分析师观点

工作场所相关疾病的增加、药品生产能力的提高、仿制药审批的增加以及研发投资的增加医药板块带动美国医药市场增长。然而,药物开发和上市审批的高昂成本阻碍了市场的增长。美国医药市场预测按产品分为疫苗、生物制品和生物仿制药以及小分子。小分子细分市场进一步分为仿制药和品牌药。小分子细分市场在 2022 年占据最大的市场份额。生物制品和生物仿制药细分市场预计在预测期内复合年增长率最高。

制药是一个广泛的细分市场,整合了一组根据其药理作用和分类的化学品。治疗用途。例如,生物碱是第一种从植物中提取的纯药物;它们包括奎宁、尼古丁、可卡因、阿托品和吗啡。同样,一些药物是由动物制成的,其中包括含有激素的腺体提取物。这些药品可诊断、治疗和预防癌症、糖尿病和遗传性疾病等慢性疾病。

市场洞察

仿制药的批准增加

作为品牌药物替代品的仿制药的需求药物由于成本低廉而大幅增加。许多品牌药专利即将到期,这是仿制药产量激增的主要原因。 2023年2月,Zydus Lifesciences的两款仿制药获得美国食品药品监督管理局(USFDA)的初步批准:波生坦片(32毫克)和卡格列净片(100毫克和300毫克)。波生坦片适用于治疗3岁或以上儿童肺动脉高压(PAH)。卡格列净片剂可改善 2 型糖尿病患者的血糖控制。 2022 年 7 月,Glenmark PHARMACEUTICALs Inc. 的醋酸炔诺酮和乙炔雌二醇胶囊以及富马酸亚铁胶囊(1 毫克/20 微克)获得美国 FDA 批准。批准的药物是艾尔建国际制药公司提供的 Taytulla 胶囊的仿制药,这是一种处方避孕药。 2022 年 11 月,美国 FDA 暂时批准了 Lupin 的 4 毫克屈螺酮片剂简略新药申请 (ANDA),该片剂是 Exeltis USA Inc. 的 Slynd 片剂 4 毫克的仿制药。

仿制药的批准数量推动了美国医药市场份额和仿制药领域的需求。

制药行业的研发投资不断增加

美国医药市场的大部分投资,公司主要针对药物发现和开发。据药物研究与制造商协会(PhRMA)统计,美国制药公司承担了全球一半以上的研发工作,投资总额约750亿美元,并且拥有大部分新药的知识产权。 2021年,辉瑞公司研发投入138.29亿美元,较2020年(93.93亿美元)增加44亿美元。同样,强生公司 2021 年研发投资达 147 亿美元,较 2020 年创下的历史最高投资额同比增长 21%。这些投资体现了公司对创造改善生活的创新的承诺。

以研究为基础的制药业是欧洲经济的重要资产;它是该地区表现最好的高科技领域之一。根据欧洲制药工业协会联合会 (EFPIA) 的数据,2021 年欧洲研究型制药行业的研发投资约为 442.6618 亿美元(415 亿欧元)。同样,亚太地区国家政府也将重点放在制药领域研发活动。例如,泰国政府推出“泰国4.0”倡议,推动国家从“制造中心”向“创新中心”转变。此外,根据印度品牌股权基金会的数据,2021 年至 2022 年间,印度药品和制药行业的外国直接投资 (FDI) 流入量达到 14.14 亿美元。

如此高的研发活动投资正在推动印度药品和制药行业的增长。目前和未来几年的美国制药市场份额。

未来趋势

越来越多地采用基于人工智能的药物发现工具

人工智能 (AI) 正在成为药物发现的重要工具医疗保健部门,因为它有助于了解药物的作用机制。人工智能工具的使用已被证明可以加速发现新候选疗法的过程;以前需要数年才能完成的过程现在可以使用人工智能在几个月内完成。除了缩短药物发现的时间之外,人工智能还有助于增强研究过程的敏捷性,提高药物安全性和有效性预测的准确性,并提高发现和临床前测试的速度和精度,从而为研发提供竞争优势战略。

