类似药包括单克隆抗体和辅助药物,例如非格司亭、培非格司亭、促红素α和促红素ζ,可用于治疗多种癌症。癌症发病率的激增、生物类似药的成本效益以及肿瘤生物类似药获批数量的增加等因素,预计将推动生物类似药市场的发展。此外,生物类似药生产商之间的合作以及临床试验有望在未来几年带来新的肿瘤生物类似药市场趋势。然而,生物类似药生产成本高昂且工艺复杂,是阻碍市场发展的因素之一。

肿瘤生物类似药市场规模及份额——市场驱动因素:

根据世界卫生组织(世卫组织)的数据,2022年全球报告了约2000万例新增癌症病例和970万例癌症死亡病例。此外,世卫组织全球癌症观察站的最新估计显示,2022年,全球新增癌症病例和死亡病例中约有三分之二是由10种不同类型的癌症造成的。其中,肺癌是全球最常见的癌症,新增病例达250万例,占新增病例总数的12.4%。女性乳腺癌位居第二,新增病例达230万例,占新增病例总数的11.6%;其次是结直肠癌,占新增病例总数的9.6%。前列腺癌位居第四,新增病例达150万例;胃癌位居第五,新增病例达97万例。价格更亲民的肿瘤生物类似药作为一种医疗手段,其出现有望减轻医疗支出负担,并提高患者获得有效癌症疗法的可及性,这得益于其在真实世界场景中展现出的安全性和有效性、临床证据以及理化质量数据。例如,多学科数字出版机构(MDPI)于2023年7月发表的一篇文章,对用于癌症治疗的生物类似单克隆抗体(mAb)与相应参考药物的安全性信息进行了比较描述性研究,并评估了上市后药物警戒数据。该研究得出结论,贝伐珠单抗、曲妥珠单抗和利妥昔单抗生物类似药与其原研药在安全性方面无显著差异。研究结果验证了生物类似药的安全性等效性,并支持其作为生物制剂原研药的竞争性替代品。因此,癌症负担日益加重,导致死亡人数不断增加,这就产生了对价格合理的治疗方法的需求,从而推动了肿瘤生物类似药市场的增长。

根据您的需求定制此报告

获取免费定制服务肿瘤生物类似药市场:战略洞察

-

获取本报告的主要市场趋势。这份免费样品将包含数据分析,内容涵盖市场趋势、估算和预测等。

细分和范围:

《肿瘤生物类似药市场分析及预测(至2030年)》是一项专业且深入的研究,重点关注全球市场动态,旨在帮助识别关键驱动因素、未来市场趋势和利润丰厚的市场机遇,从而助力企业发掘主要收入来源。该报告旨在提供市场概览,并根据药物类别、癌症类型和分销渠道进行详细的市场细分。报告还对主要市场参与者及其关键战略发展进行了全面分析。肿瘤生物类似药市场报告涵盖北美、欧洲、亚太地区、南美和中美洲以及中东和非洲的市场表现评估。

分段评估:

根据药物类别,市场可细分为单克隆抗体、粒细胞集落刺激因子和促红细胞生成素(ESA)。2023年,单克隆抗体在肿瘤生物类似药市场中占据最大份额,预计2023年至2031年间将实现最高的复合年增长率(CAGR)。单克隆抗体可通过多种途径杀伤癌细胞,例如阻断配体-受体结合的生长和存活通路。其主要作用机制包括抗体依赖性细胞毒性(ADCC)和补体介导的细胞毒性。截至2019年12月,利妥昔单抗、曲妥珠单抗和贝伐珠单抗是少数几种获得欧洲药品管理局(EMA)和美国食品药品监督管理局(FDA)批准用于癌症治疗的单克隆抗体生物类似药。

根据癌症类型,市场可分为结直肠癌、宫颈癌、乳腺癌、支持治疗、淋巴瘤和其他癌症。2023年,支持治疗领域占据最大的市场份额。预计2023年至2031年间,结直肠癌的复合年增长率将最高。世界卫生组织指出,癌症是全球重要的公共卫生问题,也是导致死亡的主要原因。随着癌症发病率的不断上升,许多肿瘤生物类似药生产商正致力于研发和推出新产品。例如,Celltrion公司的CT-P16、Prestige Biopharma公司的163 HD204、Cipla Biotech公司的CBT124以及北京迈博生物技术有限公司的MIL60均为贝伐珠单抗的潜在生物类似药,目前正在进行III期临床试验,并对其安全性和有效性进行比较。此外,这些药物在治疗非小细胞肺癌患者方面的疗效也在评估中。