许多制药公司正在与人工智能公司合作,以利用人工智能在药物发现中的优势。例如,2019 年,辉瑞与 Concreto HealthAI 合作,利用人工智能和真实数据推进精准肿瘤学工作。该公司相信人工智能工具在开发和使用药物来改善患者治疗效果方面具有巨大潜力。此外,2022 年,辉瑞扩大了与 CytoReason 的合作关系,利用其人工智能技术改进候选药物发现和药物开发流程。同样,2019 年,杨森与法国初创公司 Iktos Pharmaceuticals 合作开发了人工智能驱动的药物设计系统。杨森的新药物设计系统将通过加速分子识别来增强新药物的发现过程。此外,2020年1月,拜耳与一家总部位于英国的人工智能驱动的药物发现公司合作,拜耳将利用人工智能药物发现平台来识别和优化新结构,作为治疗心血管和肿瘤疾病的潜在候选药物。同样,葛兰素史克 (GSK) 与总部位于巴尔的摩的人工智能驱动公司 Insilico Medicine 合作,探索 Insilico 的人工智能功能,以简化新型生物靶标的识别过程。

因此,基于人工智能的技术越来越多地被采用药物发现工具可能会在预测期内引发美国医药市场分析的需求。

市场机会

慢性病和传染病发病率上升

美国疾病控制与预防中心 (CDC)指出美国十分之六的成年人患有至少一种慢性疾病,如癌症、心脏病、肺病、中风、神经系统疾病、糖尿病和肾病。此外,该国十分之四的成年人患有两种或两种以上慢性病。根据 CDC 的数据,2019 年美国报告了约 1,752,735 例新癌症病例。最常见的癌症类型是乳腺癌、肺癌和支气管癌、前列腺癌、结肠癌和直肠癌、黑色素瘤和肝癌。此外,根据美国糖尿病协会公布的数据,2019年约有3730万人可能患有糖尿病,占美国人的11.4%。其中,约2870万人被诊断患有糖尿病,而约850万人没有接受适当的治疗。诊断程序。此外,根据 2019 年全国流动医疗调查,有 1,020 万人次就诊治疗传染病和寄生虫病。

根据世界卫生组织的数据,慢性病占总疾病负担的 77%,占总疾病负担的 86%。占欧洲所有死亡人数的百分比。因此,总医疗费用的 70-80% 用于慢性病的管理。传染病的发病率激增,特别是在东南亚,也可能推动未来几年对药品的需求,最终推动药品市场的增长。例如,根据修订后的国家结核病控制计划报告,2018年印度约有44万名患者死于结核病,占全球结核病死亡总数150万人的29%。因此,慢性病和传染病发病率的上升增加了对药品的需求,这将继续推动未来美国药品市场的增长。

基于产品的洞察

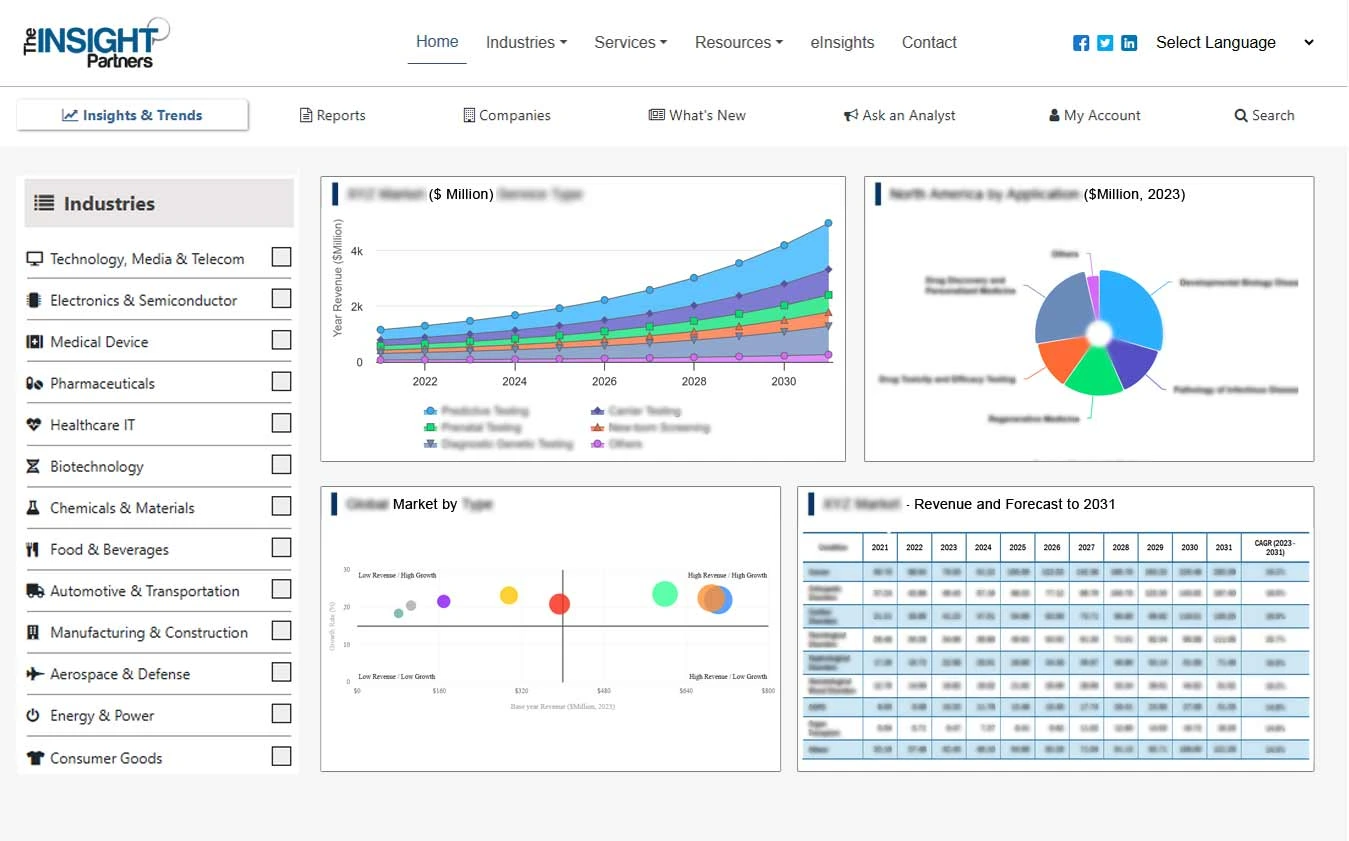

美国药品市场分析,按产品,分为疫苗、生物制品和生物仿制药以及小分子。小分子细分市场进一步分为仿制药和品牌药。小分子细分市场在 2022 年占据最大的市场份额。生物制品和生物仿制药细分市场预计在预测期内复合年增长率最高。在美国医药市场的增长中,生物仿制药用于治疗患有癌症、肾病、糖尿病和其他自身免疫性疾病(例如类风湿性关节炎和克罗恩病)的患者。生物制剂是美国医药市场前景中最昂贵的药物,每位患者每年花费数万美元。生物仿制药的价格预计将比参考产品低 15-30%。仅 2020 年,生物仿制药就节省了 79 亿美元,随着更多的生物仿制药进入市场,节省的成本预计在未来几年将大幅增长。据 Cardinal Health 称,预计到 2025 年,生物仿制药将使美国药物支出减少 1330 亿美元。患者、专家、初级保健临床医生和其他医疗保健专业人员对生物仿制药作为有效且安全药物的认识正在推动对生物仿制药的需求。此外,生物仿制药有助于改善数百万患者的生活质量,同时每年为医疗保健系统节省数十亿美元。它们已成为治疗许多疾病的有效且具有成本效益的选择,包括牛皮癣等慢性皮肤病;肠道疾病,如克罗恩病、肠易激综合症和结肠炎;糖尿病;自身免疫性疾病;癌症;肾脏状况;和关节炎。 2017 年至 2018 年期间,英国国家医疗服务体系 (NHS) 从 10 种昂贵药物转向生物制剂等价值更高且同样有效的替代药物,节省了 4.011 亿美元,预计未来还会节省更多。使用生物仿制药的潜在节省也可用于资助其他新疗法。随着慢性病的高患病率,过去五年来,用于治疗危及生命的疾病的生物仿制药的需求迅速激增。这一因素近期促进了美国医药市场趋势的增长,预计在预测期内将遵循类似的趋势。

按产品划分的美国医药市场趋势 - 2022 年和 2030 年

国家分析<近年来,美国医药市场的药品销售收入已占到全球总量的近一半。 2021 年,全球排名前 10 位的美国制药市场公司中有 5 家来自美国。辉瑞是在全球范围内提供处方药收入的公司之一,其 COVID-19 疫苗 Comirnaty 的大力推动。艾伯维 (AbbVie) 是另一家在全球范围内留下深刻印象的美国制药市场参与者,在其长期畅销品牌修美乐 (Humira) 的推动下,制药领域在 2021 年创造了创纪录的 550 亿美元收入。尽管受到几个新兴国家的影响,美国仍占据全球医药市场的主导份额。美国制药市场是全球几家主要制药公司的所在地。美国消费者可以轻松获得大多数先进的美国医药市场产品,尽管需要付出一定的成本。