根据分销渠道,市场可分为医院药房、零售药房和线上药房。2022年,医院药房占据最大的市场份额。预计2023年至2031年,线上药房的复合年增长率将最高。医院药房是患者购买处方药(例如生物类似药)的主要平台。

区域

分析:

就收入而言,北美在2023年占据了肿瘤生物类似药市场的主要份额,其次是欧洲。癌症病例的不断增加、用于癌症治疗的生物类似药获批数量的上升以及先进的医疗基础设施,预计将是推动北美肿瘤生物类似药市场在预测期内增长的因素。

癌症病例的不断增加、用于癌症治疗的生物类似药获批数量的上升以及先进的医疗基础设施,预计将推动北美肿瘤生物类似药市场的发展。生物制剂是美国最昂贵的药物。生物类似药有望比其参考产品更具成本效益。PubMed Central 于 2022 年 10 月发表的一篇文章,基于 2021 年 6 月的美国药品价格,采用生物制剂和生物类似药的平均批发价 (AWP) 进行了成本比较。分析表明,生物类似药可使贝伐珠单抗的治疗费用节省 15% 至 23%。在贝伐珠单抗生物类似药中,Zirbes 与原研药 Avastin 相比,可显著节省更多费用。用于辅助癌症治疗的生物类似药,例如非格司亭生物类似药,与原研药相比可节省17.3%至34%的费用,而培非格司亭生物类似药则可节省33%至37%的费用。此外,Epogen生物类似药可节省33.5%的费用。根据Cardinal Health于2022年发布的《生物类似药报告》,美国FDA已批准33种生物类似药上市,其中21种已上市。在这21种生物类似药中,有17种用于癌症治疗。据同一来源预测,到2025年,生物类似药预计将使美国药品支出减少1330亿美元。因此,在美国,生物类似药具有巨大的潜力,可以降低生物制剂的成本,使患者更容易获得治疗,并创造创新和科学突破,从而推动该地区肿瘤生物类似药市场的发展。

肿瘤生物类似药市场区域洞察

The Insight Partners 的分析师对预测期内影响肿瘤生物类似药市场的区域趋势和因素进行了详尽的阐述。本节还探讨了北美、欧洲、亚太、中东和非洲以及南美和中美洲等地区的肿瘤生物类似药市场细分和地域分布。

肿瘤生物类似药市场报告范围

| 报告属性 | 细节 |

|---|---|

| 2024年市场规模 | XX百万美元 |

| 到2031年市场规模 | 266.18亿美元 |

| 全球复合年增长率(2025-2031年) | 16.3% |

| 史料 | 2021-2023 |

| 预测期 | 2025-2031 |

| 涵盖部分 |

按药物类别

|

| 覆盖地区和国家 |

北美

|

| 市场领导者和主要公司简介 |

|

肿瘤生物类似药市场参与者密度:了解其对业务动态的影响

肿瘤生物类似药市场正快速增长,主要受终端用户需求不断增长的推动,而这又源于消费者偏好的转变、技术的进步以及对产品益处认知的提高。随着需求的增长,企业不断拓展产品线、创新以满足消费者需求并把握新兴趋势,这些都进一步推动了市场增长。

- 获取肿瘤生物类似药市场主要参与者概览

行业发展趋势及未来机遇:

肿瘤生物类似药市场预测可以帮助该市场中的利益相关者制定增长战略。根据公司新闻稿,以下是肿瘤生物类似药市场主要参与者采取的一些关键进展和举措:

- 2022年11月,欧加农公司在加拿大推出了阿瓦斯汀(Avastin)的生物类似药AYBINTIO。该药物适用于加拿大患有某些侵袭性癌症的患者,包括转移性结直肠癌(mCRC)、转移性肺癌、铂敏感和耐药的复发性上皮性卵巢癌(包括输卵管癌和原发性腹膜癌)以及胶质母细胞瘤。此次上市旨在扩大该公司的生物类似药产品组合。

- 2022年5月,百康生物制剂公司(Biocon Biologics)和维特里斯公司(Viatris)联合推出了Abemy,一种罗氏公司阿瓦斯汀(贝伐珠单抗)的生物类似药。百康生物制剂有限公司(Biocon Biologics Ltd.,百康有限公司的子公司)和维特里斯公司宣布,这款肿瘤生物类似药已在加拿大上市。Abemy由百康生物制剂公司和维特里斯公司共同研发,已获得加拿大卫生部批准,用于治疗四种癌症。