美国医药市场约占全球医药市场的45%和全球产量的22%。受全球疫苗接种推广以及基本和非基本医疗需求抑制的推动,2022 年美国药品产量和销售保持强劲。由于更加注重研发 (R&D),美国医药市场在过去几十年中取得了长足进步。制药公司将超过 21% 的收入用于研发,如果药物未获得监管部门的批准,这笔巨额投资就会被浪费。 2021 年美国医药市场的研发支出总计约 1020 亿美元。由于开发有效且安全的 COVID-19 治疗方法和疫苗的成本,这一数字可能在未来几年大幅增加。

强生公司, Merck & Co Inc、Abbott Laboratories、Amgen Inc、Eli Lilly and Company、Bristol-Myers Squibb Company、Bayer AG、Takeda Pharmaceuticals、Zoetis Inc、Moderna Inc、AbbVie Inc、Pfizer Inc、Gilead Sciences Inc 和 Regeneron Pharmaceuticals Inc 是很少有在美国医药市场运营的主要公司报告。美国制药市场的领先企业专注于扩大其市场影响力和客户群并使其多元化,挖掘现有的商机。 2023 年 8 月,百时美施贵宝收购了 Mirati Therapeutics Inc。 Mirati 是一家商业阶段的靶向肿瘤公司,其目标是寻找、创造和提供突破性的治疗方法,以改善癌症患者及其家人的生活质量。 Mirati 的资产为扩大百时美施贵宝的肿瘤学商标提供了绝佳的机会,因为它们补充了公司的产品组合和创意渠道。通过此次收购,百时美施贵宝将通过整合一种重要的肺癌药物 KRAZATI 来扩大其商业产品组合。该业务获得了许多有趣的临床资产,这些资产增强了其肿瘤治疗的管道,并为组合和单药开发带来了良好的前景。

- 历史分析(2 年)、基准年、预测(7 年)及复合年增长率

- PEST 和 SWOT 分析

- 市场规模价值/数量 - 全球、区域、国家

- 行业和竞争格局

- Excel 数据集

- Bathroom Vanities Market

- Personality Assessment Solution Market

- Hummus Market

- Hydrogen Compressors Market

- Rugged Servers Market

- Formwork System Market

- Health Economics and Outcome Research (HEOR) Services Market

- Point of Care Diagnostics Market

- Long Read Sequencing Market

- Small Internal Combustion Engine Market

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

This text is related

to segments covered.

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

This text is related

to country scope.

常见问题

The market growth in the US pharmaceutical market is driven by rising workplace-associated disorders, rise in pharmaceutical production capacity, increased approvals of generic drugs, and escalating R&D investments in the pharmaceutical sector. However, the high cost of drug development and marketing approval hinders the market growth.

Johnson & Johnson, Merck & Co Inc, Abbott Laboratories, Amgen Inc, Eli Lilly and Company, Bristol-Myers Squibb Company, Bayer AG, Takeda Pharmaceuticals, Zoetis Inc, Moderna Inc, AbbVie Inc, Pfizer Inc, Gilead Sciences Inc, and Regeneron Pharmaceuticals Inc are a few of the key companies operating in the US pharmaceutical market. Leading players focus on expanding and diversifying their market presence and clientele, tapping prevailing business opportunities.

The US pharmaceutical market, by product, is segmented into vaccines, biologicals & biosimilars, and small molecules. The small molecules segment is further bifurcated into generic and branded. The small molecules segment held the largest market share in 2022. The biologicals & biosimilars segment is expected to register the highest CAGR during the forecast period.

The CAGR value of the US Pharmaceutical Market during the forecasted period of 2022-2030 is 5.36%.

Pharmaceutical is a broad segment that consolidates a group of chemicals classified based on their pharmacological effect and therapeutic use. For instance, alkaloids were the first pure pharmaceuticals derived from plants; they include quinine, nicotine, cocaine, atropine, and morphine. Similarly, some drugs are made of animal origin, which includes glandular extracts containing hormones. Drugs or medicines from animal origins are biological, biosimilar, and vaccines. These pharmaceutical products diagnose, treat, and prevent chronic diseases such as cancer, diabetes, and genetic disorders.

Trends and growth analysis reports related to Life Sciences : READ MORE..

The List of Companies - US Pharmaceutical Market

- Moderna Inc

- AbbVie Inc

- Gilead Sciences Inc

- Regeneron Pharmaceuticals Inc

- Merck & Co Inc

- Abbott Laboratories

- Bristol-Myers Squibb Co

- Vertex Pharmaceuticals Inc

- Pfizer Inc

- Eli Lilly and Co

- Bayer AG

- Johnson & Johnson

- Amgen Inc

- Takeda Pharmaceutical Co Ltd

- Zoetis Inc

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published and advised several client across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organization are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

获取此报告的免费样本

获取此报告的免费样本