- 2020年4月,辉瑞公司的RUXIENCE获得欧盟委员会(EC)批准,RUXIENCE是一种单克隆抗体(mob),是利妥昔单抗(rituximab)的生物类似药。此次获批用于治疗某些癌症,例如非霍奇金淋巴瘤(NHL)、慢性淋巴细胞白血病(CLL)和自身免疫性疾病。

- 2020 年 1 月,Chorus Biosciences 与 Innocents Biologics Co., Ltd. 签订了许可协议,在美国和加拿大开发和商业化任何剂量形式和规格的贝伐珠单抗(Avastin)生物类似药。

竞争格局及主要公司:

CELLTRION公司、梯瓦制药工业有限公司、辉瑞公司、山德士集团、百康公司、安进公司、三星生物制剂公司、Coherus BioSciences公司、BIOCAD公司和礼来公司是肿瘤生物类似药市场报告中重点介绍的几家领先企业。这些公司致力于推出高科技新产品、改进现有产品并拓展地域市场,以满足全球日益增长的消费者需求。

Mrinal 是一位经验丰富的研究分析师,在生命科学市场情报和咨询领域拥有超过 8 年的经验。凭借战略思维和对卓越的不懈追求,她在医药预测、市场机遇评估和行业基准制定方面积累了深厚的专业知识。她的工作致力于提供切实可行的洞察,帮助客户做出明智的战略决策。

Mrinal 的核心优势在于将复杂的定量数据集转化为有意义的商业智能。她敏锐的分析能力有助于制定市场进入 (GTM) 战略,并发掘制药和医疗器械行业的增长机会。作为一名值得信赖的顾问,她始终致力于简化工作流程并建立最佳实践,从而为客户推动创新并提高运营效率。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST和SWOT分析

- 市场规模、价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

客户评价

Insight Partners 的 SCADA 系统市场报告内容全面,对当前趋势和未来预测提供了宝贵的见解。该团队始终高度专业、响应迅速且乐于助人。我们非常满意,强烈推荐他们的服务。

兰·凯德姆 伙伴, Reali Technologies LTD我请求一份关于特定软件市场的报告,团队在几天内就完成了。报告信息非常相关,而且呈现得非常出色。之后,我请求对报告进行一些修改和补充。团队再次迅速响应,不到一周我就收到了最终报告。

让-埃尔韦·詹恩 主席, 未来分析公司我们与 Insight Partners 合作进行了一项重要的市场研究和预测。他们清晰地洞察了机遇和风险,帮助我们制定了计划。他们的研究简单易用,数据可靠,帮助我们做出了明智而自信的决策。我们强烈推荐他们。

皮尤什·纳格帕尔 高级副总裁, 远光全球Insight Partners 凭借其深厚的行业专业知识,提供了富有洞察力、结构合理的市场研究。他们的团队始终专业且响应迅速。用户友好的网站让访问行业报告变得顺畅无阻。我们强烈推荐他们可靠、高质量的研究服务。

安达幸彦 首席执行官, 深蓝有限责任公司这是我第一次从The Insight Partners购买市场报告。起初我有些犹豫,但访问了他们的网站后,我更放心地冒险购买市场报告。我对报告的质量和客户服务非常满意。我对最初的报告有一些疑问和意见,但在与他们的分析师通过电子邮件沟通了几次后,我相信这份报告可以作为我们战略规划流程的参考。非常感谢您抽出宝贵的时间,让这次体验如此愉快。我一定会向其他人推荐你们的服务,当我们需要更多市场数据时,你们将是我的首选。

约翰·铃木 总裁兼首席执行官、董事会董事, BK科技感谢您在处理我关于尼日利亚传染病体外诊断市场信息请求的过程中所展现的支持和专业精神。感谢您的耐心、指导,以及您愿意提供的折扣,最终促成了这笔交易。我期待未来与 Insight Partners 继续合作,这一切都要归功于您与我初次接触后留下的良好印象。

奇吉奥克博士 ONYIA 董事总经理, PineCrest 医疗保健有限公司购买理由

- 明智的决策

- 了解市场动态

- 竞争分析

- 客户洞察

- 市场预测

- 风险规避

- 战略规划

- 投资论证

- 识别新兴市场

- 优化营销策略

- 提升运营效率

- 顺应监管趋势

获取免费样品 - 肿瘤生物仿制药市场

获取免费样品 - 肿瘤生物仿制药市场